Is anyone covering this.

I went through the last concall of Alkem Labs.

My understanding is that they are looking to grow at par or better than Indian Pharma. Chronic is growing well and Acute is helping (though there is some seasonality). The raw materials prices are stable and helping recovery of bottomline. Biosimilars division is tiny and not expected to impact topline significantly atleast for another few years. US price erosion has come down to single digits now (earlier double digits). No major capex in sight except for an investment in the US. They are doing very well in ROW markets and expect to continue to do so.

Currently price at around 35 times earnings, I expect nothing extraordinary going forward - maybe 10-15% (at or above Indian Pharma growth). They had a great 2020 and 2021 due to uptick in Acute business; and not so good 2022 due to increase in raw materials prices and price erosion, etc. They expect Chronic segment (around 10% higher margin than Acute) contribution and debottlenecking to help improve margins (minor) going forward.

Yesterday there was a news with allegations of 1000 cr tax evasion against the company (read on social media, not reliable) and therefore the price dopped by 6% however they came out with clarification that this is completely false, and nothing to worry about.

I am waiting to see how the India Pharma and ROW story pans out - though I do not expect great returns from here (but who knows). It is only a small part of my portfolio and no transactions in the last 6 months. Sitting at much lower prices hence the cushion to wait and watch.

Alkem Labs -

Key highlights from FY 24 -

Continues to rank no 1 in Anti Infectives, No 2 in Vit/Min space in India

India business contributes to 68 pc of sales, grew by 5.4 pc

US business contributes to 21 pc of sales, grew by 10 pc

Rest comes from RoW mkts ( LATAM, Australia, EU ), grew strongly at 33 pc

Cash on Books @ 3550 cr

Anti-Infectives mkts were sluggish throughout FY 24, which affected company’s India performance. However, the company continued to do well in Anti-Diabetic, GI, Vit/Minerals and Derma therapies

Lesser pricing pressures in US and descent volume growth in US + RoW business helped improve overall gross margins. Company believes that the worst of pricing pressures in the US business should now be behind

Company’s domestic biosimilar business ( under its Subsidiary - ENZENE ), with 7 brands continues to ramp up well

Aim to grow revenues by 10 pc in FY 25 with stable gross and EBITDA margins ( with an upward bias )

Capex lined up for FY 25 @ around 600 cr

Expecting the anti-invectives mkt to pick up in FY 25 ( as FY 24 was exceptionally weak for this segment ). If this happens, company may outperform its guidance

30 pc of company’s India products are under NLEM

Company has the largest trade generics business in the country. At the same time, the branded generics business continues to do well. Company believes, both can do well simultaneously

As the company’s chronic business ramps up in India, Margins should improve further over the medium term

Launched 3 new products in US in FY 24. Going to launch 6 new products in US in FY 25

Expect to maintain 4.5 of sales as R&D expenses going fwd

Setting up a Bio-Similars plant in US under its Bio-Similars subsidiary - ENZENE. It’s mainly going to engage in contract manufacturing operations. Expect it to contribute meaningfully from FY 27. Capex required here should be around 400 cr

MR productivity for the company is 4.5 lakh / month. On the chronic business side, its about 3.5 lakh / month - clearly there is a lot of headroom to improve the productivity here

Company’s share of Chronic business is low at present @ 18 pc. There is a huge scope of improvement here. Expect it to cross 20 pc in next 2-3 yrs

Total MR strength for the company is around 12000

Trade generics contribute to around 20 pc of company’s India business

Company is working on another 5 biosimilars to be launched in India under its subsidiary - ENZENE

Cash on books - in all likelihood to be used to inorganic acquisitions - specially in the Chronic segment. Actively looking out for the same

Company is setting up a new business division - to manufacture medical devices. Will update investors as the business goes commercial. Focus here will be on the domestic Mkts to begin with

