Akums – Our Choice in India’s Pharma Growth: Domestic-Focused CDMO, Avoids Tariff Risk

Akums Drugs and Pharmaceuticals Ltd., incorporated in April 2004, has established itself as the largest contract development and manufacturing organisation (CDMO) focused on the Indian pharmaceutical market. The company’s operations span more than 60 dosage forms, covering a wide spectrum from solid orals and syrups to injectables, hormones, nutraceuticals, and cosmetics. Its footprint is broad: 11 manufacturing plants across Haridwar, Kotdwar, and Baddi, supported by three R&D centres (two DSIR-approved) with over 970 DCGI approvals and 200 first-to-market launches.

Scale and Market Position

Akums’ scale and breadth allow it to service a wide array of dosage formats for an equally diverse client base, ranging from large multinational pharma companies to leading domestic brands. Its extensive manufacturing network, spread across multiple state-of-the-art facilities, enables the company to produce high volumes across therapeutic categories while maintaining flexibility in production. This multi-site capability not only enhances operational resilience but also allows Akums to meet varying client needs efficiently, strengthening its role as a preferred long-term manufacturing partner.

A Distinct Position in the Listed Investments Space

In the listed pharma universe, businesses with strong domestic exposure often command premium valuations, driven by the stability and growth potential of the Indian market. CDMO operations add further appeal through sticky client relationships, capital efficiency, and scalability. Akums combines these advantages with a revenue base largely derived from domestic operations, shielding it from tariff volatility and global trade disruptions. This combination of domestic market stability, embedded customer relationships, and sector tailwinds makes Akums a compelling proposition.

Unlike many peers, Akums offers a unique blend of scale, capacity readiness, and sector positioning. Its low export exposure not only reduces global risk but also allows it to focus entirely on the expanding Indian pharma ecosystem — a market benefiting from rising healthcare penetration, increasing chronic therapy needs, and steady branded generics demand. For us, this is precisely the type of business we want to own: entrenched in the right sector, benefiting from structural growth drivers, and trading at valuations that remain attractive given its quality and growth profile.

CDMO Growth Drivers

The Indian CDMO market is projected to expand from ₹14,500 crore in FY24 to ₹23,800 crore in FY28, reflecting a CAGR of ~13%. Growth is underpinned by increasing outsourcing from both Indian and multinational pharma companies, rising manufacturing complexity in specialised dosage forms, and a shift towards chronic therapy segments such as cardiac, diabetes, and CNS — areas where Akums already maintains a strong presence. Comparisons with global CDMO leaders like Lonza and Catalent illustrate the scalability of the model, although the Indian branded generics segment operates within different margin structures and regulatory frameworks.

Capacity and Operating Leverage Potential

Akums’ current utilisation, at approximately 31–39% in FY25, leaves considerable headroom for growth without material new capex. Historically, mature assets have delivered asset turns of around 4.8x, compared to the current blended figure of 3.4x, depressed by recent capacity additions. This under-utilisation suggests significant potential for operating leverage as volumes scale, creating a pathway for earnings growth beyond topline expansion.

Business Diversity and Competitive Moat

The company operates across multiple therapeutic categories, with over 60% of revenues derived from clients with relationships exceeding a decade. Such longevity reflects high switching costs, embedded trust, and operational reliability. A continuous pipeline of DCGI approvals and a history of first-to-market launches reinforce its competitive position.

