Alkem Labs, an Indian pharmaceutical company

Annual Report 2019 notes

Alkem is Ready to Scale the Next Frontier of Growth. It was a landmark year for the Company AS IT CROSSED THE REVENUE MILESTONE OF US$ 1 billion. The intense focus on building market-leading brands, investing in state-of-the-art manufacturing and R&D FACILITIES, ensuring continual adherence to quality and compliance, setting up robust supply chain and distribution network, penetrating deeper into key focus markets and driving efficiencies and productivity enabled it to achieve this significant milestone. While Alkem has firmly established itself among the leading pharmaceutical companies in India, the determination and drive to outperform itself remains as high as ever.

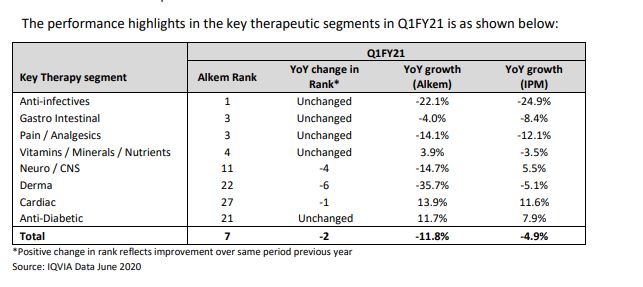

In the domestic market, Alkem is amongst the prominent players in the acute therapy segments of anti-infective, gastro-intestinal, pain/analgesics and vitamins/minerals/nutrients. The Company looks to further consolidate its position in these therapy segments through market leading brands, comprehensive product portfolio, extensive marketing and supply chain reach and an experience of over 40 years. In the fast-growing chronic therapy segments of neuro/CNS, cardiology, anti-diabetes and dermatology, the Company is taking rapid strides to emerge as one of the faster growing companies in the country. The Company looks to outperform in the chronic segments on the back of new product launches including in-licensed products, effective sales and marketing strategies, improved sales force productivity and building strong brands.

In the US market, the Company has developed a healthy pipeline of products with over 120 ANDA filings of which more than half are yet to be commercialised. Continuous investments in R&D, adherence to quality and compliance and timely product approvals will be pivotal in taking growth to the next level, not only in the US market but also in other international markets. Investments in biosimilars and its in-house manufacturing is another tactical lever for growth.

All in all, the capabilities and capacities are in place, be it product offerings, manufacturing, R&D, supply chain, technology or control systems. At the core of the Company’s ability to realise an even stronger tomorrow, is the unshakeable competitive desire of its talented team to outperform and a work culture that is aligned with organisational goals. These strategic levers will bolster the successful progression to the next level.

