Ok, I guess I confused you. What I meant is, if margins continue to tumble, then for sure I will stay away from it. My idea is not to buy just at cheaper valuations but when it begins to show an uptick in its margins. Given the current situation and the recent rally, I am saying that its valuations will anyway come down further (just my opinion). And let’s say next quarter if they show an improved performance, you might as well start buying some then where you can feel more confident about the prospects and you would be getting it for cheaper.

2 Likes

Alkyl amine concall may 2022

1…Challenging year

(raw materials and energy input costs)

=.This was a very challenging year for Alkyl Amines and our results are

showing that. Most of our raw materials and energy input costs went up by a large percentage. We managed to pass some of the increases in our price to our customers,

but that was not enough. Things have started looking better with many of the raw materials prices coming down to some reasonable levels.

=We have grown on the top line by about 25%, as you have seen, year-to-year and most of

that growth has come from price rises. But the price rises have not been sufficient to keep our margins intact because the raw material prices or rather, input prices including

the energy costs like coal and ammonia and all the other raw materials have gone up

considerably especially in the last six months. Fortunately, they have stabilized now

and slowly we are able to pass on some of these increases onto our customers. Looking forward we are a little optimistic that the worst is over.

=However, it is difficult to say

because there is a lot of volatility in the market due to the Chinese issues and Ukraine war and all the logistical issues people are facing.

2…Capex

A= We have put more capacity on ground for one of our products, that is, Acetonitrile.

B= We are also in the process of establishing a new large amines plant at Kurkumbh, which would come on-stream in the next nine months.

C=Dahej plant

I think we will have to look for some more land because along with methylamines we will put up some derivatives there is other plants also. So definitely we already

looking for some land. So maybe in a next six months or a year’s time we will have a lot of land which will be suitable for us.

3…Operating margin

Q=When do we anticipate our EBITDA margin to go back to the net 20’s the range that you guided earlier?

Ans=In fact, I hope to have that as soon as possible but if the cost of raw materials come down a little bit and do not go up further plus the cost of energy that is coal comes down significantly then we are very confident we can bring up the EBITDA to a very decent level.

Q=But we are not passing it on to the customers over the last two quarters I think we are taking a hit ourselves but when do we expect that to pass to the customers at least partially.

Ans=We are trying to do that but we cannot just increase otherwise they will get into issues and then we have competition from imports also. So we have to be very careful how much we can pass it on.

=Margins as you see are stabilizing and probably will improve

as we pass on some of the increases in our costs on to customers. The process has begun towards the end of last year and continues. Looking forward we are not able to say how much the raw material prices will go up or down, but at the moment we are optimistic that the margins will improve as we go along.

4…Acetonitrile

Q=INEOS has recently announced Acetonitrile capacity

expansion by around 15000 tons and also we have seen your domestic competitor also increasing their Acetonitrile capacity by another 15000 tons. So to what extent do you

foresee this could possibly impact the realizations for the product?

=Yogesh Kothari: Well I can tell you one thing that Acetonitrile is a growing product and I do not foresee

any issues in capacity because a lot of material is imported now and it is going to be

challenging, but we are very confident that the quality and the service which we have will definitely give us an edge. So we have already established a market and we will continue to do better in Acetonitrile.

=Acetonitrile: Most of the 25% growth rate on the top line has been largely due to price almost 2/3rds to 70% has been price and the rest has been volume.

= As far as Acetonitrile is

concerned, we have begun the plant in the last quarter of the last year January to March and slowly it is being ramped up. Looking forward we think between the two plants we

will probably hit 60% to 70% of utilization of our capacity and we are hoping to push it

to even further because there is a market out there, but as you can appreciate that

introducing a new plant, new market it takes a little time. So we hope to get to the 60%-70% capacity utilization both plants put together.

Q=Three, four years back the price used to be 120 a kg and then there was a demand for it,

it shot up to 300 to 400 a kg. So with Balaji also adding a new plant and so do you see

that the price of ACN going down below 200 kg.

Ans=Well it is always possible if there is more supply than the demand it could happen and

also there are imports also. So there is always a possibility to it. Then you have to see at what rate you can operate at and what is your cost of production and how you manage your plant.

=We manufacture from acetic acid and ammonia which is a much, greener route. You can call it green because really speaking there are no side products. It is all getting recirculated within the system hardly anything goes out. So this is something which h is very positive for our plant, our company and many of the international players also

prefer our type of production and since now we have two locations where we make acetonitrile, it gives more confidence to the customers that they can get their material

from two different locations. So that is why we are very positive on acetonitrile.