Financial Profile and Valuation

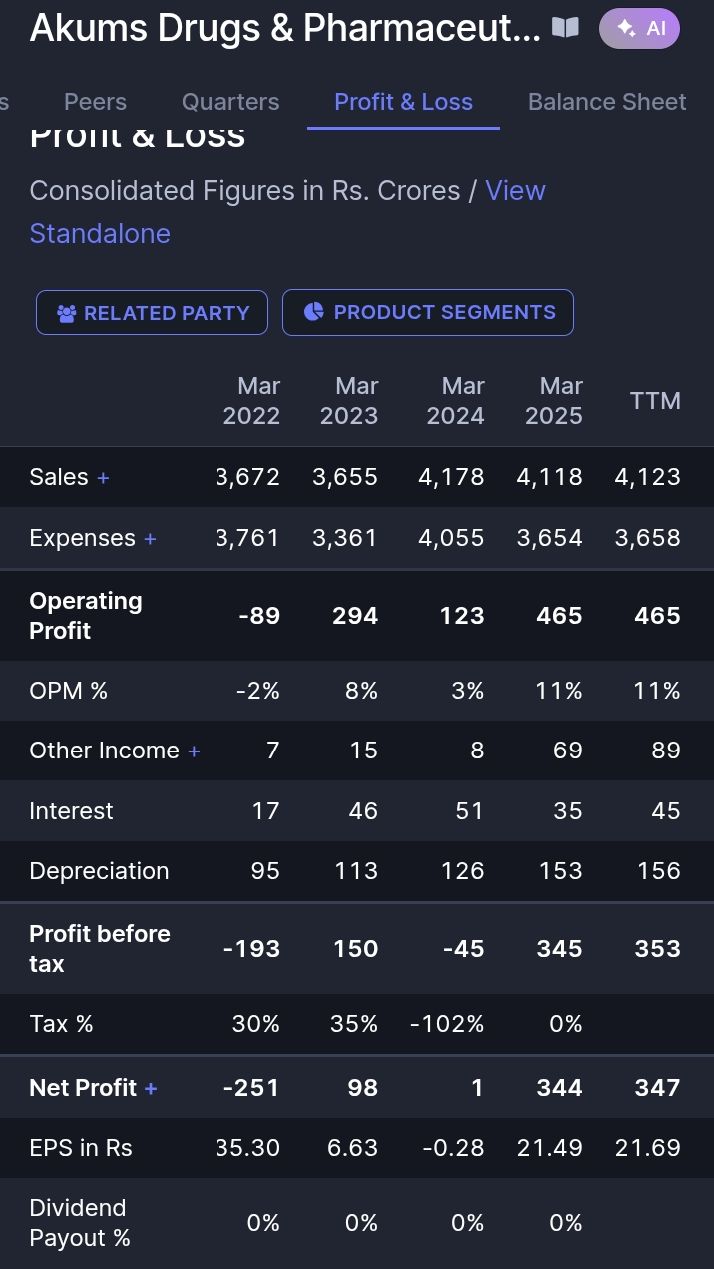

For FY25, Akums reported revenue of ₹4,074 crore and EBITDA of ₹503 crore. Over FY21–FY25, revenue and EBITDA grew at CAGRs of ~15% and ~12%, respectively. The company maintains mid double-digit ROCEs and a strong balance sheet, bolstered by cash from a significant biotech contract. At current levels, Akums trades at ~1.75x EV/Sales and ~14x EV/EBITDA — a discount to many global and some domestic peers, despite its market-leading scale and growth profile.

Risks and Overhangs

The overhang from an income tax inquiry into the promoters in FY24 remains a factor, though there has been no subsequent regulatory action. High promoter shareholding (over 75%) aligns interests but also concentrates control. Other risks include client concentration in the domestic market, competitive pricing pressures, and potential regulatory changes affecting domestic formulations.

Investment View

Despite these overhangs, Akums operates in the right sector, with industry leadership, strong client stickiness, and ample capacity to support future growth. Structural tailwinds in India’s pharma outsourcing market, combined with low utilisation and reasonable valuations, create a favourable setup for long-term value creation. We view Akums as a core portfolio holding — a differentiated play on India’s expanding pharmaceutical manufacturing ecosystem, positioned to deliver steady growth, margin expansion, and potential valuation re-rating as execution remains consistent

Disclaimer: This is a core portfolio position for us, built up over the last quarter with recent transactions in our Adezi Ventures family office portfolio. This article is not investment advice. Please do your own research. The views expressed here represent our investment perspective only.