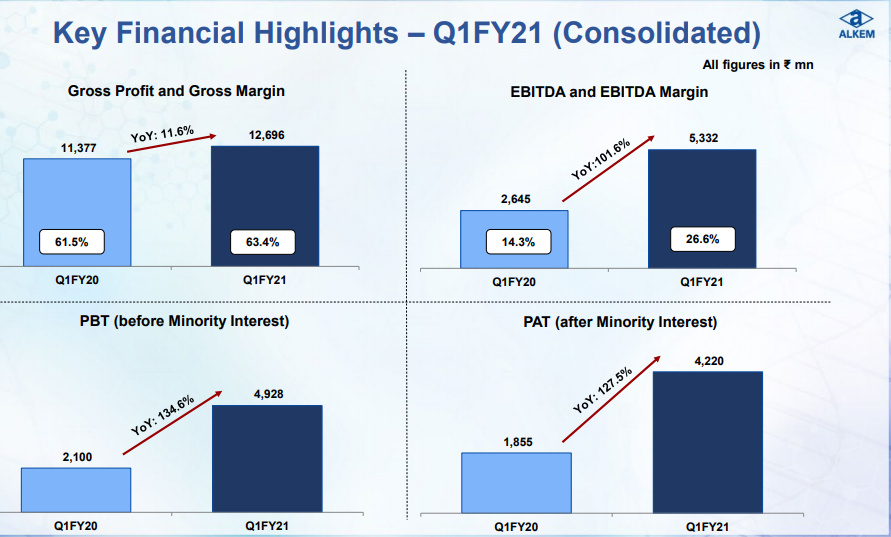

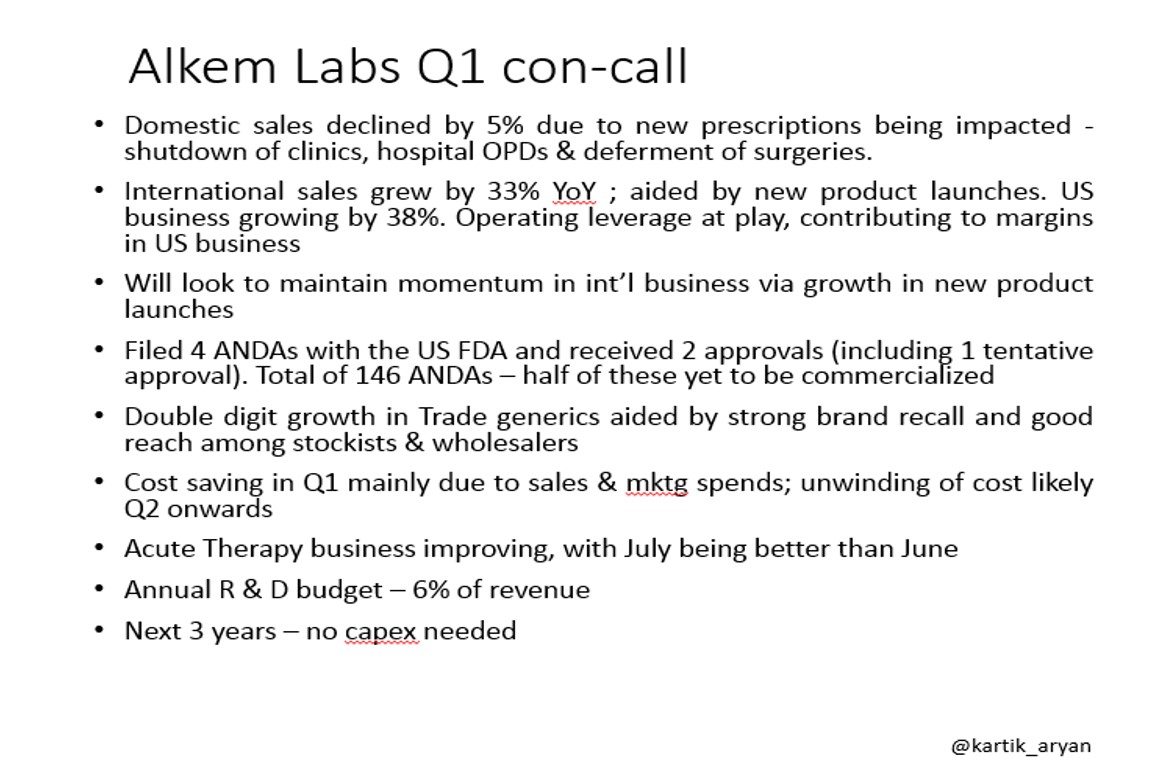

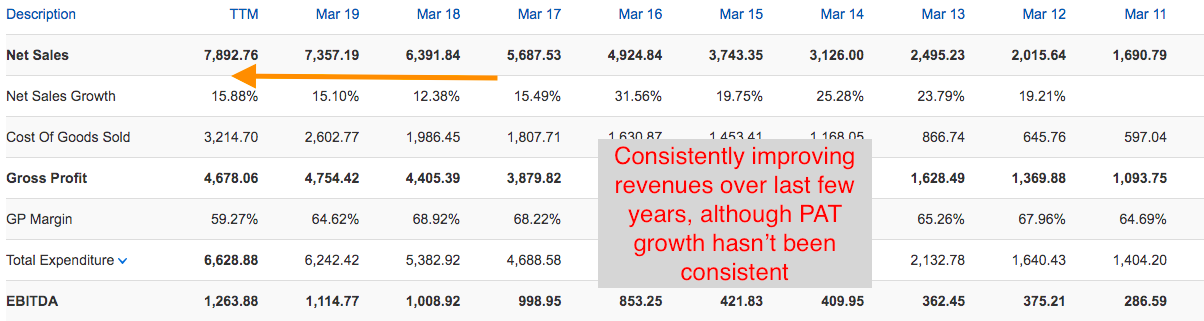

The financial year 2019 has been a mixed year for the Company. While our International business, mainly led by the US business, delivered a robust year-on-year revenue growth of 31.2%, our India business faced challenges on account of FDC ban on select products, relatively weak anti-infective season and muted growth in our trade generic business due to tightening of credit terms by the Company. Our EBITDA margin dipped by 60 basis points compared to the previous year on account of higher API prices, increase in R&D cost and change in revenue mix. However, on the working capital front, we showed good improvement over the previous year, and that translated into better operating cash flows during the year.

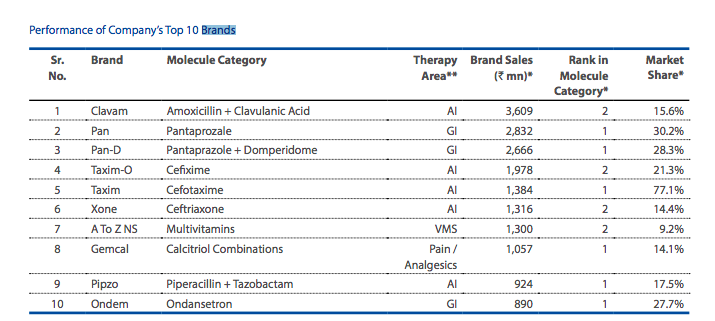

Clavam, one of their brands features in the top 10 drug brands sold in India

Key risks mentioned in the annual report include

Alkem’s products face fierce competition from multiple pharma players, which may lead to shrinking revenues and impact its competitive advantage. The occurrence of quality issues, manufacturing defects and adverse audit findings by regulatory agencies may impair Alkem’s reputation and expose it to liabilities, fines or penalties. Adverse pricing regulation by NPPA on prices of key products may reduce company’s revenue and margins.

My view

The company witnessed strong growth across major therapeutic areas in Q2 FY20. As per the company’s quarterly results, anti-infectives and gastro-intestinal segments grew 30.8% and 17.5%, respectively, whereas Indian pharma industry in that space grew only 19.9% and 12.1%, respectively. The stock can do well especially because majority of the market is looking at MNC companies and ignoring other quality companies.

Technically, Alkem is near its 52 week high breaking out with a cup and handle pattern with high volumes

Disclosure: I have recently bought a tracking position in Alkem India, I might buy more/exit if the thesis changes. Hence recency bias. I invite other members of the forum who have looked at this company to share their opinions.