The contract win is great and very positive in many respects. My only concern wrt this company is that most of the revenues for the company come from the pesticides which the government is planning to ban. Although the company is trying to take a detour from these products by taking approval for substitute products from its customers, there will definitely be a big short-term impact as the approvals for new products are a time-consuming process.

I thing company is moving towards contract manufacturing.Beside this company will also focusing on new molecules. Contract manufacturing is a low margin business on the other hand new molecules will take time to capture the market. Company is on Wright track I suppose. In concall they sound confident of achieving 400 - 450 cr sales in next financial. Key will be double digit margin. Due to high commodity prices it is difficult to achieve but I think they can.

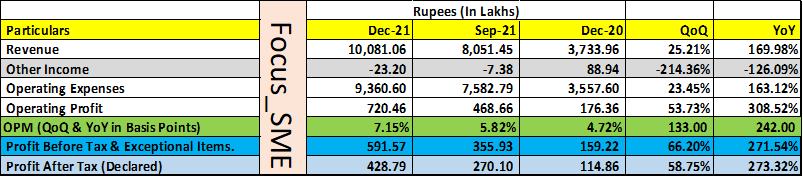

The journey continues. Now the company is debt free. In Q1 2023, EBITDA has improved to 7.1%. Topline is growing at a very decent pace. In the current FY, topline may surpass 350 crores. Based on 7% EBITDA, eps maybe somewhere around Rs. 16/-. Capacity expansion is likely to contribute from Q3 2023. aimco.pdf (6.9 MB)

At 200 Cr. Market Cap, the company look fairly valued.

[Disclosure- Invested]

*Company manufactures a total of 11 molecules in various categories; some key products are Chlorpyrifos (Ethyl & Methyl), Triclopyr, and Bifenthrin

Company is Debt Free

Technical grade revenue contribution is now 70% of the revenue (Formulations 14% , rest is trade )

Technicals Capacity is going up from 4,500 to 6,000 (Mostly debottlenecking ) , will start contributing from H2 FY23

Technical grade agrochemicals are sold to formulators in India & across the globe. Key global markets include Australia, Africa, Brazil and the United States of America.

Formulations are sold in bulk to marketers globally and marked directly by the Company under its brand portfolio. Some of the key brands are Anaconda, Pyriban, and Bykill

Growth is mainly from Contract Manufacturing of Technicals for other agchecm companies (like UPL ?)

They have long term 3 year agreement for contract manufacturing

Chlorpyrifos (product end of life) is completely phased out of production

Aiming to get registrations for new products this FY

The company has received environmental clearance for new manufacturing unit for synthetic organic chemicals. d5fc9c59-7284-4ba0-a438-a45844fbb10a.pdf (309.3 KB)

In a difficult FY, the company has received decent credit rating.

From the credit rating reports, it has come to notice that branded formulations now consists of 29% of the sales, whereas technical formulations stands at 59%. Thus almost 88% sales of the company is likely to be decent margin products. Quoting from Credit Rating report:-

“The company is into manufacturing, marketing & exporting technical grade chemicals & formulations of Insecticides, Fungicides and Herbicides. The revenue to the extent of around 50% is from exports. The product portfolio consists of 11 technical grade chemicals, 90+ formulations, 300+ branded SKUs. Technical constitute around 59% (vis a vis 70% in FY22), contribution from branded formulations was 29% in FY23 vis a vis 22% in FY22, contribution from B2B formulations was 9% in FY23 as compared to 2% in FY22. The company has obtained license/registrations for 200+ products & expects to grow over a period.” 202307120755_Aimco_Pesticides_Limited.pdf (156.4 KB)

[Disclosure: Invested and Biased]

Yah, rating has been downgraded. In fact last year it needed substantial short term borrowing, and despite that the downgrading is not substantial.

In any case the market is valuing this company as almost bankrupt.