DISCLOSURE: I hold quite a good quantity of Aksh Optifibre as a long term holding. The fundamental analysis of Aksh is from the blog of Mukesh Bhatia while the full write up of the problem area of Aksh i.e its share holding pattern and issue of GDR and FCCB is by me.

The two key raw materials, optical fibre and FRP rod, constituting 70% of cost of optical fibre cables are manufactured in-house. This makes Aksh as one of the most cost effective optical fibre cable manufacturer. Also, Aksh is now the largest FRP rod producer, supplying to all optical fibre cable manufacturers in 56 countries across six continents.

Manufacturing units: AKSH has two plants at Bhiwadi, Rajasthan for Fibre & Optical Fibre Cables. And one plant at Reengus, Rajasthan for Fibre Reinforced Plastic Rods (FRP).

Future Outlook: India today is at the threshold of breaking into the big league of digitized nations. With investments upward of Rs 450,000crores being announced in the recently conducted Digital India Summit and continued support from the State and Central Government, the optical fibre cable industry is looking for a bright future ahead.

Special initiatives such as the Digital India Campaign, Smart Cities, National Optical Fibre Network and renewed faith in the deployment of large scale Optical Fibre backbone networks by private telecom companies have upped the morale of the entire industry. The spread of technology through various channels will ultimately lead to the building of an efficient national network . In addition next generation technologies such as LTE and FTTx, which require last mile connectivity, would also propel the demand for optical fibre cables in the coming years.

Considering the huge demand for Optical Fibre Cables Company has approved an expansion plan that will see capacity expansion in its Optical Fibre and Optical Fibre Cable business at its existing manufacturing facilities in India. The FRP business is also set for expansion through its wholly owned subsidiary AOL FZE, Dubai. The Company will be investing around Rs.95 Crores for the expansion and setting up of additional manufacturing lines across all the facilities. The expansion is proposed to be funded out of debt and internal accruals.

Financial Performance:

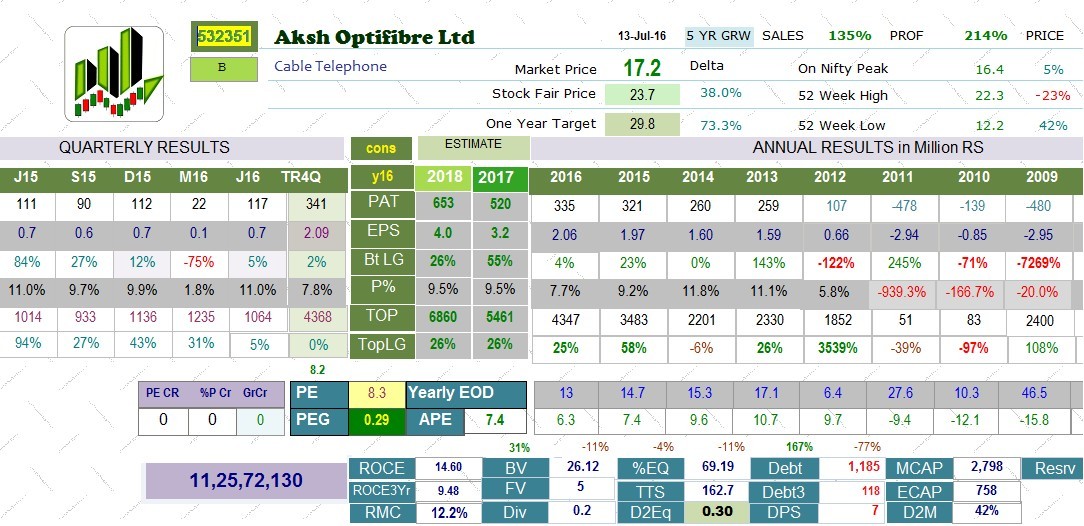

As per the below financial performance of last 5 years company has performed well in last 4 years and maintained profitability as well.

