Hello folks, this is my first thread on this forum. I invite all the respected seniors like @phreakv6 ,@hitesh2710 , @rupaniamit , @harshitgoel etc and everyone else to go though it and share their views on my analysis and the company.

Looking forward to hearing from you guys.

Company Overview

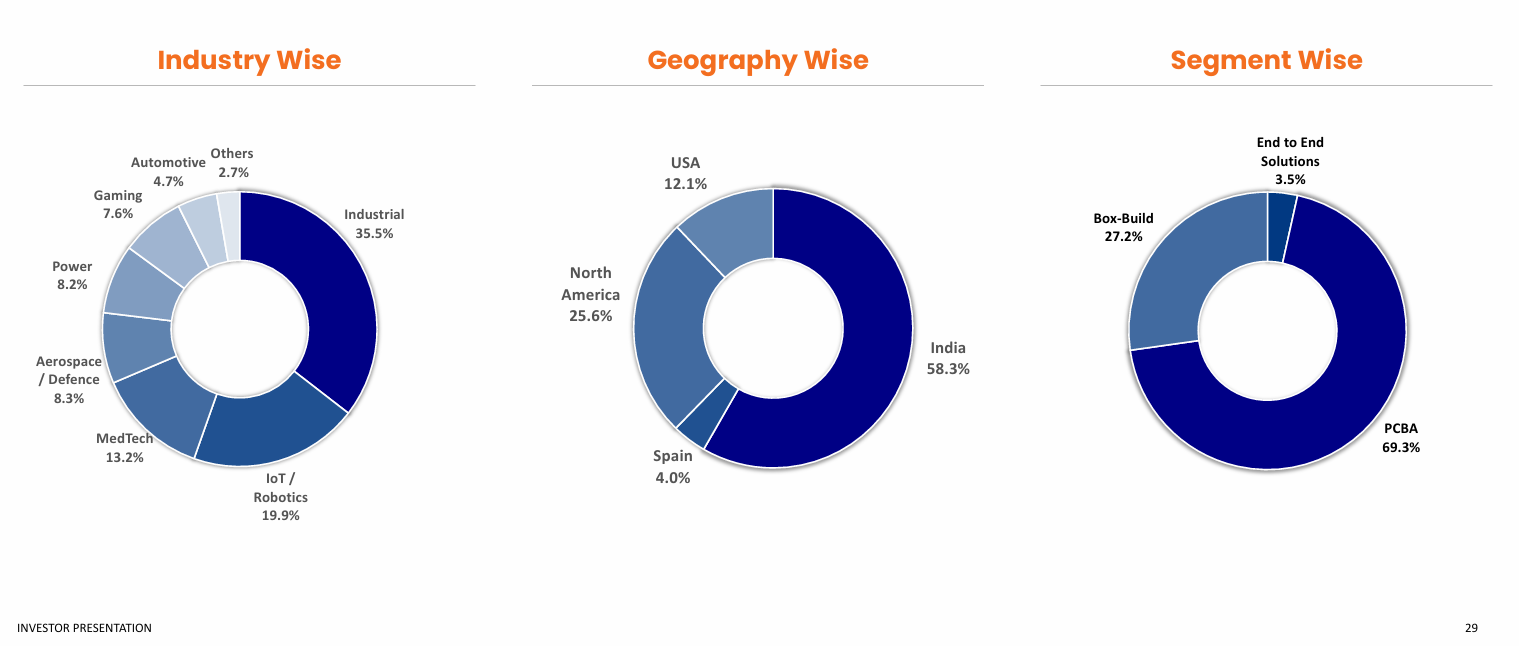

Aimtron Electronics is an India-based EMS (Electronics Manufacturing Services) SME specializing in high-precision PCB design, assembly and box-build integration. It offers end-to-end solutions—from initial PCB design through to fully assembled electronic systems (including EV battery management systems)—for global OEMs in IoT/Robotics, MedTech, industrial, telecom, aerospace/defence (drones), power and other sectors.

Key Facts

- Manufacturing & R&D: Two plants (Vadodara, Gujarat; Bengaluru, Karnataka) plus R&D/design centers in both locations.

- Incorporation & Listing: Founded 2011 (Pvt. Ltd.), converted to public in October 2023 via SME IPO.

- Promoters: Mukesh J. Vasani, Nirmal M. Vasani, Sharmilaben L. Bambhaniya.

