there was some buzz about Piramal Enterprises trying to buy out the promoters now that its no-compete clause with Abott has expired. But looks like it was mere rumours

disclosure: no holding in Albert David. Holding Piramal

there was some buzz about Piramal Enterprises trying to buy out the promoters now that its no-compete clause with Abott has expired. But looks like it was mere rumours

disclosure: no holding in Albert David. Holding Piramal

Price to sales for Albert despite the run in the stock is only 1.2-1.3, despite it being debt free co with 75 crores cash on books.

Most pharma cos are trading at 3-5 price-sales ratio (and also having debt)

https://www.drvijaymalik.com/2018/09/albert-david-ltd-research-report-fundamental-analysis.html good report lot of red flags pointed out

Yes. Certainly indepth analysis and many valid points. Like he always does. A few can be explained, like for eg. the sale of assets, which was done above the depreciated value (they were old assets and nearing full depreciation) and infact were sold at a profit over the written down value. Also labour cost, which reason was explained by the Chairman himself. Etc.

Hopefully, the future should see a lot of improvements and things correcting out.

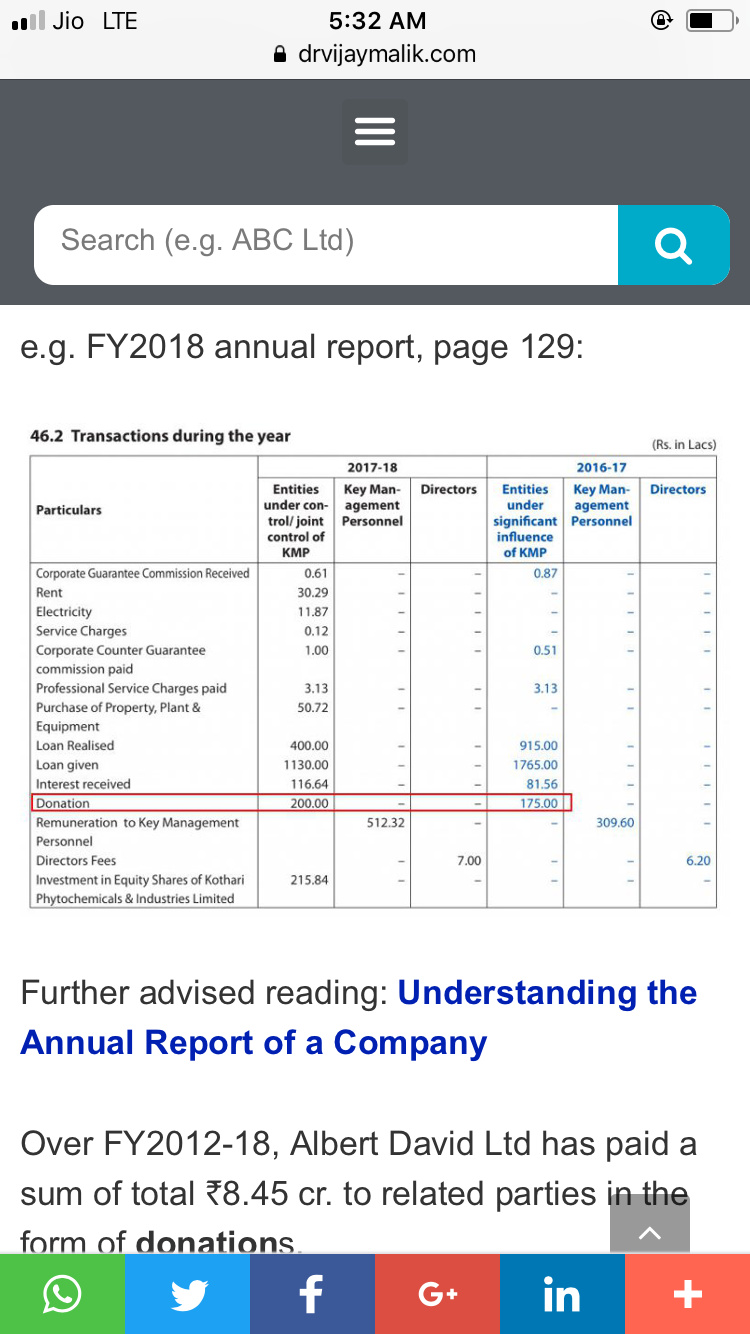

Two major red flags: (1) Number of related party transactions and to my surprise- DONATION to related parties, what is this? very serious issue (2) They are not providing data and cooperating with credit rating agency- What future hold for such a co? if numbers are true they should provide data to Credit Rating agency…

The future of a company is again dependent on how much net money it makes and whether it shares profits with shareholders or not… Which is seen by dividend payout as a percentage of profits.