2016 2015 2014 2013 2012 2011

Total Income 448.8 354.13 227.49 240.21 194.02 12.36

Interest -11.56 -10.26 -7.06 -3.73 -5.35 -2.32

Net Profit 33.52 32.11 26.02 25.94 10.69 -47.81

EPS 2.14 2.18 1.75 1.77 0.75 -4.37

In the financial year 2014-15 there was a surge in demand of OFC, largely fuelled by introduction of next generation technologies and up gradation of existing 2G networks to make them 3G and 4 G compatible. A trend which is set to increase further in the coming year, with several Greenfield sites are being rolled out and more in the pipeline with operators preparing to launch 4G services, OFC network deployment is likely to gain momentum over the next few years making India one of the fastest growing markets in this segment.

India optical fibre cables (OFC) market is expected to grow robustly due to expansion of telecom infrastructure throughout the country over the next five years. Being the second largest telecom market worldwide, India exhibits high data traffic owing to increasing penetration of smartphones and growing demand for broadband services, thereby creating significant demand for OFC installations. Consumers are increasingly shifting towards internet driven applications like HDTV, video on demand and high-speed file sharing. To address the soaring demand for high speed data transmission, the government of India along with telecom giants is investing substantial capital in upgrading the country’s telecom infrastructure. The existing network of copper cables is being over hauled by using advanced fibre optic technology. All these factors are consequently providing a considerable thrust to the OFC market in India.

The demand of company product is truly reflecting in the company’s financial performance. The 2014-15 revenue increased by more than 50% and in FY-2015-16 the revenue increased by approx. 26% and net profit too increased.