Disc: holding, Biased, Not SEBI registered

Alkem Labs -

Q1 FY 25 Concall and results highlights -

Revenues - 3031 vs 2967 cr

Gross margins @ 64 vs 59 pc ( huge expansion )

EBITDA - 608 vs 389 cr, up 56 pc ( margin @ 20 vs 13 pc !!! )

PAT - 545 vs 286 cr, up 90 pc

R&D expenses @ 125 cr, 4 pc of sales

Cash on books @ 3845 cr

Alkem’s rank in major therapeutic segments in IPM -

Anti Infectives - 01

Vit/Minerals - 02

Pain Analgesics - 03

GI - 03

Among the chronic therapies, Alkem is ranked 7th in Neuro, 15th in Anti-Diabetic and Respiratory, 20th in Derma and 26 th in Cardiac segments

Breakup of revenues -

India sales - 2022 cr, up 6 pc ( 67 pc of total sales )

International sales - 967 cr, down 4 pc

Out of this, US sales @ 641 cr, down 8 pc

RoW sales @ 326 cr, up 2 pc

Massive improvement in Gross and EBITDA margins on the back on sharper focus on profitability, favourable RM cost environment and cost control initiatives

Will continue to invest aggressively towards future growth opportunities ( basically ENZENE’s Biosimilars plant in the US which is likely to turn profitable only in FY 27. Company is spending 400-450 cr towards this facility ). These are likely to entail operational costs. Hence sticking to full yr’s EBITDA margin guidance of 18 pc for FY 25. However, if the API prices continue to remain soft and decline further, company may report higher margins

Domestic growth in Q1 is driven by volume growth of 1.5 pc, new products at 2.5 pc and price hikes of about 2 pc

US generics business is seeing price erosion in single digits

Guiding for an R&D costs at around 4.5-5 pc of sales for FY 25

Looking at single digit growth from US mkt in FY 25. Will be launching 3-4 products and filing for 8-10 new products for US in FY 25

Expecting the growth to pick up in a significant way in the European + EMs. These mkts are showing encouraging signs and company is hopeful of growing briskly and more profitably ( vs US ) here. These Mkts are a big focus area for the company. Q1 was weak because of some supply chain issues which now stand resolved. Guiding for a mid teens kind of growth from non-US International business for next 2-3 yrs. Blended margins in these international mkts are > US and < India

Trade generics contribute to around 20 pc of company’s India business

Tax rate guidance for FY 25 @ 11-13 pc

Share of Chronic therapies in company’s India business @ 19 pc. 81 pc is acute business

Medical devices, OTC products - are two business areas where the company is working hard. Will share updates with shareholders when they finally launch products in these spaces

Cash on books to be used for acquisitions / mergers etc to add value to the business

ENZENE Biosciences ( a subsidiary ), already has 07 biosimilars in the IPM. Aim to launch 05 more over the medium term. Their US facility ( under development ) will be utilised for contract manufacturing

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

Alkem Labs -

Q2 FY 25 results and concall highlights -

Revenues - 3414 cr, down 0.7 pc

Gross Margins @ 64.7 vs 61.4 pc

EBITDA - 752 cr, up 0.8 pc ( margins @ 22 vs 21.7 pc )

PAT - 688 cr, up 11 pc YoY

R&D expenses @ 147 cr, @ 4.3 pc of sales

Segmental sales -

India - 2461 cr, up 5.7 pc ( representing 73 pc of company’s total sales ). Company’s volume growth was at 1.1 pc. Company continues to maintain No 1 position in Anti-Infectives, No 2 position in Vit/Minerals, No 3 position in GI and Pain/Analgesics portfolios. Company is ranked No 5 in the IPM

International sales - 918 cr, down 13 pc ( 17 pc of company sales come from US mkts and 10 pc come from RoW mkts ). US sales de-grew 22 pc to 597 cr. RoW mkt sales grew 12 pc to 320 cr. Launched 1 product in US mkt and received 5 new approvals

