The biggest overhang at this point of time is the tax liability and any retrospective tax claims going ahead. Although the management has clarified, still a couple of quarters will make things more clear.

After showing a steady increase in operating cash flows over FY08-FY11, it has contracted in FY12. Given the heavy capital expenditure ahead, free cash flow generation might be under pressure. Also dividend payout will remanin muted till capex phase continues.

Muted bottomline growth for next two quarters despite high topline beacause of tax impact. Hence, on increased base of H2FY12, bottomline growth would be lower. (If we consider the 15% EPS growth for FY13, of which much higher growth has been booked in H1FY13 aided by lower base and lower effective tax rate)

All in all, fundamentals hold good. Will hold and add on dips below 360 and lower. No rush to add at this level. Recently added more of Unichem and looking to add further.

I think broadly company can achieve the consolidated figures you have projected with a chance of positive surprise looking at the momentum shown in first half.

On that basis, at a projected EPS of 40, stock currently is available at a PE of 9-10 which seems very attractive for a company which has shown exemplary growth in the past 5-6 years and is likely to keep growing at 20-25% CAGR over next few years.

**

**

The only worry here would be to see if there is any retrospective tax levied on the company – management has categorically denied in your talk with them and I would tend to accept their version because till now except rumours of tax raids we dont have anything facing us.

**

**

Once the stock starts showing some momentum all these things and worries will be forgotten and people usually flock in to buy growth stories available at reasonable/cheap valuations.

Consistent promoter buying from markets inspite of very high promoter stake gives additional comfort.

**

**

I think Ajanta can be a very lucrative takeover candidate for any big company though this should not be a thesis for buying into ajanta.

**

**

Personally after having exited at 415-420 levels post q2 fy 13 results when the tax worries came about, I have re entered recently because for me the only concern is any retrospective tax on the company – I am not too worried about higher tax rates going forward looking at the growth momentum shown.

**

**

So in answer to ur query, answer is yes, currently it looks good for fresh allocation also.

I have been going over Ajanta Pharma over last couple of weeks and just kicking myself for not being able to catch up on this story properly despite in-depth discussion here

Considering the brands the co has along with good rankings in some of them, the stock looks attractive at current valuations. Usually such cos trade at 15 time PE by markets. If they are able to maintain 25% CAGR, the stock should do very well and also see a re-rating.

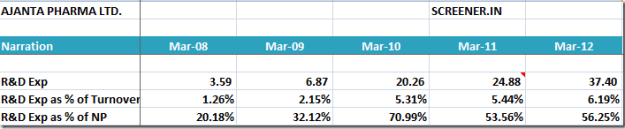

Among the recent developments, haven’t been able to figure out on the tax issue. Considering the huge R&D they do and 200% tax exemption available to the same, why should tax pay-out be 30%?

Anti-Malarials (Artefan a Artemether & Lumefentrine)

Gastroenterology (Lafutax a Lafutidine)

Male Erectile Dysfunction (Kamagra a Sildenafil Citrate)

In the Dermatology segment, the company ranks 18th and has 34 generic brands a with 4 leading brands and more than 10 first-time products. In the Opthalmalogy segment, the company is ranked 7th and has 30 generic brands a with 9 leading brands and more than 16 first-time products in India. In the Cardiology segment, the company ranks 31st and has 51 generic brands a with 3 leading brands and more than 6 first-time products in India.

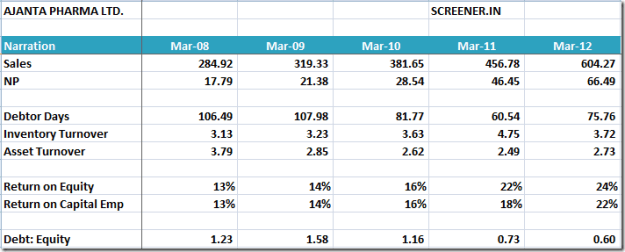

Over last 3 years, things seem to have really changed for the company.Ajanta is growing at about 25% CAGR nowand at the same time itsimproving its operating margins, reducing loans and bringing working capital efficiency. Hence theROE has improvedfrom about 15-16% in earlier years to about 24% in 2012. The markets have noticed the same and the stock has been re-rated from usual 5-7 times PE multiples to about 10 now. However, we feel that given the strong branded formulation play and good rankings in several segments, the stock is available at a reasonable valuation considering the high multiples enjoyed by the pharma sector (Industry PE 26).

Here is a snapshot of improvement in key ratios:

Another very noticeable thing in the company over last few years is the huge outlay on R&D. The company is now spending close to6% of its turnover on R&D expenses:

Usually a R&D spend of 2-3% of turnover is considered good and anything above it in the right direction can be very positive.

As per FY 2012 annual reportof the company, the company expects the current capacities to peak out in 2 years and hence they would be needing fresh capacities. Co has chalked out an expansion plan of 400 Cr.They have planned two separate manufacturing facilitiesa one for regulated markets & other for domestic and emerging export markets.

Hence considering the growth prospects and leadership position of the company in several segments, the stocks looks attractive at CMP of 385 for long term investing.

Thanks to Hitbhai, I have been holding Ajanta from lower levels. But, your post is an eye opener for me and I thank you for it. I have not added to my existing positions - I guess due to price anchoring syndrome. To know that you are entering Ajanta at these levels really made me realize that I need to re-look at the stocks that I already have and do better analysis as opposed to looking for more stocks to add.

Ajanta Pharma’s results out. Looks like a blockbuster results. YoY basis Topline at 229 Cr Vs 164 Cr +40% while bottomline at 32.57Cr Vs 18.51 +76%. This is despite higher taxation at 33.3%.

Usually the last qtr is the best qtr for Ajanta and likely to post eps of 15-18 and that makes full year eps of 47-50. Giving PE multiple of 12 for the kind of growth it is delivering, makes the possible price target of 565-600. Good to note that the exports contributed 69% of the topline. The stock has hit 20% circuit at 491.

amazing results by ajanta. i still remember management was guiding for 20% growth rate for the next 2-3 years. this is another case of management underpromising and overdelivering similar to mayur. ajanta should now be a core holding for any long term portfolio.

Fantastic nos from Ajanta…the co continues to surprise on the upside. During my post, I was thinking that 200Cr for Q3 would be good while they have done 230Cr !

Was lucky to get some just after the results yesterday

At this price too, it does not appear expensive at all. I think it deserves a PE of 15 and that gets us to a priceof 700 by March/April. Great find from Hitesh bai.

ideal time would be to buy once this volatility settles down. currently there is big variations in prices intraday to the tune of 30-40 Rs. It seems to have become day traders favorite stock from the look of things.

In a few trading sessions I expect the stock price to settle down in some small range with low vols. That should provide a good entry or accumulation point.