ASL was incorporated on 13th January 1992 under companies Act, 1956. The Company is engaged in the primary business of manufacturing of Vanaspati and various kinds of refined oil with shortening products for bakery like biscuits, puffs, pastries and other applications. Company is selling it’s products under three brands DHRUV, ANCHAL and PARV. Company has Vanaspati plant and refinery located in Alwar, Rajasthan.

Listed on Bombay Stock Exchange Ltd., the company went Public with the Initial Public Offering in the year 1993 with 162% shares fully subscribed. The company also issued Preferential equity shares in year 2012.

Financials

Market Cap = Rs. 56 cr.

For F.Y. 2016, Sales = Rs. 579.12 cr., PAT = Rs. 5.09 cr.

5 year CAGR in

PAT = 61.73 % (From Rs. 0.46 cr in FY2011 to Rs. 5.09 cr in FY2016)

Sales = 13.93 % (From Rs. 301.74 cr in FY2011 to Rs. 579.12 cr in FY2016)

Company has a very strong balance sheet, cash and short term investment as on 30.09.2016 are Rs. 50 cr. and short term borrowings of Rs. 2 cr.

Company has seen steady volume growth of it’s product in past three years.

2014 2015 2016

Prod.(Mt) 75441.978 89472.406 106271.921``

Sale (MT) 75411.978 89472.406 106725.205

Negatives

Very low ebitda margins. Though it looks like a norm across the industry, edible oil industry works on thin margins (Overcapacity and Competition).

No dividend payment in spite of cash rich balance sheet.

Corporate guarantee given of Rs. 70 cr. to bank for a non-listed promoter group company.

Promoters have various other business interests in reality, textiles and construction.

Contingent Liabilities totaling Rs. 130 cr.

Oil is extracted from Oil Seeds, MSP of seeds is decided by government. Slightly government regulated which may have effect on cost front.

Investing Rationale

It is a balance sheet play as the market cap is equal to the free cash in the company, negative working capital seems to be the source of cash. Core business is doing reasonably well and has shown good growth in the past 3 years and is likely to do well in the future as the company works in an import substitute sector (As per Annual Report 2016, India imports nearly 67% of its edible oil requirements). Will be interesting to see how the cash is utilised in the future. Will it be used for growth or will it be siphoned off from the company, remains to be seen.

From my quick scan Ajanta seems to one of the few companies which has at least has some returns on its capital to show ( which in this industry are not too great ). While the company seems to be terribly undervalued the economics of this industry ensures that you will not earn a decent return over a longish period of time because the underlying business itself will not earn that kind of return.

My personal preference is to avoid any packet that has the word “hydrogenated” printed on it so i would give this a miss. Passing hydrogen through palm oil at superheated temperatures and then trying to sell it is not a very profitable business

Ajanta soya is a mis-priced stock in the lower side. It sells edible oils in the name of its own brands…Terribly under priced in a country when branded edible oils penetration is very very low…Markets have to re-rate this stock up, sooner than later…It has marquee customers like ITC…

To my reading of the AR, things look OK in the management side…The co

has increased profits by 60% in last 5 yrs, has very strong cash flow…stk

languishes at 7 PE…

Sorry to hear that Vivek…That was not good manners…But it does not mean

the stock will not do well in the markets…Like HDFC Bank is so attrocious

to its customers by charging for every little thing…But great for

shareholders…

Maybe this chor is becoming mor. But sector also gets poor discounting. I am thankful for Ajanta owner in helping me identify chor run of the mill management

Ajanta Soya’s new state of the art factory inauguration is happening tomorrow in Bhiwadi. This factory replaces the one which burnt down and had been built at a cost of approx 25 crores. Out of which Rs. 20 crores is being reimbursed by the insurance company. Full production will start by first week of February. The share price was 94 in May when it crashed to 43 on the news of the factory burbing down. Apart from the temporary setback and bad last quarter, this has worked out very well for Ajanta Soya as it adds tremendous capabilities which were not possible in the earlier factory at zero investment . The new factory is completely financed by insurance + the depreciation benefits. The state of the art factory can now make many variants which are sold at much higher prices. These variants are used in all kinds of FMCG food products and Britannia, Haldiram and most big food FMCG companies there key clients. The OPM is generally low as the factory is mostly used for mixing the oils to get the right temperature profile. Oil and raw material is bought and the profits are normally shown in other income. However, this other income is possible only because of the factories mixing capabilities. Expecting a re-rating in the coming weeks as the market gets to know.

