Can anyone share AGM notes, if someone has attended the AGM.

ATFL AGM Notes:

- Company has been keeping costs under tight control, since it is a challenging time for everyone. Q2 should be normal comparatively.

- There has been a significant uplift in the food segment.(Ready to cook)

- As we started to scale up, had to make some choices and focussed on Ready to cook segment- ActII and Peanut Butter segment due to these 2 being much more profitable and supporting good volumes.

- At present we have set a rule of not to employ peak employment in any unit more than 40%, hence had to make a choice of focussing on ready to cook rather than ready to eat segments.

- Spreads segment was performing low, but is changing month on month. Since people were not going to gyms or lack of exercise has pushed them to be more health conscious, hence there could be some downside due to this but now demand has started coming back.

- Chocolate Spreads is on a track to takeover large market share of a prominent brand due to quality & pricing.

- There has been an increase in demand of peanut butter in UK markets, Kellogs & Unilever has now entered this segment. Expect more competition in the next 2-4 months.

- Cereal & confectionary: Expectation was of 500+Bps from new products and that’s happening. Intend to expand breakfast cereals, will grow much more in future. Will cross the 20% mark in margins soon. Will take 1-2 quarters before scaling this big time.

- Cocoa margins are down in mid teens. There has been a fall in chocolate demand all over the world, so they are being cautious here. Why did we focus on coconut as a filling in our chocolates? Well, we could have gone for any tyoe of filling or moulded chocolates, but Cadbury is a brand which so well placed in the market that it is very tough to get into. Hence we launched coconut filled chocolates which has low competiton (Bounty) as compared to cadbury’s.

- Edible Oil - Sundrop - fall in April due to low levels of Inventory, but have done good in May because of some fatigue after so much cooking done in past few months. Did saw good elevated demand in March but it tapered off in June. There was an increase in commodity prices of oil in march. We expect significant improvement in volumes in next quarters.

- Our Food business has now crossed our Edible Oil business. With this the risk in the oil business is expected to come down. This change took a long time and a lot of effort. Expect to decrease the V.oil prices in the next few quarters. It should be set between Rs 140-150. See food business continue to grow from here.

- Sundrop Heart and Active life are the margin drivers. We look at some moderate level of growth in these two brands. And we are in good shape here.

- Fall in expenses was due to decrease in expenses like travel, electricity, low maintenance costs. Is this sustainable in future? It can be if we focus on margin expansions and control our costs.

- During March-June we have been able to improve our distribution networks immensely. Why don’t we outsource in Food categories? We dont believe in outsourcing since it does impact our costing and retail network. Also it is a matter of months since 2 new plants are ready to start post installation(taking time due to COVID). We expect July & August to see growth.

- Food business is a 35000 cr business. Distributors in smaller cities won’t be interested in our company if we don’t give them their profits. Hrnce we have changed aur distributor process. Rs. 5-10 Ready-to-Eat products are now directly going to distributors unlike through warehouses. It saves costs and gives us a margin to give them their share of profits. Hence these products are doing well in small cities also.

- Ready-to-cook segment grew double from 18%-37%. Without COVID this kind of growth would have come in Q4.

- Expect launches of new products in the food segment in the current FY.

@desaidhwanil please correct me if I have missed any point or have put any point wrongly.