H1 Highlights -

Revenues - 6446 cr, up 0.6 pc YoY ( India sales @ 4483 cr, up 6 pc. International sales @ 1885 cr, down 9 pc. US sales de-grew 15 pc in H1, RoW mkts grew 6 pc in H1 )

Gross Margins @ 64.5 vs 60.6 pc ( significant jump )

EBITDA - 1361 cr, up 20 pc ( margins @ 21.1 vs 17.7 pc - significant jump )

PAT - 1233 cr, up 36 pc

Company’s BADDI facility was inspected in Mar 24, EIR received in Jun 24

Going to launch 1 product in US in Q3 for which they have received 180 days exclusivity

US business in H1 faced supply chain issues due to which company lost some volumes. Also there was price erosion. Expecting a much better H2 in the US business. Expect to end FY 25 with mid single digit de-growth in US business

Company has been very selective wrt products that they sell in US. This meant that they did forego some thin margin product sales. This has helped them improve profitability ( H1 profitability in this FY has been better than LY in US despite the sales decline )

IPM breakdown of Acute : Chronic is about 62 : 38. But for Alkem, its about 81 : 19. Acute business has been slow this Q2. Hence company’s growth in IPM has been 1 pc lower than the mkt in Q2

Company expects much better growth in H2 vs H1 in the India business as well

Enzene’s Biosimilar plant ( their subsidiary ) in US should go commercial in Q1 FY 26 ( have spent 400 cr on the same ). Seeing good enquiries + Orders to be made from this facility. Will share more details at an appropriate time. This facility will focus on CDMO operations

Guiding for mid single topline growth for FY 25 with EBITDA margins in the vicinity of 19 pc for full yr

US mkt seeing 6-7 pc kind of price erosion

Company hopes that their Biosimilars CDMO plant should break even in FY 26

Company’s subsidiary - MedTech ltd’s plant should also go live sometime in Q3. It will manufacture Hip and Knee replacement implants under license from Exatech US. They should be able to launch their products in the mkt by Q1 or Q2 next FY

Commercialisation expenses for both these plants ( MedTech and Enzene ) should start flowing into P&L wef Q3

Lower sales in US + Lower API prices have helped company improve their Gross Margins in H1. As the RoW sales pick up, they should also support the Gross Margins

Company also has a domestic Biosimilars business. Have commercialised 7 products in India. Aim to commercialise 3-5 products globally ( including US ) in next 3-4 yrs

In IPM, company’s focus is to grow their Chronic therapies. For the next 3 yrs, should grow at rates significantly higher than therapy growth rates in India - that should increase company’s chronic mkt share

Aim to keep improving company level EBITDA margins by 100 bps every passing yr for foreseeable future. If company happens to make some acquisition that’s margin accretive ( as they have aprox 4000 cr of cash on books ), the improvement may be even faster

Company is also bullish about their RoW business. As time passes and the scale of RoW business increases, that should be another trigger for margin improvement

India business split @ 80:20 between Branded : Trade generics. Even the margins in trade generics are also improving because of better product mix

Company has 145 approved ANDAs in US. Out of these, 100 products are currently active in US

Company will be launching Mirabegron ( used to treat over active bladder ) in US in FY 27 as per their agreement with the innovator

Disc: holding, inclined to add more, biased, not a buy/sell recommendation, not SEBI registered