Hi Anuj , you have good insight. Do you have any insight in promoters & corporate governance ? Promoters holding has increase slightly in march 2018 Q. One of promoters - Angry goyal has increase his holding by 8000 shares but their is no SAST announcement in bse in this regards in entre Q. Also any insight on how new plant and state of business will be highly appreciated. Thnx

The tightening of the trans fat regulation by FSSAI is a big positive to Ajanta Soya limited (ASL). Refer the FSSAI announcement… While many manufacturers are finding it tough to meet the regulations, ASL seems to already meet the final 2%guideline.

The products of the company fare best in tests and this is probably the reason for a high pedigree of clientele including many MNCs like Pesico, ITC, Parle, Britannia etc (ASL’s website).

Seems with increasing demand for edible oils, ASL is poised to fare much better with its , strong Balance sheet, tight working capital requirements, High ROE of 20%+ and super Q2 results.FSSAI_News_TransFat_Hindu_04_01_2020.pdf (504.7 KB) Vansapti Ghee.pdf (1.1 MB)

Just, forgot to add that as per company’s announcement yesterday, ASL has undertaken capacity expansion which has been commissioned commercially.

The company’s expansion especially in premium bakery shortening segment is a positive as the demand is growing rapidly. The response to Mrs bector IPO reflects the huge upswing in demand bakery products and snacking produASL capacity expansion.pdf (395.0 KB) cts in post covid scenario with eating at home and QSR are increasing traction.

This stock showed up when I was searching for high inventory turnover ratio, low DRO and high ROE+ROCE.

The company had a terrific last couple of years, 2021 seems to be a blast from data on screener.in (i could only find 19-20 annual report) and it seems to be a beneficiary of the high cooking oil prices we are seeing (that doesnt seem to stop anytime). oldtimers on this thread, do you want to look see?

Surprised, by not to seeing much of recent discussions on this stock. The results for June quarter could be called ‘strong’. Companies’ all fundamentals appear to be in place. Generates very high ROE and ROCE. Promoter stake is increasing gradually in small proportion. Product mix is also decent and gaining market share (though very small currently). Some marquee investors are heavily invested in this stock. Things are really improving for Ajanta Soya.

Actually, Ajanta Soya ( ASL) requires Forex to import raw material (CPO mainly) for around 300 Cr (AR 2019-20 page 24 ). To import it requires to open “letter of credit” (LC) though banks which will ask for Bank Grantees (BGs) (which is a “non cash” exposure and can be in form of Bank deposits held lien/mortgaged).

Now, if we see carefully, they have these associate/KMP companies which are putting money on the block for Ajanta Soya (ASL). ASL has given Bank Guarantee on behalf of Dhruv Global for 68.1 Cr to banks AND in-turn Dhruv Global has given Guarantees to tune of 130 Cr to banks on behalf of ASL.

So, actually Dhruv Goyal and DG estates have a net exposure of 61.1 Cr (130 cr- 68.1 Cr) on behalf of the ASL.

Bottom-line: It appears that ASL has gained a “net net” support of 61.1 Cr in form of BGs support for its imports.

As per AR, ASL has investments both Dhruv Global and DG estates.

Why this is done? Dhruv Global is a garment exporter firm and has forex income (from exports) which can be used to support the “forex outgo” required for ASL imports (imports of CPO). This provides natural hedging of forex for both companies without any expenses. Infact ASL gains from it.

Disc: Invested. The above explanation is purely my assumption and reading.

My points/understanding from AGM held yesterday:

• Bank Guarantees:

o ASL has given bank Guarantee (of 68 Cr ) to related companies but in turn got bank guarantees of much more amount ( 130 cr) from these companies in favor of ASL.

o They are anyway applying to bank to get out of these bank guarantees.

• Company is in expansion mode. Plans to remain low on debt, hence, Free cash flows will be directed for fueling growth (increased working capital and Capex).