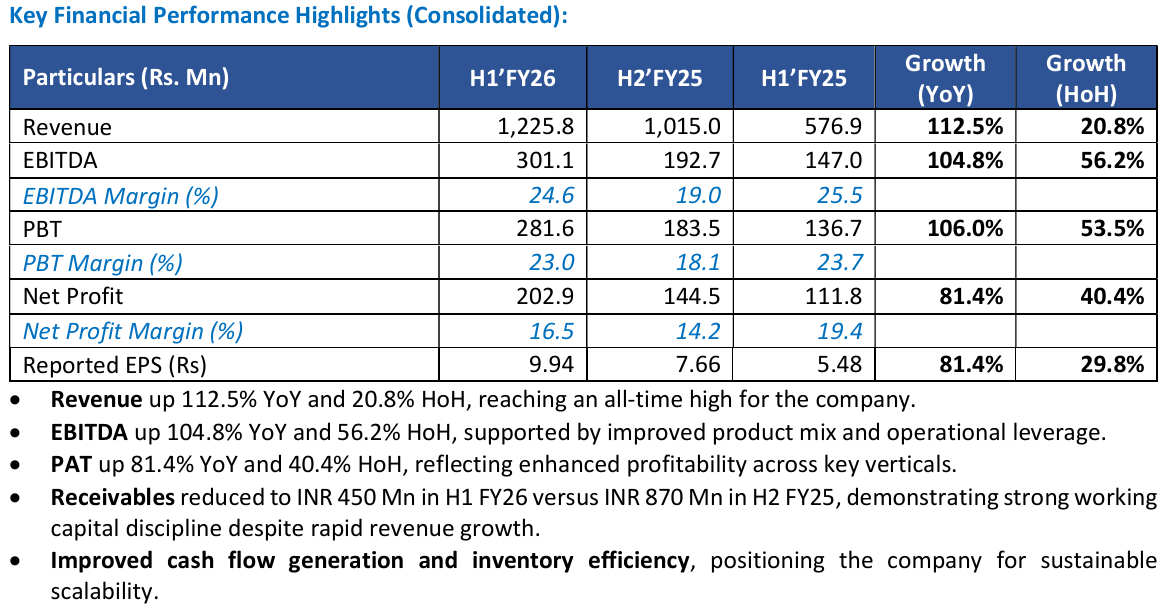

- Revenue Growth: FY23 +217%, FY24 +11%, FY25 +71%.

Product Portfolio

Key Concerns & Clarifications

- SME Status & Governance

- As an SME, some investors worry about governance risks.(Nuvama Analysts also visited company’s Vadodara facility and interacted with the mgmt, which also raises investor confidence in the company.

- We performed extensive checks (audit reports, SEBI filings, related-party disclosures) and found no material red flags—but no audit can ever guarantee zero risk.

- Inter-corporate Loans: Advances to related parties exist (e.g., Aimtron Electronics LLC, Texas), accounting for ~20% of FY25 revenue. These are disclosed and ring-fenced, but warrant monitoring.

List of Related Parties (From AR)

Accounting Policy Changes

- In H2 FY25, the company revised certain accounting policies, affecting margin comparability both half-on-half and year-on-year.

- Management states these changes better reflect the business’s true economics; disclosures adequately explain the rationale.

Receivables Spike & Cash-Flow

- Receivables rose sharply in FY25 due to clients delaying payments and asking for early delivery amid US-tariff uncertainty, though ~50% of the March 31 balances have since been collected.

- Management highlights a zero-debt balance sheet, which should ease working-capital funding despite higher receivables.

US Tariff Uncertainty

- With ~60% of revenue from the US, tariff changes pose a risk.

- Management argues that “China + 1” supply-chain strategies will favor Indian EMS players, cushioning Aimtron against tariffs.