5…Kurkumbh plant

=Kurkumbh Capex so we are doing almost 300 Crores of Capex for around 35000 tons of ethylamine capacity.

=We are putting up a very large plant at Kurkumbh for making ethyl amines and our capacity will be quite high compared to whatever capacities are there and for our existing plants also we have technologies to change them over to other amines.

6…

Other expenses

=Other expenses” includes our power, water, fuel. As you all know, that

energy costs have substantially increased over the last six months and in fact the last three months much more. Coal, which we use for heating, has almost tripled from what

it used to be a year ago. So that is to a large extent where the other expenses have gone up. The rest of it has not really changed that much. Power, water, fuel which you see

has significantly changed the other expenses.

7…DMF

Q=. You had said our competitor produces DMF. So I would like

to ask do we have capabilities to produce DMF.

Ans=Currently we do not have the capability but we have the process and at some stage we

may do it. Before that we will be adding some more methylamine capacity because

dimethylamine is needed for making DMF and that is what is going to be needed in

future. So at the same time we will be planning a new methylamine plant maybe two

years down the line.

8…Intermediates

Q=As we see that there are a lot of companies which are going under very specialized chemicals wherein they can actually drive the margins and direct the prices. So are you

looking for something on those lines or you are looking only for those products which

are right now in your portfolio.

Ans=We are largely in the business of what we call intermediates, which means we are not

commodities and we are not what you might call performance or specialty chemicals

which are sold on performance or formulations. But we have a few products which are

unique and where we are able to set prices, of course within limits which are comfortable. But, by and large, we would define our company as an intermediates

company rather than a performance chemicals company.

9…Over capacity and commonality of products

Q=Because so the fear is that the commonality between both is now sort of meaning

earlier the commonality was not that high now the commonality is sort of rising by the

day and if both the companies are looking at selling this much in the domestic market

then is there a fear that there could be some price wars in order to get your capacity

utilized or you do not envisage that kind of a scenario.

Ans=It is always a possibility there have been periods of time when there has been an

overhang of capacity and there have been periods of time when both of us have been

behind the curve and there has been a shortage but this is part of the business and itisa

cycle sometimes you are ahead, sometimes you are behind and do not forget there is a

third player also: RCF.

10…Capacity utilization in 2022

=Because acetonitrile we have just

expanded the capacity, so obviously there is a lot of headroom

=. In methylamines we

have expanded a year and a half ago in Dahej and that is likely to be used up.

=Next year or so we will be probably using some part of the Patalganga plant. If you remember we

have a plant in Patalganga which is a swing plant between ethyl and methyl and we will probably be using the methyl plant and maybe as Mr. Kothari just mentioned two

years, three years down the line we will need another methylamines plant.

=That leaves us with the ethylamines which we have just now mentioned that we are expanding that

capacity because we feel we are reaching the limits of capacity of existing plants by the

end of this year. So we will be expanding the capacity at the end of this year which

hopefully will last us for another five years at least.

11…New products

Q= We have also seen your competitors significantly expand

capacities across newer product lines which could be a DNC or a DMF or a

butylamines as well now to diversify away from some key products now what is Alkyl thinking about in terms of either focusing on the key products where you have competency or are you also looking to go beyond them.

Ans=

A…acetonitrile was a new product which has made a sizable part of our revenue that was introduced about four, five years ago significantly. For it was the trial runs were

about seven, eight years ago but significantly we expanded capacity about four years

ago.

B… we have a product called diethylhydroxylamine which is also a significant product.

C…then there is dimethylaminopropylamine which is also a significant product.

D…Then we have products like DIPEA and there are some speciality products which are not that larger volume maybe a 500 tons but they contribute significantly.

Q=Apart from acetonitrile are there any other products which have a capacity of over say

15000 tons per annum

Ans=Ethylamines, DMAHCL methylamine, acetonitrile all over 10000, 15000 tons.

Q=Sir any new products that we are looking to introduce now, so any significant new

products which we have completed R&D and kind of trial runs and looking to introduce in F¥2023.

Ans=We have several products in pipeline but we will be only sort of talking about it only

once they become commercial at this stage we would not try to disclose that.

12…Growth

Q= we can safely see a volume growth of around 15% to 17% percent coming on for Alkyl Amines for next four to five years depending on some of the years where the volumes could be lesser some of the years where the volumes would be higher

based on the demand supply

dynamics.