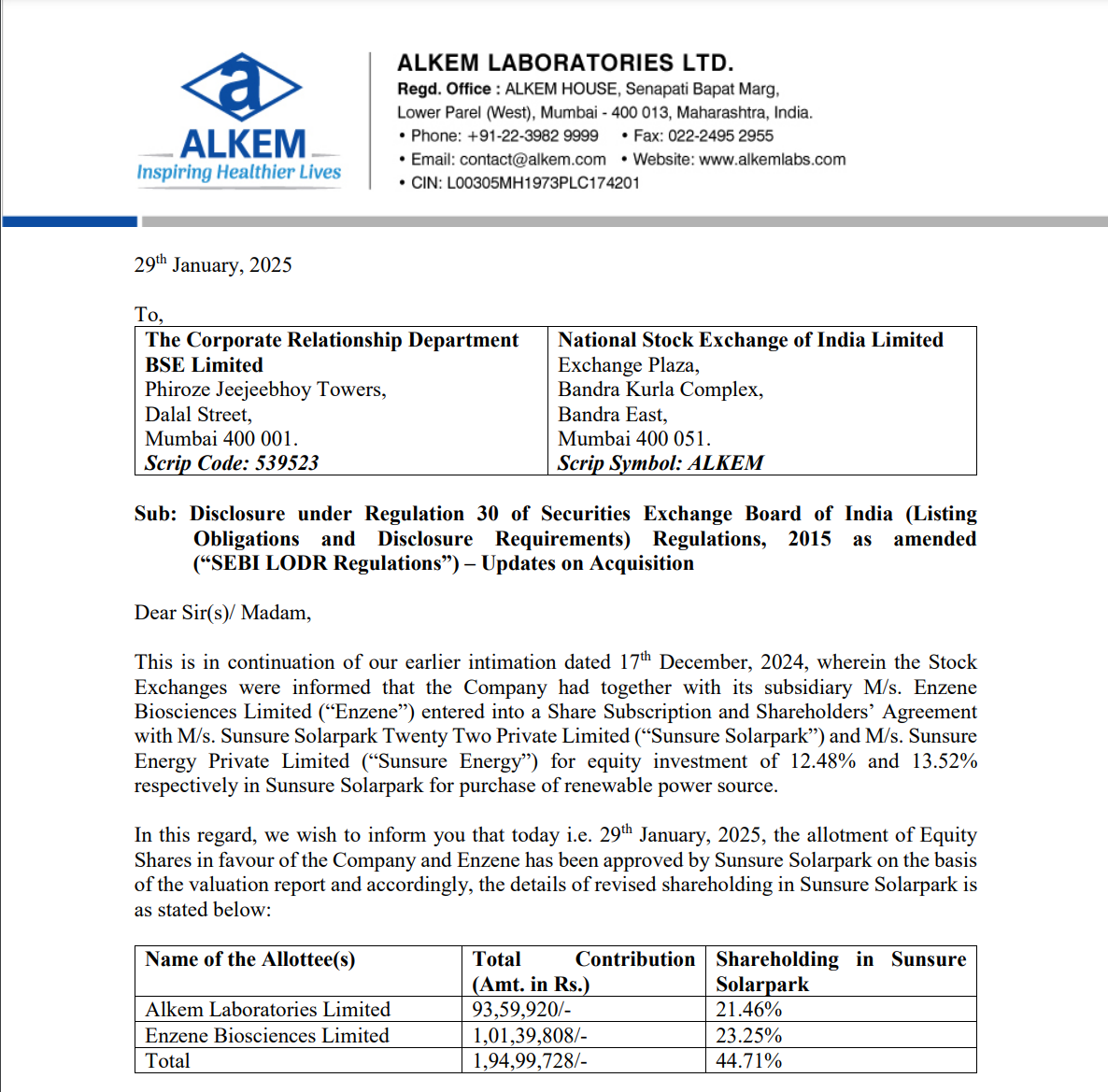

Company, along with its subsidiary Enzene Biosciences Limited, entered into a Share Subscription and Shareholders’ Agreement with Sunsure Solarpark Twenty Two Private Limited and Sunsure Energy Private Limited to invest 12.48% and 13.52% equity, respectively, in Sunsure Solarpark for the purchase of renewable power.

From Q3FY25 Concall

Financial Performance

- Total Revenue: ₹3,374 Cr, up 1.5% YoY .

- India Sales: ₹2,364 Cr, showing 5.9% YoY growth .