Yes related party loans and investments is a known issue and I am quoting some snippets from above posts. This was raised with the management at the AGM - directly with the Chairman and later reiterated with the CEO after the Chairman had left. It needs to be seen what they do about it.

Also, the company has hardly any debt and is net cash positive by a huge margin. So debt rating, which is an opinion on the solvency of the company needs to be looked at in this context. Typically, lenders to the company push them to get ratings done. In this case, since debt levels are very low, and as pointed out, the entire assets are mortgaged/hypothecated, the lenders may not have pushed the company to get the rating done. The credit rating agency has not said that the management is not cooperating or that they are suspending the rating etc. which they have done in the past in other cases. They have just said that they are awating additional information.

Anyway, I have tried to be rational in my explanations without tilting overbearingly to the company’s side although I am invested. Concerns have been there, issues are there, and these need to be balanced with the positives. So boarders may take their individual call.

Really amazing analysis by Dr. Vijay M. of the ADL . I doubt form the past perspective one can do any better analysis then this. Kudos.

As for the issues raised in the post,I guess most of the points have already been covered by @sammy11 @Vijayk So not going to repeat it. Since Science part has been covered, I would rather focus on the art part of it.

I have been thinking about ADL its past and also what it future may hold.

Thinking of future - I can think of following scenario : -

For me as an investor : 1 is ideal 2 is good 3 is decent and 4 is where we are.

So, I see more things in favor then against me at current juncture. I will take 3/4 odd any day.

Now, which scenario will play out depends on CEO/MD skill and Promoter intention.

As, for the skills of CEO/MD looking at the past it is reassuring that he has the experience, whether he would work in this situation or not that no one can say, not even he himself. So, the only data point is the past which says that he might just be able to grow it. I mean looking at the scope( geographical, brand etc.) It is not a herculean task and any smart person should be able to grow. So, in conclusion i feel comfortable with the skill of the MD cum CEO.

Now, coming to Promoter intention ( this is what we are actually debating in the science part), In the past his methods/ decision have been questionable. Now, consider this - he is paying the CEO 1.5 cr. Think about this for a moment. If the objective of the promoter was only to milk company - he could have hired any Tom, dick and harry at cheaper rate and would continue with status quo. What does this huge salary to an outsider indicate about the intention of the promoter. I am sure he would not do it just to fool the investors. That would be a very expensive for him. So, this decision is crucial and speaks a lot about the intention of the promoter.

Now, whether from above 1/2/3 which one will play out and how would that play out for company and in turn for shareholder no one can say with certainty. So, its not a clear cut case of black and white investment. It has shades of grey.

However, I have invested my money in this business, so, its obvious that i want which scenario to play out.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/cddd5d8d-3ea7-4474-b021-e40a95534900.pdf

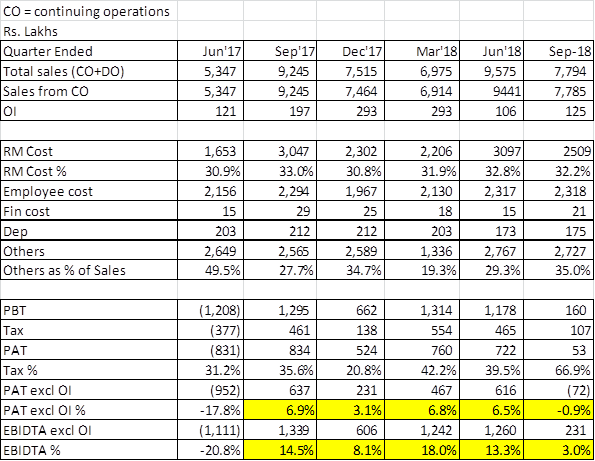

not so good results from albert. sales dropped by a lot both yoy and qoq. absolute amount of employee costs and other expenses remained same qoq. hence profits fell more. RM cost as a % of sales remained almost same both yoy and qoq. employee expenses are fixed in nature. other expenses is a combination of about 50% fixed and 50% variable expenses. the fixed expenses remaining same, caused big drop in profits.

company had indicated for soft quarter, and had said not to expect similar levels as Jun q in sales. Sep sales are similar in number to Dec17 and Mar 18 numbers. the high cost employees better start delivering on sales now.

