My research notes on AIA. Have picked few points from this thread as well & credit goes to respective persons -

@rajpanda, @aveekmitra, @hack2abi, @punitm306

PRODUCTS

High Chrome Mill internal products that are used for crushing/grinding

Cement

The company supplies - grinding media, shells liners & diaphragms for this industry.

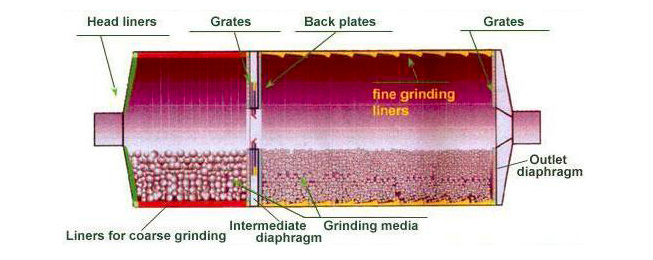

Tube MIll Parts

Following diagram explains the usage of various tube mill parts -

Vertical Mill Parts

The company provides grinding rolls for vertical mills. The company claims to have improved abrasion properties of these rolls resulting in cost savings. The company claims to have improved metallurgy of grinding rolls in following client mills - Loesche, Polysius, Atox, E, Raymond, CE

The company also provides - HRCS castings & crusher parts.

Mining

Tube & Rod Mill Parts

The company provides grinding media, inlet/outlet head liners, shell liners & diaphragms in this segment. The parts are customized for different metals that are being mined.

A similar assortment of products is provided for power sector as well.

Also company provides services like - Mill Audits, Installation Supervision, Mill optimization etc.

Grinding media needs to be replaced every 30 days whereas liners need to be replaced every 2-3 years.

INDUSTRY & CUSTOMERS

Cement

AIA is global supplier of mill parts in cement industry in Europe & North America.

In FY11, company started supplying vertical mills parts to China cement industry.

The global demand of high chrome mill internals for cement is pegged at 0.3 million tonnes per annum.

The global client list includes - Holcim, Lafarge, Heidelberg, etc

The company serves the cement industry in domestic market as well.

Mining (60%+ revenue)

AIA supplies mill parts to Iron, copper, gold, platinum & zinc mines in various counties like USA, Canada, Brazil, South Africa, Australia, Philippines. The global replacement demand in mining industry is pegged at 3 million tonnes per annum & only 10-15% of the demand is converted into high chrome.

The focus of the company in mining industry is predominantly outside India. The company sells products to companies like - Rio Tinto, Anglo American, BHP Billiton, Vale, Arcelor Mittal, etc.

Utility

Company also serves coal powered thermal power plants in India.

The list of customers include - NTPC, SEBs, BHEL, Doosan, L&T, Hitachi, Alstom etc.

SALES & MARKETING

Worldwide presence in 120 countries through front end marketing companies.

S&M Commission Expenses - 20Cr+

COMPETITION

Magotteaux – 350K MT, Anhui – 12K, Estanda – 8K, Christian Pfeiffer – 7K

Manpower cost too high for foreign players, freight cost is not an issue.

Forged players also form competition & falling forge prices pose challenge.

STRENGTHS

-

Replacement products - these products are repetitive in nature as against one time nature.

-

Stickiness - Once customer moves to chrome (takes 2-3 years), they stick with chrome due to tangible/intangible benefits.

RISKS

-

Lower commodity prices poses a question for survival of various metal mines. This also naturally holds back investments from mines. But on the other hand, increasing RM prices can hit OPM.

- The major growth driver for growth in company is exports markets. This seem to have slowed down in FY15, FY16. (Need to figure out why?)

- If some other technology other than high chrome metallurgy provides mill parts with longer life/lower cost, that would be disruptive.

SUBSIDIARIES

- Welcast Steels Limited (71% stake)

- Vega Industries (Middle East) FZE, U.A.E.

- Vega Industries Ltd., U.K.

- Vega Industries Ltd., U.S.A.

- Vega Steel Industries (RSA) PTY Ltd.

- Wuxi Weigejia Trade Co. Limited, China

- DCPL Foundries Ltd.

GROWTH AXES/ENABLERS

- Conversion to high chrome parts

- Mines for newer metals

- Geographical expansion in India & Abroad

- Commodity upswing

MANAGEMENT

Bhadresh K Shah - Managing Director, B. Tech Metallurgy, IIT, Kanpur

The company seems to be one man army riding out on the talent & skills of Bhadresh K Shah - an IIT graduate. His age is 60+ & prudent succession planning is required for future growth of the company.

Mr. Sanjay Majmudar, Independent director

Independent director yet quite hands on.

Dr. S Srikumar, Director

Common director with powertec & company uses powertec services.