- International Sales: ₹960 Cr, experiencing a 6.2% YoY decline .

- EBITDA: ₹759 Cr, with a 22.5% margin , marking a 7.3% YoY increase .

- R&D Expenses: ₹131 Cr (3.9% of total revenue).

- Net Profit: ₹625 Cr, up 5.2% YoY .

- Market Performance: According to IQVIA, Alkem registered a 6% YoY growth , slightly lagging behind the 7.2% growth of the Indian Pharma Market (IPM).

9M Performance

- Revenue: ₹9,820 Cr, up 0.9% YoY .

- India Sales: ₹6,848 Cr (6.0% YoY growth ).

- International Sales: ₹2,846 Cr (7.7% YoY decline ).

- EBITDA: ₹2,120 Cr, EBITDA margin at 21.6% , a 15% YoY increase .

- Net Profit: ₹1,859 Cr, 23.8% YoY growth .

- Market Performance: Alkem registered a 6.9% YoY growth in 9MFY25, compared to IPM’s 8.0% growth .

Operational Highlights

Domestic Business

- Domestic sales accounted for 71.1% of total revenue, up from 68.6% last year.

- Outperformed in seven key therapy areas , including VMN, Anti-Diabetic, Gastrointestinal, Neuro/CNS, Gynae, Respiratory, and Urology .

- PAN-D was the fastest-growing brand in the IPM top 12, with a 15.5% growth rate .

- Volume growth of 1.1% despite a sluggish market (0.3% volume growth for IPM).

International Business

- US business contributed 19.1% of total sales in Q3FY25.

- Other international markets contributed 9.8% .

- Received two approvals from the USFDA during Q3, including one tentative approval.

- Chile market downturn due to tender exits and currency depreciation, leading to 30% degrowth ; stabilization expected in Q4.

Business Performance & Insights

- Trade Generics Business: ₹488 Cr in Q3FY25, totaling ₹1,378 Cr YTD.

- Forex Impact: Positive; every 1% appreciation in USD adds ₹10-20 Cr .

- NLEM Portfolio: Accounts for 30% of sales, limiting price growth opportunities.

- Enzene Biosciences: ₹200 Cr YTD sales, projected to close FY25 at ₹300 Cr , targeting 15-20% growth next year.

Strategic Moves & Acquisitions

Product Pipeline & New Launches

- India: First wave of GLP-1 Semaglutide launch.

- US: Key approvals include Sacubitril-Valsartan, gSuprep, and Carbamazepine ER .

- Upcoming US Launches: Topiramate oral solution and Varenicline .

- Filings: Three filed till Q3 in the year, expecting five more in Q4.

Acquisitions & Expansion

- Adroit Pharma (Dermato-cosmetology) : ₹140 Cr acquisition to expand into the dermatology segment.

- Bombay Ortho (Orthopedic Implants) : ₹147 Cr acquisition; manufacturing capacity of 2,000 hip & knee replacements/month .

- Exactech (Ortho Business Entry) : ₹133 Cr licensing deal for premium hip & knee implants, launch set for Dec 2025 .

Challenges & Risks

- Forex Loss: Booked ₹20 Cr loss due to Chilean currency depreciation in Other Income.

- Price Erosion in US: Mid-single-digit price erosion (~5%), expected to be offset by new launches & volume growth .

- NLEM Portfolio Pressure: Zero price growth in large parts of the portfolio, requiring a volume-driven growth strategy .

- Acute Therapies Slowdown: Market-wide slowdown in Q3 (5.7% growth), but Alkem expects a stronger Q4.

Guidance & Management Outlook

- Domestic Market Growth: 7% for FY25.

- International Business: Expected 13-14% growth .

- US Business Q4: Expected to remain flat YoY .

- EBITDA Margin Guidance: Q4 margin to be lower than Q3 (~13.7%).

- Big Acquisition Plans: Management is prioritizing Indian formulations expansion .