This post is about a small cap that I may be invested in, it’s a very risky bet due to the company being small and not much information about management credibility. Hence pls don’t see this as any kind of recommendation.

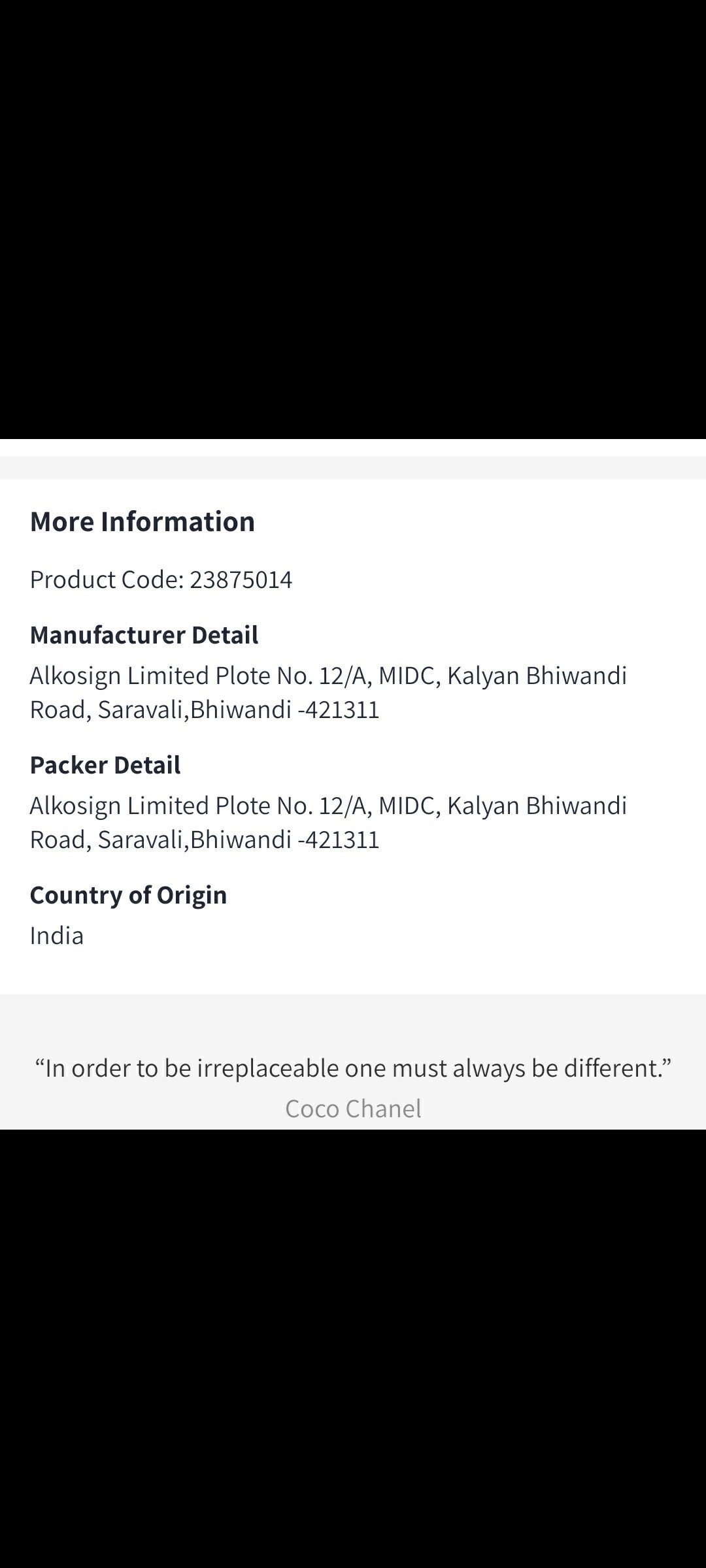

Alkosign, a micro-cap company with a market cap of around 100 crores and a relatively small free float of approximately 10-12 lakh shares, has shown a sudden surge in sales and operating profit, notably doubling and quadrupling, respectively, in its latest reported numbers. The key catalyst behind this uptick was unveiled in a founder’s interview where it was disclosed that Alkosign has ventured into manufacturing hard luggage for the well-known brand Baggit.