Ans=I agree with you there we have always managed that 10% to 15% increase and | think looking forward I do not see things changing

13…Competitiors

Q=My only question is about the market share. Is there any market share loss because our

other competitor, the domestic competitor has done the volume of about 34% up and

we have only done 10%-11%.

Ans=I think it is one of the products which we do not manufacture is what has really aided

our sort of co-producer we do not make Dimethylformamide which is what has to a

large extent helped our co-producer.

Disc…invested from lower level and may add on dip

My latest portfolio

6 Likes

Thank you sir for posting concall details. I heard the concalls. Some investors were pointing out repeatedly that Balaji is doing capex and their margin is better…I felt that they are just trying to get some data from Management.

anyways…I have invested at quite a high level in alkyl amines…I trust the management. If possible, can you do some absolute valuation for Alkyl Amines at current price of 2570? it would be really helpful to add further to my existing position… Thanks in advance.

3 Likes

Agreed. Although they have highly stressed margins, but their conversion ratios (cash, WC, inventory) seem to be better than Balaji.

Disc: Invested (is one of my largest holdings)

2 Likes

Do they release investor presentation?

I couldn’t find it on BSE website / company website.

e11263a7-24f3-4199-9e16-af55d9b0d089.pdf (3.2 MB)

Though margins have improved but lackluster results.

3 Likes

Short notes from last concall:

- Ethylamine plant should be coming up by May or June 2023

- Above plant in four years down the line when full usage of our assets is being made could be between Rs. 600 to 800 crores on the top line

- Europe conflict increasing price of Amonia

- Should have a muted year in terms of sales growth. Managment pointed out domestic pharma is having slight slowdown which impacts sales.

- Overall for the company we may be between 70%-80% capacity utilization.’

- Top line decline is largely value driven, not volume driven. There’s been a drop in prices.

- At some stage perhaps we will get into making Dimethylformamide. (DMF)

4 Likes

I am invested in this at 2715 levels. 10% of equity portfolio and very negligible part of my overall portfolio. I want to know more about the valuations of this stock.

Instead of valuation, i would be more curious about its growth trajectory. Will this company grow as in the near past or that was just one off and its a cyclical chemical company with no room to grow at such level to become a constant compounder and part of one’s Core portfolio? Or it was one opportunistic bet of 2020 and 2021 , whose time had come and now gone and in next 5 to 7 years it will remain stagnant , if not degrow. I would be interested more into its long term outlook…If some learned member can help me on this, i would be indebted. I have read most of its concalls and not able to made up my mind to retain it in my portfolio or sell it in immediate future.

Disc. Invested at higher levels and currently in losses.

