Hi Valuepickr community,

I have been a part of this forum for a while now, but sadly I haven’t been as consistent with my investments. I have vouched to be more disciplined with my monthly investments as well as with my stock selection.

I started my investment journey 15 months back and after a gap of 8 months I am back.

My investment option is through monthly SIP’s on stocks with my income savings, and since I have built my emergency fund, I will be able to invest all of it.

I generally pick my investment ideas from Valuepickr, screeners and SOIC. Mostly I follow Valuepickr and in the lines of Mohnish Pabrai " Everything in my life is cloned…I have no original ideas ”.

I am still not sure what should be the best allocation strategy per stock, per sectors, the best strategy? Is long term the way to go or be a more techno-funda guy like a lot of people here? How many stocks to keep? Is it 3-4 names or 30-40 ?

As of now (and for the next 2 years) I have decided to invest into 20-25 stocks with allocation per stock ranging from 3-7% of my folio depending mostly on my conviction and will not go beyond 15% on a single stock at any point of time in future.

I will only sell a stock if there are sectoral headwinds or something fundamental changes in the company, which I hope I will be updated through ValuePickr.

Since the time I have started I have exited the following stocks-

- Laurus Labs (Still tracking through Valuepickr and Investor Presentation; had exited at a 20% loss a month back, as I needed some cash and I was unsure about the company prospects)

- HFCL (Exited on a 10% loss; had it since the start with the 5G and Defense theme in mind but results never reflected the “order book”)

- Yash Pakka (Exited on a 20% profit; in recent quarterly result revenue from their molded products did not show growth; prices might come down once paper cycle is over)

- HUL (Exited on a 10% profit; Took it as a swing trade months back)

- Dr. Lal Path (Exited on 10% profit a quarter back)

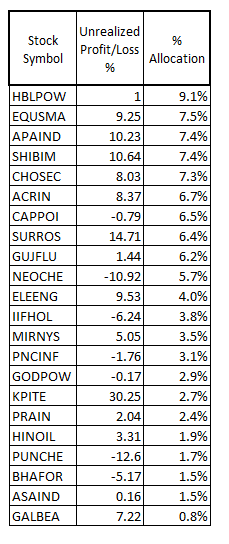

My current folio :

My current folio has 19 stocks which I intend to keep it in the range of 20-25 at any given point of time. I am still looking for ideas and the right price to buy some.

As I have been very sporadic with my investments, the per stock allocation is off the place and I will rebalance in the coming months and update accordingly.

Current Return on overall folio as on 09/02/2023 - (-1.20 %)

Companies and Current % Allocation:

Balaji Amines------5.60%

Deepak Nitrite----6.20%

UPL----8.00%

Vinati Organics—3.50%

Carysil-----16.30%

PNC Infratech-----3.60%

Surya Roshni----2.50%

Apar Industries-----3.50%

Rolex Rings----3.20%

KPIT----6.80%

GPIL----11.00%

SAIL----2.20%

Galaxy Bearings----1.80%

Bank Bees----1.10%

Caplin Point----6.70%

Divis Lab----2.90%

Cosmo Films----5.40%

Tata Power----8.10%

Avantel----1.50%

Rationale behind stock picks:

1.Well mostly like I mentioned before I have come across these companies through Valuepickr, screener and a few Youtube channels like SOIC. That is my first source of vetting companies.

2.I will try to balance my portfolio on individual allocation as well as on a sector basis but going forward at least for the next 1.5 year I will be a bit more inclined towards API/Pharma (Current holdings- Divis, Caplin, looking to add one), Specialty Chemicals/ Agri Chem (Vinati, Balaji Amines, Deepak Nitrite, UPL) ( Both these sectors seem out of favor now), Infrastructure/Capital Goods (Stocks like Surya Roshni, Rolex Rings, PNC Infra, Galaxy Bearing, Apar Industries, Tata Power are part of my Infra play), Defense (Currently I only have Avantel, rest big names either I have not build the conviction as of now and look expensive to me for eg Solar Industries, HAL, shipbuilding names), Financial ( I am confused on which 2 or 3 names to pick hence will go ahead with the ETF as of now).

Rest names that I have taken according to my limited understanding are undervalued like Carysil (Huge potential in international and Indian market; might pick up once Europe crisis ends), GPIL (Well came across this through screener and added it with time because of the extensive coverage @kumar_manas had on this company, Cosmo Films (Screener plus potential unlocking in value as I understand it is moving away from its commodity part of the business and the pet care business might be a big hit), SAIL (Will buy on dips; when it is around 0.4-0.6 P/B ratio)

As a safety net I have 10% of my folio’s total allocation on Gold ETF and will readjust the amount as my folio grows in the coming months and years.

I will be grateful if the experienced investors like @StageInvesting, @hitesh2710 bhai, @ranvir, @harsh.beria93, @Malkd, @basumallick whom I have been following religiously take a look at my current folio and suggest me on the way forwards keeping my constraint that I can only deploy money on a systematic basis monthly.