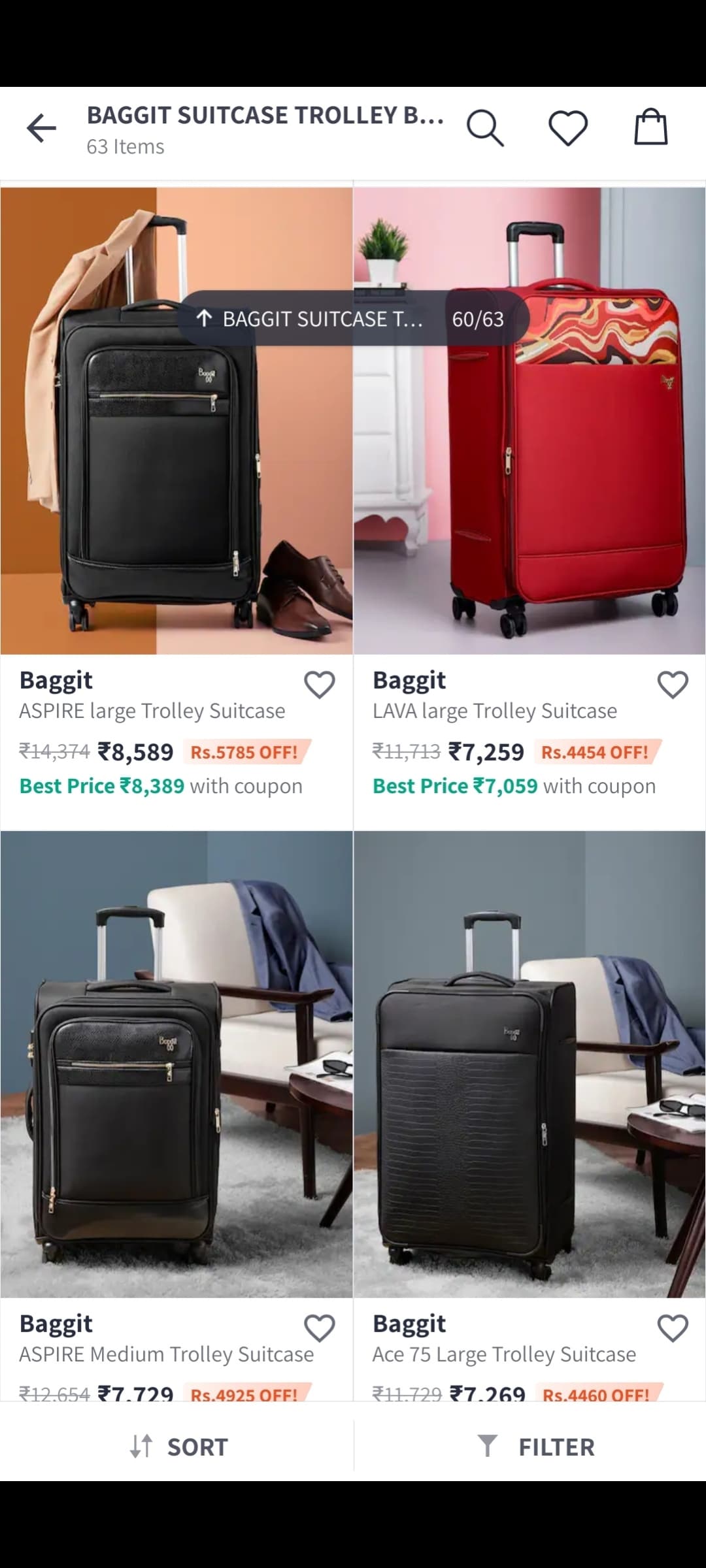

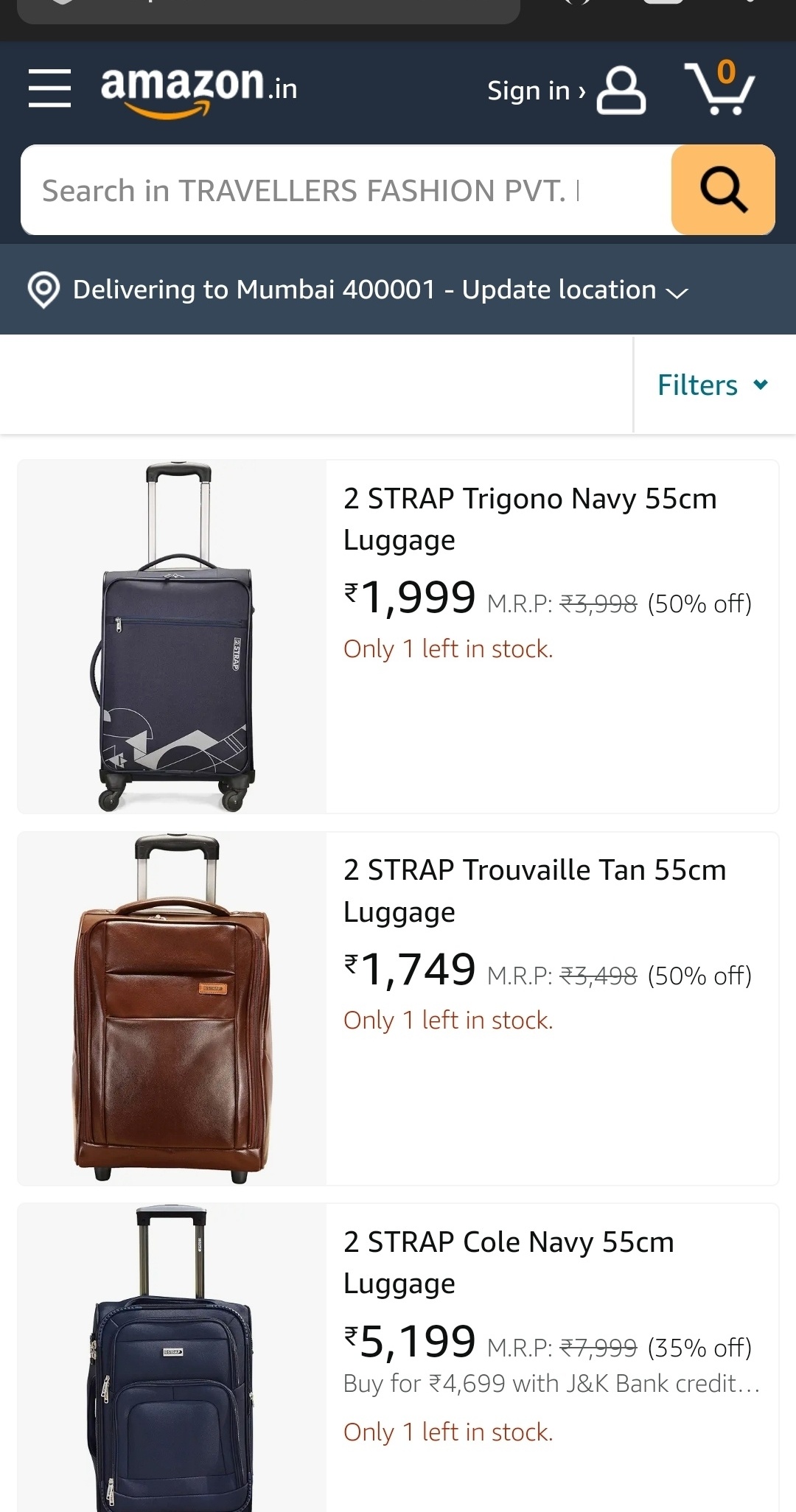

A firsthand investigation, including visits to Baggit stores in Delhi and online platforms like Myntra and Amazon, confirmed Alkosign’s involvement in producing Baggit’s entire range of hard luggage. Despite the typically low margins associated with luggage contract manufacturing, Alkosign’s own line of hard luggage under its brand name adds an interesting dimension to their revenue stream.

The CEO’s ambitious target of reaching a 100 crore turnover was discussed in the interview, and the prospect of achieving this goal appears feasible, given the new venture into hard luggage. Notably, Alkosign’s association with Piyush Pushkar of Suvid Retail, who shares directorship with Mr. Sameer Shah in a subsidiary responsible for marketing and venturing into hard luggage, adds promise. Piyush’s previous experience with Brand Concepts, now manufacturing for major brands like Tommy Hilfiger, lends credibility to the venture. The hard luggage arm of alkosign is travellers fashion pvt Ltd.

While contract manufacturing can drive revenue, it’s acknowledged that margins may not be as robust. The strategic move to ride the travel trend through Baggit, coupled with the expertise of Piyush from Brand Concepts, presents an interesting growth trajectory. The recent substantial investment by astute investor Mona Laroia in a bulk deal adds a positive dimension, making Alkosign a compelling wait-and-watch play in the market.

Link to YouTube interview - https://youtu.be/6nogIaxMv58?feature=shared

Link to twitter on detailed post with pics as unable to upload pics of luggage and shareholding details:

https://twitter.com/BOOMBERG_SQUINT/status/1725528393595162966?t=zAZUdU3Jb6ibSX7zd66gSA&s=19