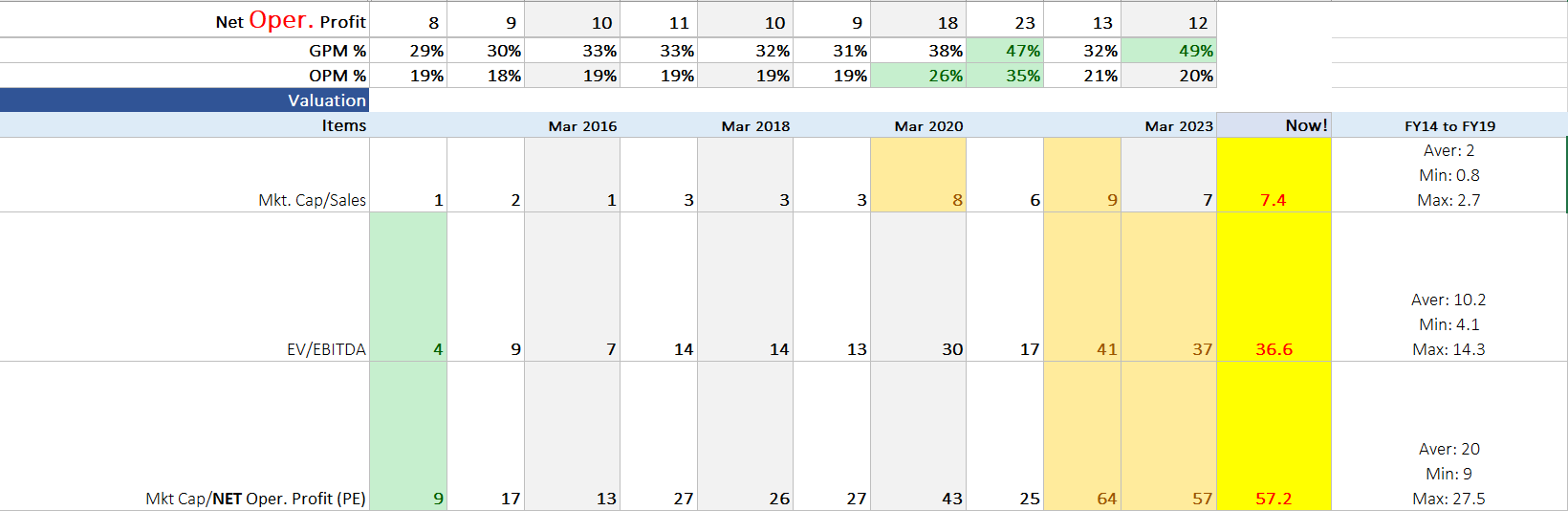

Current OPM are at the level seen in the period of FY14 to FY19. In those years, mkt valued this business at 2(Mkt Cap/Sales), 10(EV/EBITDA), and 20(PE) on average basis. These parameters are currently at 7.4(Mkt Cap/Sales), 37(EV/EBITDA), and 57(PE).

You need to focus on the levers that are expected to improve the OPM and revenue to take a final call on the trajectory of the current valuation.

Details as below:

2 Likes

If its operating margins vary so much from 16% to 35% during covid years, it indicates that its margin varies as per market conditions and raw material price fluctuations. This means , business doesnot have any moat as such and no pricing power and it has to price its products as per its customers. It doesn’t have much say in its product pricing. Also it means, if in future , if its margins improve, then its price will also recover, giving the false impression of its secularity. But its inherent nature of margin fluctuations and no-moat and at mercy of clients…will still remain.

-

Good Investment (Valuation) ? I think that prevailing valuation still bakes in outlier margins as sustainable margins and correction/consolidation in price is more likely till earnings catch up. Since supply chain has normalized, margins are back to the level at which products are competitively priced.

-

Good Business? Yes. The same can be judged by using all the traditional fundamental parameters [CAGR of BV, ROE, CAGR of Sales, OP, NP, Profit Vs Cash Flow, Cash Conversion Cycle etc.]. Even only considering the 20% consistent OPM, business will be in the top 20% out of all listed ones in the Indian market. The ranking further improves if one considers the consistent ROE with increasing BV.

P.S:

- Neither an advisor nor invested. All the above are just personal opinion for deliberation and should not be considered as a recommendation.

- A good way to etch the lesson that even a good business can turn in to a bad investment in the short run if valuations are not valued !!!

2 Likes

One more question I have in general, not specific to Alkyl Amines…but asking by taking example of Alkyl Amines, since we are on this topic…Operating margins during 2014 to 2019 can be 15-16% , but since then many projects they executed, many new factories came up, new capacities installed leading to scale benefits. So is it practical to expect same margins now, when things are changed…Margin re-rating, PE re-rating also happens. Then what is a better metrics to judge the current business scenario, instead of comparing it with its past version? Sometimes even higher margin new products are also introduced, which were not there in earlier periods. What is the better way to judge such ever-evolving companies?

Retaining gross margins (GM) happens with a lag for B2B business, even if it is very well established.

- Customers resist price hike, and start looking for alternative sources if terms are not lucrative.

- Key raw material costs keep increasing with inflation and dynamic supply situation.

Operating Margin (OPM) expansion possibility can be sensed by focusing on:

- Gap b/w capacity and production: Management commentary about the expected sales growth ++ type of products to be launched.

- Operating Leverage: Contribution of fixed operating costs (Manufacturing, Employee, and Others) in overall expenses.

If sales growth materializes and fixed operating costs do not increase to a similar extent, OPM increase would be inevitable.

In my opinion, past margins provide a solid anchor to base valuation since most management do their best to avoid lowering the established levels. Even maintaining consistent level of OPM is a good performance in my view. It’s like running on a treadmill, one needs to do a lot to stay at the same place.

P.S: Open to hear views from far thinking or well read minds on VP around this topic.

3 Likes

Notes from the AR, Conference calls from 2016 to 2023:

Management:

- Yogesh Kothari (CMD): Aged 74 years; Chemical Engineer from Institute of Chemical Technology, Mumbai; Master of Management Science and MS-Chemical Engineering, from the University of Massachussets, Lowell, U.S.A. ; promoted this company in 1979. 37+ years of experience in chemical industry. First-generation entrepreneur and ex-President of Indian Chemical Council.

- Kirat Patel (ED): aged 70, B. Tech. (Mech.) from IIT, Mumbai, and M.M.S. (Finance) from Jamnalal Bajaj Institute of Management, Mumbai. Working with the Company since its inception.