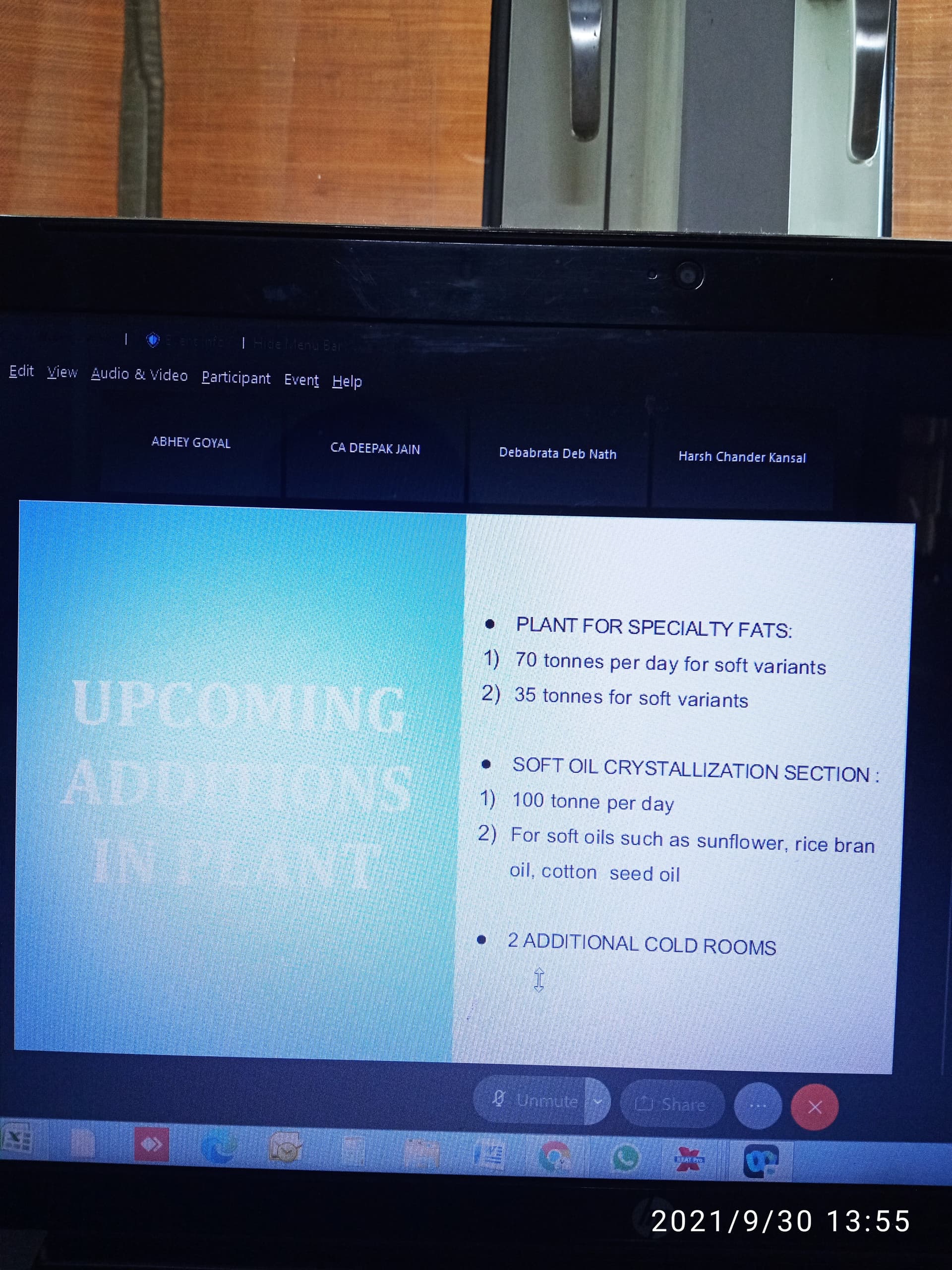

• They are planning new products “soft oil fats” of around 100 TPD. (As per my understanding these are used as table margarines as “low fat substitute” of butter.( see slide pic))

• The current financial performance trajectory shall continue in case there is no arrival of the third covid wave.