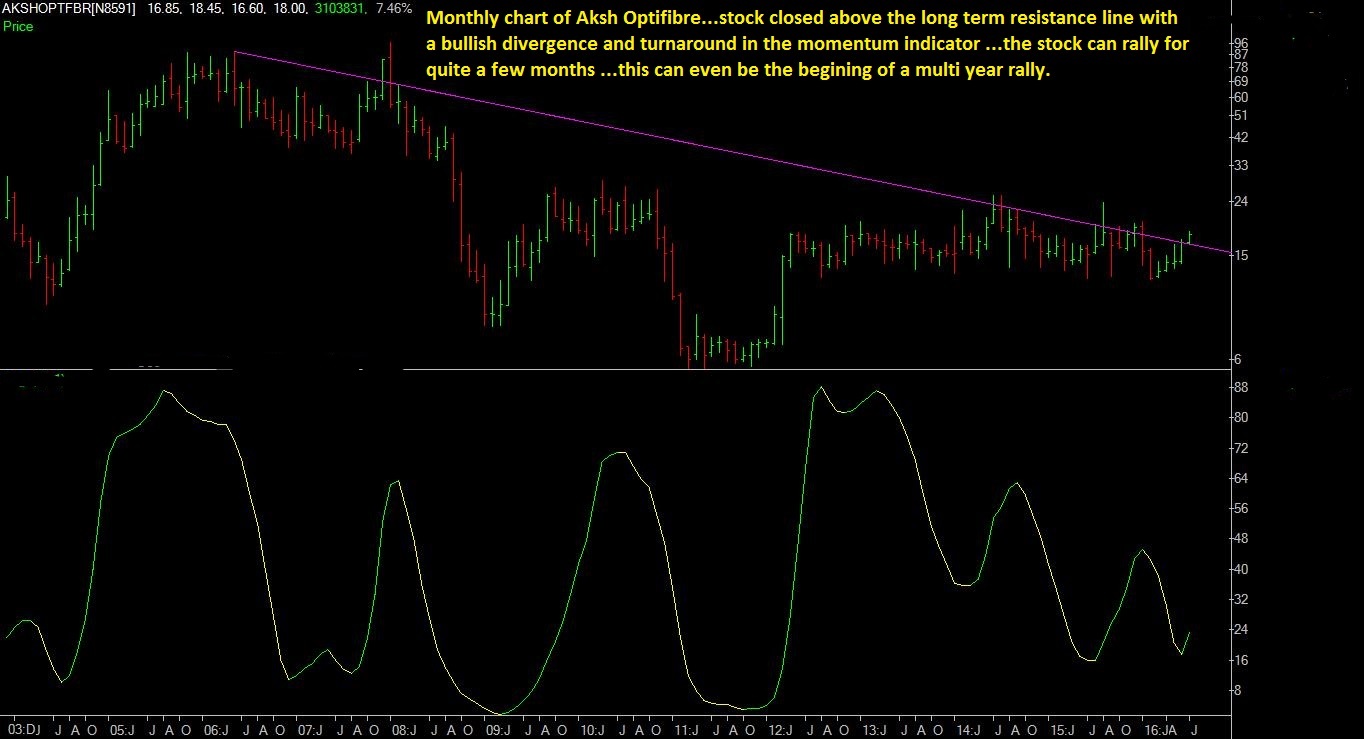

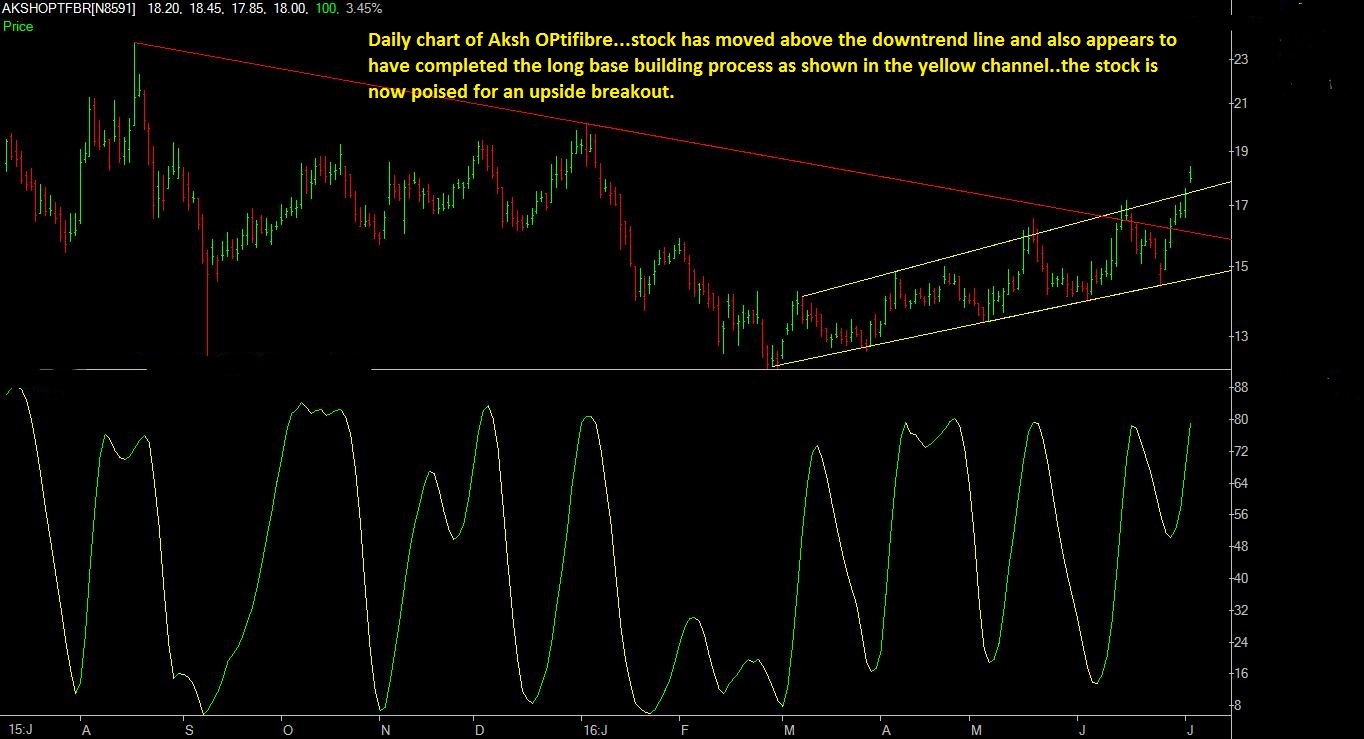

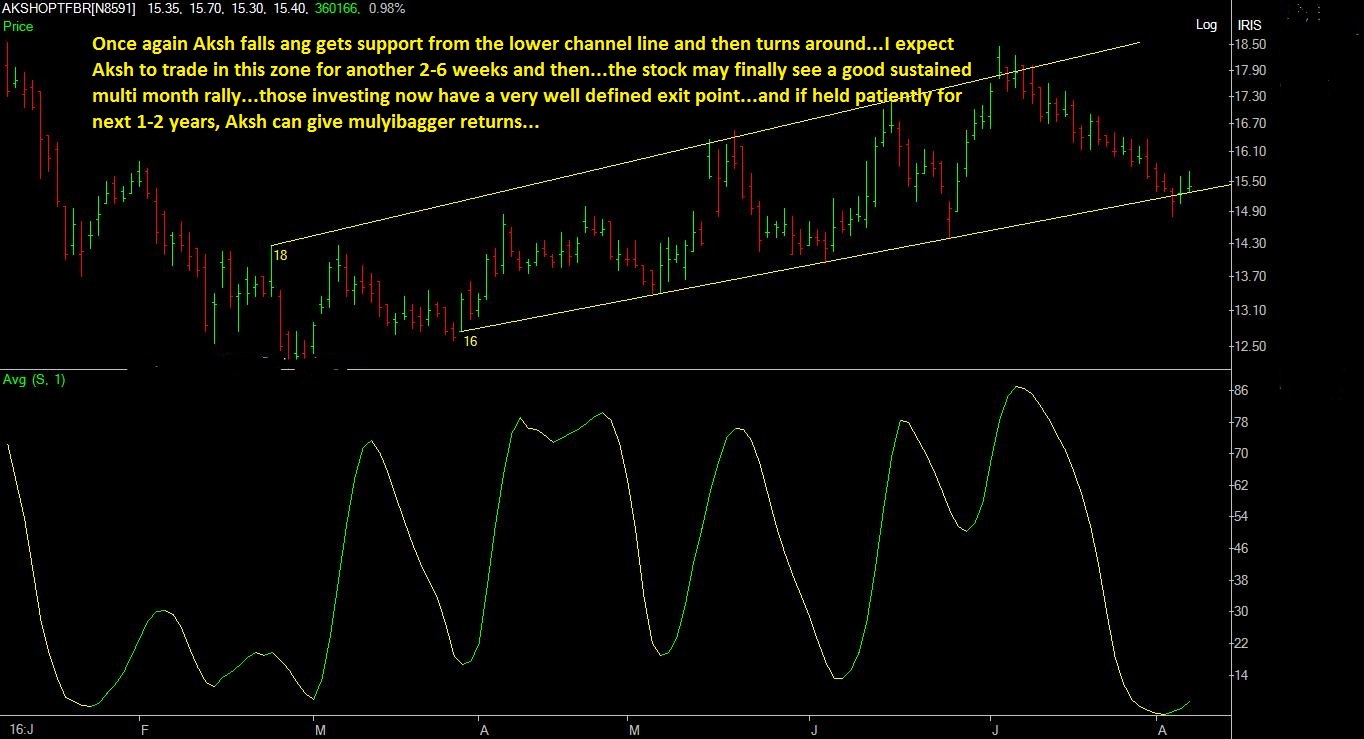

Share price valuation: Share is available at CMP of Rs 18 at a PE multiple of 8.4 .Technically stock had created highs of Rs 22.50 in the past and it can easily surpass the same in short run.

Fundamentally with continuous increase in demand of product the performance of company is set to improve year on year from here on.

SHARE HOLDING PATTERN – THE MAIN PROBLEM AREA IN AKSH OPTIFIBRE

GDR and FCCB CONVERSION OVERHANG IN AKSH OPTIFIBRE

About 1165750 GDR ( equal to 5.82 crore shares) were issued in Sept 2010.