Yashwant M. Patel, Whole Time Director

Closing in on 70, salary is just 7-8 lacs. Can’t figure out - what does he bring to table? wisdom?

Mr. Kunal Shah, Executive Director, Finance

Working in company in last 14 years. Intelligent but very direct in communication.

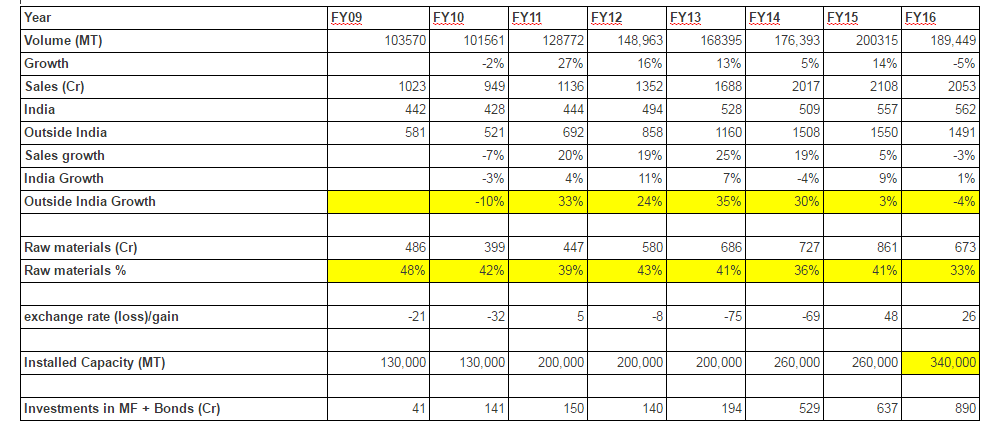

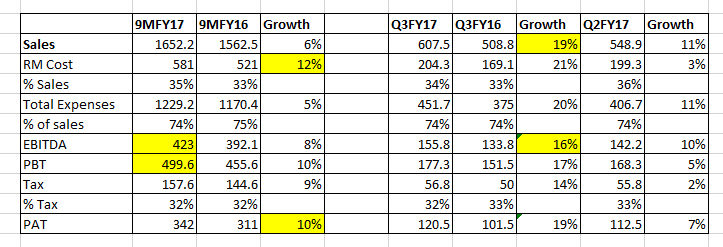

NUMBERS

MISCELLANEOUS

- The legal & consulting expenses are consistently high - 10Cr+ since FY10

AR FY10

- Added 22 new customers in cement business

- Started supplies to - Platinum mines in South Africa, Iron ore mines in Brazil, Copper mines in Africa, Gold mines in Far East.

- 45 - 55 sale ratio for India - Outside India

- FII + Mutual Funds already hold 30%

AR FY12

- OPM shrank from 24% to 21% mainly due to increase in raw material cost (447 Cr → 580 Cr) & 31% increase in other expenses (373 Cr → 489 Cr – 20Cr more purchases + 37Cr more in power & fuel)

- The capacity of cement industry domestically stood at 300 million tonnes per annum

- It seems to me that some accounting method has changed in this FY. The numbers vary across two annual reports in Raw Material, Loans & Advances etc. Raw material example shown below. (Ask CA??)

FY11 RM →

FY12 RM →

AR FY13

- Joint venture with Polyex Minerals Private Limited on 50-50 basis. The goal is to establish a Silca Sand Refining project with capacity of 2L MT. This will help in backward integration & procurement of quality sand on continuous basis.

- Another instance of mismatching numbers between AR FY13 & AR FY12. In FY12 AR, exchange loss in consolidated financial statement is 8 Cr. The exchange loss for FY12 as per AR FY13 is 55 Cr.

- Award of Damages in Patent matter by District Court of 3924.02 - Nashville, Tennessee U.S.A. (US$ 7228544.64, INR - 39Cr), which is disputed by the Company.

AR FY14

- Operating margins significantly expanded in FY14 on the back of reduced RM cost (39% to 35%) & reduction in other expenses (40% to 33%)

- The patent matter dispute in USA of 39Cr seems to have resolved without any payment. Perhaps, this is one of the reasons legal fees had spiked to 19 Cr in FY13.

AR FY15

- Margin expanded again due to inventory expense going from +70Cr to -100Cr.

AR FY16

- Margin expanded again on the back of reduced RM cost from 39% to 32%

The pro-investment points in AIA engineering are -

- Very sharp managing director

- A very large opportunity size in converting mill parts from forged to high chrome

- Repetitive nature of business

- Capacity expansion to 4.4L TPA with utilization around ~2L TPA

- Clean balance sheet with negligible debt through expansion.

The risks in investment thesis are as follows -

- The stock is well discovered (32% holdings by FII + MF) & richly valued.

- The growth in export business has slowed down which was major growth driver

Disc - No investments at this point