- Suneet Kothari (ED): CMD’s son. Aged 47 years. Chemical Engineer, Chemistry/Biochemistry Graduate from Cornell University, U.S.A. and MBA from INSEAD, France. Joined in 2001.

- Rakesh Goyal (Whole-time Director – Operations): Effect from June 1, 2022 to May 31, 2027.

- Joined in April 2018 as COO.

- Aged 55 years; B. Tech (Chemical) from IIT, Kanpur. Diploma in Business Management from ICFAI, Hyderabad. 28 years of experience in manufacturing, Technology Transfer, Process Development, Quality Management and Sales and Marketing. Earlier, he worked with National Peroxide Limited (NPL) as VP (Operations) for 4 years, Jesons Industries Limited as VP (Operations) for 1 year, The Dow Chemical Company for 10 years in various important positions in Process, Control engineering, Technical departments and eventually as Global Improvement Leader, Hindustan Unilever Limited for 5 years as Manufacturing Manager and in NOCIL Limited for 4 years as Process Engineer Officer.

- Ms. Kanchan A. Shinde (CFO): w.e.f. May 19, 2022. Kirat M. Patel was CFO up to May 19, 2022.

- Experience of 18 Yrs. in Finance, Accounts, internal controls, financial analysis, and taxes.

Key Points:

- Methyl Amines: Not easy to transport in large quantities since it is gaseous and needs pressure vessels. Hence, least affected by import. Only 3 suppliers [Alkyl, Balaji, and RCF] in India.

- Size of projects is not that large for larger companies to come and invest in India. So, it is a niche sized area which is comfortable for us and local competitors. Industry is ~duopoly.

- Local manufacturers are preferred as Just-In-Time delivery is expected since products are hazardous and consumers do not want to import and store in large quantities.

- Amine molecule is very versatile one and used in many medicines. Repeat customers…99%.

- EBITDA margins sustainable? Will not go back to the EBITDA margins of the old days (i.e 18%) as fixed costs are distributed over a bigger scale of manufacturing. 30% kind of margin seems difficult. Margin volatility (20%~35%) has some buffer due to specialty products.

- As cost structures are similar for competitors, prices settle to acceptable level in the market.

- Balaji Amines overlap in ~ 50% of our sales. 3rd player RCF is a significant player in methylamines and they do overlap some of their products, more with Balaji then with us.

- Industry and Sales %: Pharma 50%, Agrochem 20%, rubber chemicals 5~10%, and Others 20%.

- Nature of contracts: Usually 1~3 months.

- Plants: 2 plants at Patalganga (MH), 3 plants at Kurkumbh (MH) and 12 plants at Dahej (GJ).

- Palette ~100 products, 30~40 under active sale, 8~10 under R&D. Mkt. Size: C1 (methylamine) > C2 (Ethylamines) > C3 (Isopropylamine). C4/5/6 are smaller markets. 3 Product categories:

- Aliphatic Amines: 50% Volume. E.g., Methyl, Ethyl, and Others – Isopropyl, butyl

- Derivatives of Amines: 30% Volume

- Specialty: Products that do not use amines, 20% Volume. E.g., Acetonitrile, DMA HCL

- Acetonitrile: Manufactured from acetic acid and ammonia (no side products). It’s a growing product, used as a solvent, no cheaper alternative. Established a market with quality and the service and will continue to do better. Total capacity ~30,000 TPA & ~ 65% utilization.

- Expect 15% volume growth in FY24

Capacity:

- Max. utilization can go up to 95% | Amines capacity ~100,000 tons. Plus 30,000 tons (Ethylamine) by mid of FY24. 3 yrs. down the line another 45,000 tons (Methylamine). Acetonitrile capacity ~30000 tons. The other products capacity is fungible: 10 TPA to 40 TPA. Methylamine, Ethylamine, DMA HCL, and Acetonitrile all over 10,000 tons.

- Building capacity takes ~2 years. Utilization ~3 years. Later do incremental debottlenecking.

- Expect progress on new land request by mid of FY24. Capex (excluding land), in '23, '24 and '25 would be about Rs300 crores, Rs200 crores and Rs100 crores, respectively to launch 3~4 specialty and derivative products, and may add ~15% to 20% to top line and hopefully a larger portion to the bottom line.

- DMF (Dimethylformamide): Do not have the capability but have the process and may do it after enough inhouse methylamine, which is needed for DMF, capacity.