And as reported in the Annual Report, as on June 2015 all the GDRs were converted into equity shares.And hence as of now there is no overhang of the issue of any GDRs

With regards to the FCCBs, Aksh raised 3.792 million USD in Feb 2014 by issuing 5 year duration FCCBs. On conversion, these FCCBs would amount to 1.41 crore shares. But the process of conversion of FCCBs into equity shares was started with in 4 months…when between June and Sept 2014 29.7 lakh equity shares were issued. The remaining FCCBs were converted into 1.11 crore equity shares between August 2015 and December 2015. The final conversion was effected on 7th Dec, 2015 and now there are no more FCCBs pending for conversion into equity shares.

Thus the issue of overhang of GDRs and FCCB conversion in Aksh is over.

UINQUE HOLDING ARRANGEMENT BETWEEN OFFICIAL PROMOTERS AND D.K.JAIN FAMILY OF LUXOR GROUP

With regards to the promoters group, Aksh shows a very special pattern. The company was started by Dr Kailash Choudhari in association with two very well established business families - the Fulchand family and the D.K Jain. While Fulchand who are well established garment makers ad exporters having the status of 5 star export house and interests in various other business joined Chaudhris as the co promoters; the other group headed by Davinder Kumar Jain who are the owners of the Luxor group (makers of Luxor pens) now style themselves as among non promoter investors (although in March 2002 D K Jain & Luxour Infotech Pvt Ltd are shown as part of promoters group along with Fulchands).

After the death of D.K Jain on 19th March 2014, through a convoluted method involving a proxy - Sunidhi capital Pvt Ltd, Usha Jain - wife of D.K.Jain (and now Chairperson of Luxor Group) stepped in place of her late husband D.K.Jain. This arrangement continues even now.

In Sept 2010, Aksh issued massive amount of GDRs (equivalent to around 6 crore shares) which caused the official promoters holding to fall by more than 50%. The holders of these GDRs were Bank of New York and Deutche Bank. Thereafter, from 2011 onwards, the Chaudhris and the Fulchands started increasing their holding in Aksh. And the increased holdings percentage of the two official promoters coincided with the reduction in the GDRs. Finally, in Dec 2012 Aksh came out with an open offer for 3 crore shares @ rs 7 per share and consequently the two official promoters acquired 2.84 crore shares (through open offer alone) from the GDR holders and the percentage holding of the official promoters again rose to around 30%. After, the open offer the share of the promoters was further increased on conversion of GDRs held by Dr Chaudhri into 62.5 lakh equity shares in June 2015.

On the other hand, the non official promoter - D.K. Jain started increasing his share in Aksh mainly from 2014 onwards. This period again coincided with the conversion of FCCbs into equity shares and also selling by GDR holders ( quantity remaining after open offer). BY end of June 2015, the unofficial promter Usha Jain was holding 2.4 crore shares.

SALE OF SHARES BY DR CHAUDHRI

In June 2014, 62.5 lakh equity shares were alloted to Dr Chaudhri on conversion of GDRs held by him. As a consequence, the shares held by Dr Chaudhri & family rose to 3.31 crores. And in Sept 2015, the Chaudhri family sold off around 30lakh shares. Coincidentally, during the same period, the number of shares held by Usha jain rose exactly by 30 lakhs…indicating that it was not a sell off by the promoters but a transfer from the official promoter to the unofficial one-Usha Jain.

Thus from the above, we can conclude that:

-

There is no dilution of the shares held by the promoters and allies. Their combined total holding is around 45%.

-

The whole purpose of issue of FCCBs of around 1.4 crore shares was to enable the promoters circle to accumulate shares through their benamis and to profit from a pump and dump sort of scheme.

-

Now that the overhang of GDR and FCCB is gone and the promoters / operators have picked up their required quantity of shares…and the results too have been good…it is a matter of time before the process of jacking up the share price starts.