Investment Thesis

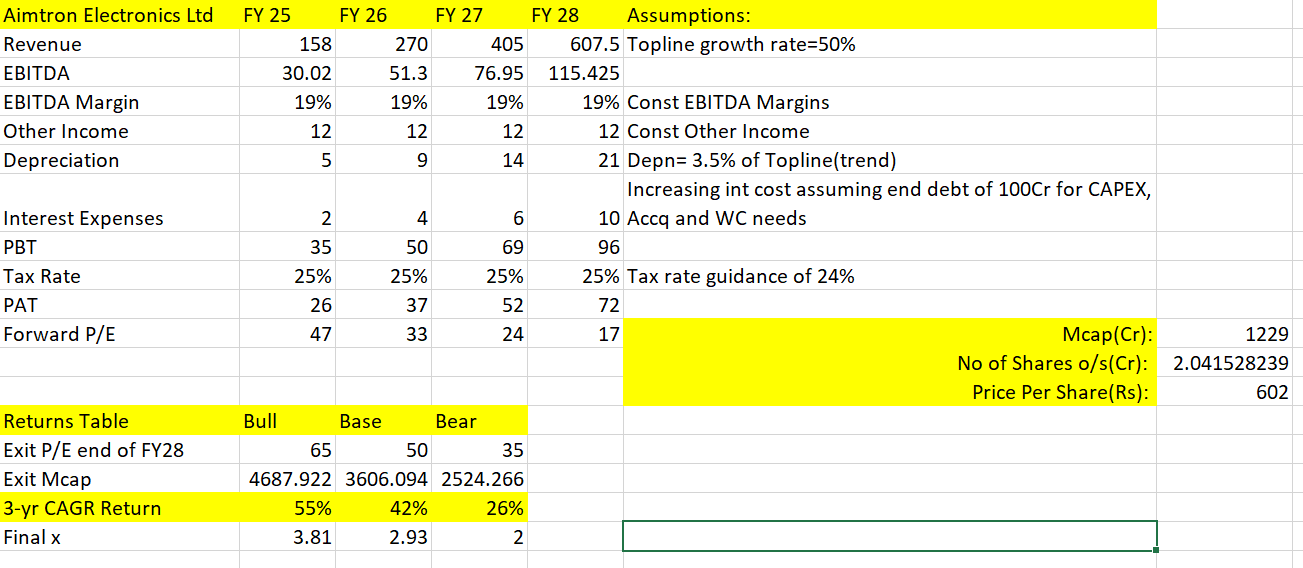

- FY25 Revenue: ₹158 Cr

- Current Capacity: Supports ₹450–500 Cr topline without further capex.

- FY26 Guidance: ₹270–280 Cr (we believe 300 Cr+ is achievable).

- Order Book: ₹189 Cr at FY25 end (up from ₹135 Cr in H1); additional orders in April push it to ~₹275 Cr.

- Enquiries: ₹800–1,000 Cr pipeline; win rates of 20–40%.

- Growth without Capex: At a ~50% CAGR, no new capex required until mid-FY27. Post-FY27 growth may need debt or equity infusion.

- Financial Model (FY26–28):

- Assumes 3.5% depreciation of revenue, 100 Cr debt @10% interest to fund growth.

- Projects FY28 revenue ₹607 Cr (50% CAGR) and PAT ₹72 Cr.

- Valuation Upside:

- At current ~50× P/E, FY28 P/E falls to ~17×.

- Even using conservative exit multiples (35×–65×), investors could see 2× returns over 3 years in a bear-case scenario.

Anti-Thesis Pointers

- High EBITDA Margins vs. Peers

- FY25 EBITDA margin fell to 21% (from 25% in FY24) due to mix shifts.

- While peers like Cyient DLM and Avalon report ~9%/5% EBITDA/PAT, Aimtron’s high margins may be difficult to sustain at rapid growth rates.

- Scalability Constraints

- To maintain ~50% growth beyond FY27, Aimtron must raise capital. Promoters prefer minimal dilution, so debt may increase leverage and risk.

- Niche manufacturing expertise may limit rapid scaling.

- Raw-Material Sourcing Risks

- ~70% of RM is imported. Geopolitical or logistical disruptions could significantly impact operations and margins.

Final Verdict

The Indian EMS sector enjoys strong tailwinds—government incentives, China + 1 shifts, rising domestic demand and competitive labor costs. Aimtron combines these secular trends with best-in-class profitability and a clear growth path. While governance and related-party loans merit watchfulness, no major red flags have emerged.

At present valuations, Aimtron offers an attractive risk-reward profile. Its growth targets appear achievable with existing capacity, and even conservative cash-flow projections imply multi-bag returns over three years. Investors should, however, monitor receivable collections, tariff developments, and capital-raising plans closely.

Disclosure:

For complete disclosure I am not currently invested in the company, but am thinking strongly about buying the stock. But this is not a buy or sell recommendation, kindly do your own research.