Risks:

- Growth comes from the growth of clients, primarily Pharma and Agrochem Industry who face competition from Chinese manufacturers

- Energy Intensive business: Requires coal to make steam needed for distillation process

- GPM fluctuation: Raw material [Major ones - METAHNOL, Ethanol, Ammonia, isopropanol, coal, and acetic acid] prices change with crude oil, but finished goods prices as they are mkt. driven [Import Prices, local competition to gain market share].

- Pricing driven by market based on prevailing prices of finished goods (import landing) as well as raw material, and the intent to maintain market share. Most of the products are import substitute. Hence, imports price is the benchmark to price the finished products.

- Operating in the intermediate business. No plan to forward integrate and step in to customer area. Hence, limited opportunity for further margin expansion.

- Upgrading plants to be ZLD, but no plan to operate with ZLD. If enforced, it will add to cost.

- Limited Exports opportunity. Established large players in the USA, Germany, and China. Opportunity improves only if anyone stops further manufacturing of these products.

Overall Impression:

- 15% volume CAGR in the long term [Growth of 8%~12% per annum for a longer period with boost of 30%-40% in 4-5 years when establish a new Aliphatic Amines plant]

- EBITDA at least 21%

- Continuous capacity addition (debottlenecking or new plant) with internal accruals.

- Customer Stickiness | Clear communication & Transparent Responses | Avoiding predictions of the future earnings - No comment on product prices, Margins, Qty and WIP products

- Expected (transcript of May 20, 2022) sales of 3100Cr. and Op. Profit of 750Cr. by FY25. | Contributors: Growth in the Traditional Business, 1.6x of upcoming commissioning of the EthylAmines’ new capex (400Cr.)+, ~100 Cr. from Diethylketone, and 20% from new 4~5 special products | Capex FY23, FY24, and FY25 – 300, 200, and 100Cr. respectively.

Disc: No Position.

17 Likes

very concise analysis. it gives a preliminary hint about the nature of business company doing.

Few questions : -

-

In FY 20 and FY 21, operating margins were suddenly high , 26% and 35% while long term average had been around 19%. What was the exact reasons for this sudden rise for just 2 years and is there any such future possibility of this happening?

-

PE re-rating has happened in last 2 years. Past 10 year average PE has been 20 , while 5 year average has been 40…but from last 2 years , PE has been re-rated and in the range of 65-70. Is this sustainable? and if so why? I mean, is there any change in nature of business.? You have said that they don’t want to go in forward integration direction, then what is this PE expansion due to?

-

When I see a long term Stock Price chart , what I observe is, whatever big move that has come in the price , is only after March 2020…But from 2005 till 2020 , its a normal earnings growth reflected in price. So what was happening in this business during those years?

-

After 15-20 years of good business performance, its still under smallcap category. Is there a chance that in next 10 years, it can become a large cap company? Is there such business scope or it will remain as a small cap company ,all its life?

-

Compared to Deepak Nitrate, I know they both have different product categories and different chemistry. .but just for assumption, I want to paint them with same brush as chemical companies, then which one out of them has Target market so big and scope such that it can become a large Cap company?

4 Likes

Your questions need too much crystal gazing, which is not my forte.However, I will share some additional facts.

Improved operating margins in FY20, FY21: Due to benign raw material price and better price realization. In those days, supplies from China were disturbed and the end customer (Pharma Industry) was doing well. Those margins were outlier, at least for the near term. 21~22% range would be the new normal.

Valuation: Valuations of this business (12~15% growth + B2B processor + Miniscule pricing power + continuous capacity required for growth) are nearing that of Page Industries. It became too popular, inferring from the shareholders count of the last 3 Yrs.

| Mar 2020 | Mar 2021 | Mar 2022 | Mar 2023 | |

|---|---|---|---|---|

| Shareholders # | 12.5K | 59.8K | 213.3K | 203.7K |

Small to large cap shift: The real question shall be 'Would I make sufficient money in this position? I will not buy at these prices. However, It’s a compounder that can grow at 1.5x of GDP for a long term.

13 Likes

5 Likes

This is a fallen angel that has massively derated in the last few years.

Debt-free company with a close to 20% RoE and consistent dividend payment record. Company’s P/E expanded from 15-18ish in 2019 to 60-70ish in 2021 and 40-45 ish now. Looks like it was a 4X P/E expansion led by strong hopes of growth. Sales is growing at only 11 percent.

Good company if picked up at good price. I am thinking of a tracking position but given historical P/E looks like more fall is possible in this stock

2 Likes