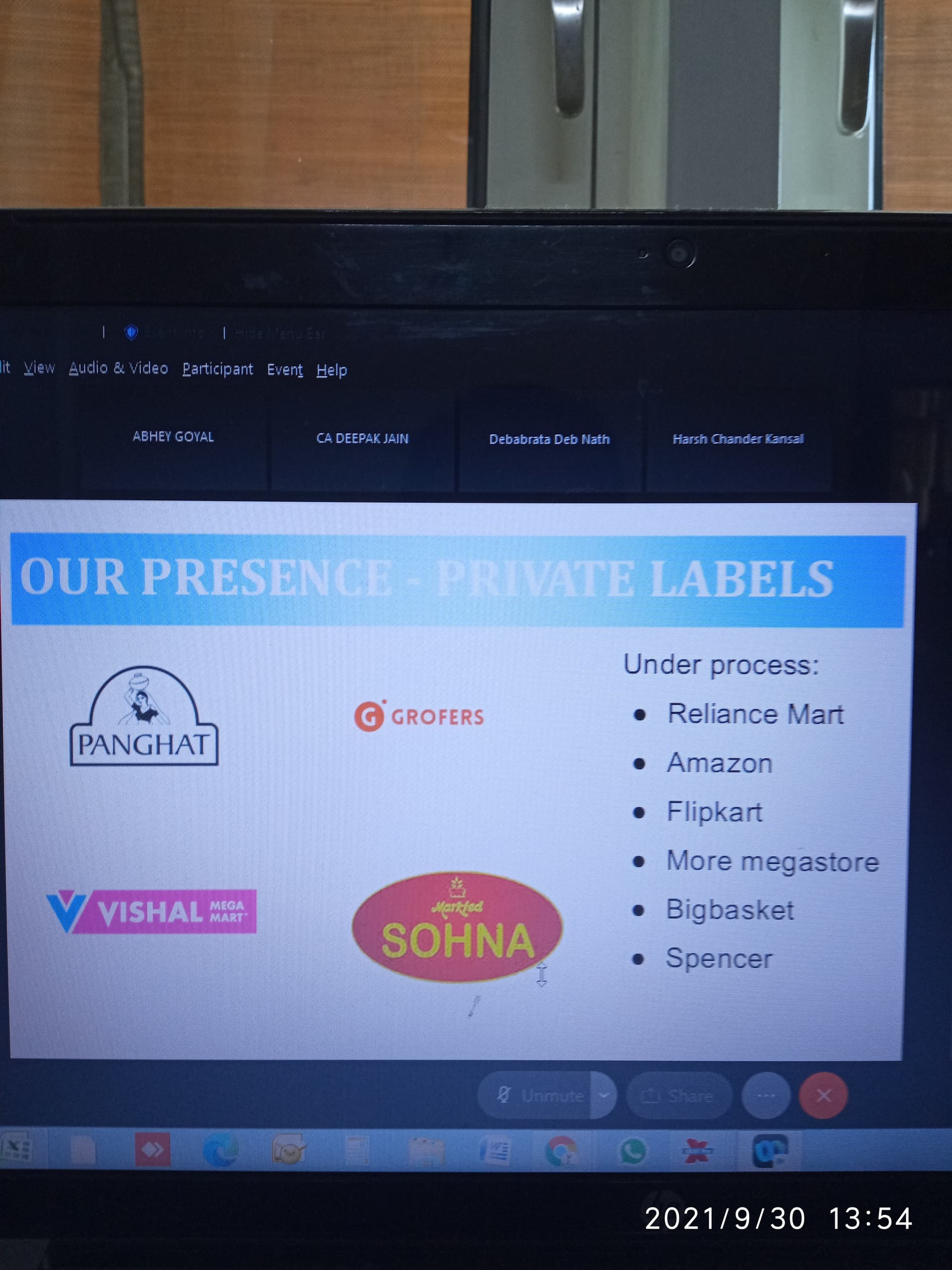

• To further deepen consumer market presence, they are “under process” for supplying items through e-channels (see slide). (they are already very strong in institutional sales)

• They have already have achieved <2% transfat regulation of FSSAI in their products, much before the due date of January 1, 2022.