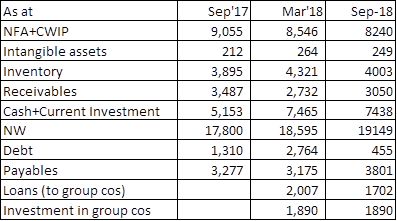

Balance sheet is fine. cash position has been maintained. Debt has come down significantly. Loans to group cos has reduced by 3cr over Mar 18. Need to see if they have a conscious plan to keep bringing it down.

This is definitely interesting.

The operating leveraging will also work in positive in a big way once sales starts growing.

The existing workforce has a union and can’t be fired, so it it taking some time.

Can any one help me understand why the sales went down so much?

Investing is simple but not easy. Results of ADL clearly prove this point. Very difficult to stay convinced when the very basis of “value” goes down. Though, I agree operating leverage cuts both way - so in case they are able to show 20-30% growth over next year or two, the bottom line should appropriate grow slightly higher. But only Hope is not the best strategy.

If any can share an idea on whether the sales decrease are one off or is it due to some structural issue?

It seems some of the sales was booked in last quarter.

The reason of profit wash out is higher cost base.

The management has hired new MR and created specialty wise divisions to build sustainable sales organization. The costs are front ended.

So, a small dip in sales has led to profits wipe out.

On the other hand, balance sheet is very strong.

The mkt Cap to sales is very low for a debt free company vs rest of the industry.

CRISIL has reaffirmed its ratings on bank facilities of Albert David Limited (ADL) at ‘CRISIL A-/Stable/CRISIL A1’.

2 key interesting points from the note:

Cash and cash equivalents stood at over Rs 5.97 crore and investment in liquid funds at Rs 68.14 crore, as on September 30, 2018. A substantial part of the liquid surplus is expected to be maintained over the medium term given no major capex in ADL or investment plans in any of the group companies, barring any exigencies. (in fact, in H1, investment has reduced by 15% over Mar’18 levels - remains to be seen whether this is one off or will reduce further, or go back up).

Upside scenario

***** Improvement in scale of operations and sustenance in operating profitability, while maintaining an adequate financial risk profile

***** Stabilisation of newly formulated marketing division (Division II) in nine states

(this is an important development, and most likely, the contributor to cost increase in Sep Q results. as the divisions stabilise, and sales start coming in, the high fixed costs would start working to the benefit of the company in terms of profits)

Albert david products being used in bulk at my place of work where thers is a daily opd of over 5000

Will be great if you can share more details - in terms of their product - who are main competitors , how is the efficacy of their products. Any feedback on whether they are getting more aggressive in selling, pricing etc. Has your place of work seen a increase in sales from their products?

Had got this from my doctor sister:

Albert David-Like all other pharmas they have a wide range of products including anti inflammatory, antibiotics, respiratory, wound healing, herbal uterotonics, laxatives and placental extracts

Their star product i suppose is only Placentrex. This is used mainly for deep wound healing process (eg burn injuries). There is no substitute product available for this product on the market and its indication although not a very common one but is such that when prescribed it cant be avoided.

The anti inflammatory anaflam range although good, has very tough competition in market eg are voveron (Novartis), Acenac (Medley pharma), Dolokind (Mankind pharma). These products although a bit costlier are more commonly prescribed and used

Their respiratory range also showcases products which are commonly available on the market with their competitors eg is Montair range of products (Cipla) and Infinair ( pfizer). Again these are in greater use then their Breaze range.

They do provide antibiotics but nothing special apart from those routinely available on the market.

The uterotonics are herbal based and usually these will have a comparatively smaller market (restricted group)

Laxatives, vitamin supplements available will have limited use and may not be forming major part in their portfolio.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/90bc1537-b3fc-45c3-91a6-590d11ed8400.pdf

update on sale of mandideep unit.

Extract:

2. Date on which the agreement for sale has been entered into: November 27, 2018;

3. Expected date of completion of sale/ disposal: December 10, 2018. Formalities with Madhya

Pradesh Audyogik Kendra Vikas Nigam (Bhopal) Ltd. (the lessor) are pending.

4. Consideration received from such sale/disposal: Rs.8,56,83,725/— (Rupees Eight Crores Fifty Six Lacs Eighty Three Thousands Seven Hundred Twenty Five only).

I am not sure whether the company will receive the entire amount of 8.56cr hereon (ie subsequent to date of announcement) or whether they have received part amounts earlier and have already accounted for it in H1-fy19 or FY18. Any idea?

Interim dividend of INR 7/Sh has been declared by Albert David. Record date 16-March.