14 Likes

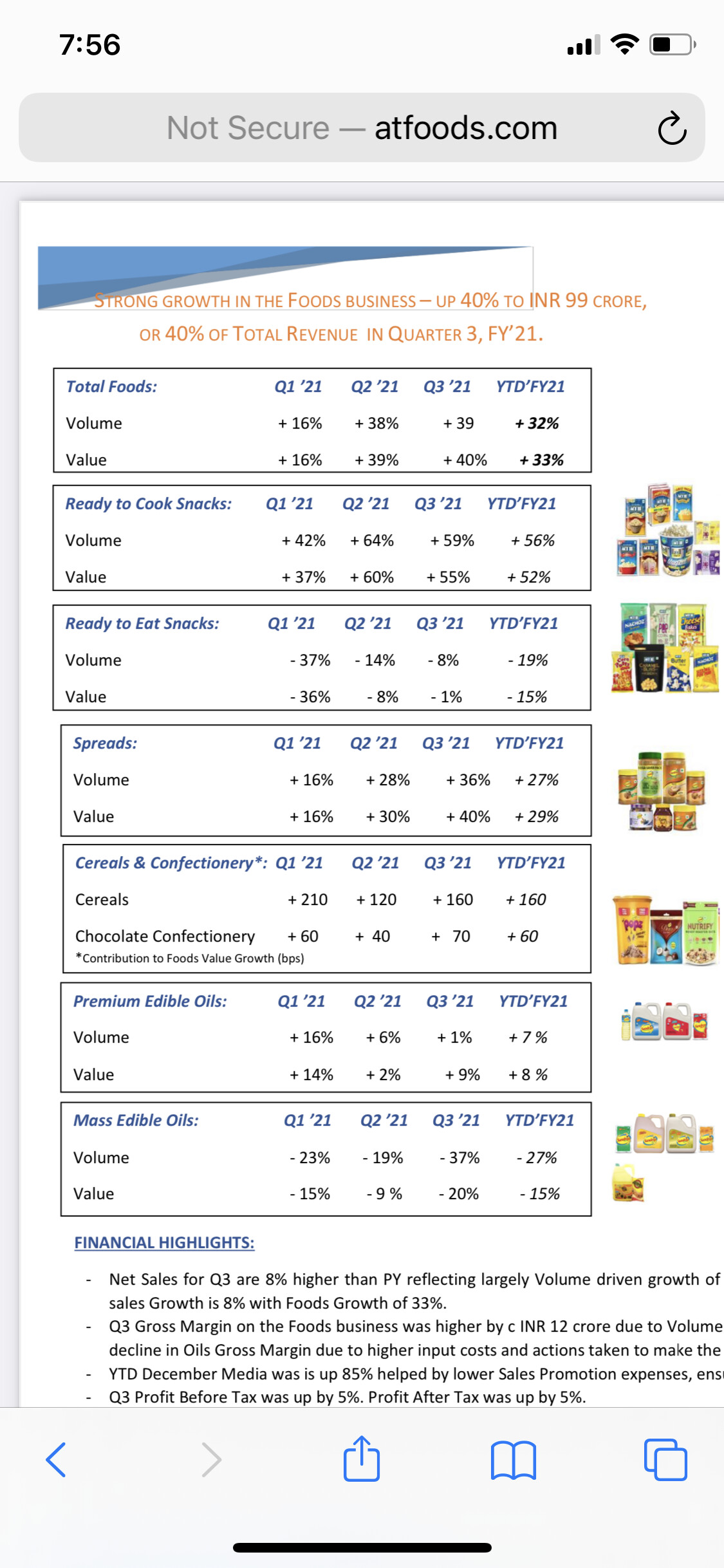

Stellar performance of the food in RTC and spread business continues. Food now contributed 42% of the total revenue in the current quarter and if it wasn’t for the subdued RTE ( conscious decision) segment, the contribution have been even more. Management is walking the talk and moving in the direction where food business have dominant share of the overall business.

Disc - invested and is part of the core portfolio

1 Like

Indeed, revenue yoy growth also looks promising. Any inputs on why the expenses have shot up significantly this Q and also Inventory costs? I also see significant chunk of expenses under head of “other expenses”…any idea what lies in this bucket?

Thanks

‘Other expense’ were mainly on account some receivables write off which they anticipate they will not be able to recover and special sanitation arrangements in manufacturing both as an impact of covid.

On con call they informed that HUL have entered the peanut butter space with their Kisaan brand but mgmt feels confident about the value Sundrop offers to the consumers.

RTC will remain the focus for the co and all media spend for now is being spent on this category alone. The increase in adv and media spend was offset by the saving in travel and overhead expenses as a result of work from home, without jeopardizing the P&L. This was clarified on the question raised by @desaidhwanil.

While they are confident all foods category doing well, the opportunity size is biggest for the chocolate confectionery with their center filled coconut and peanut offering. This festive season they will be experimenting with some gift packs but on a very small scale. Idea here is the explore packaging and also sample peanut butter in small sachets ( my reading ).

They gave a hint of working on developing pasta and noodles as new product in the RTC category but it’s a work in progress and nothing in near future.

Overall the commentary was on the same line as to how they want to decouple themselves from the commodity business of edible oils and become a food company and create long terms sustainable growth with healthy FMCG margins.

They also acknowledged that the superior growth in the RTC category has some share on account of lockdown and therefore people consuming more at home but as such couldn’t quantify how much of the growth is structural and how much is temp. One positive thing to note however is, Aug was better than July and September sales were better than Aug when there was hardly any lockdown. So some of it could be a structural shift in acceptance of the brand. Will get to know more in coming quarters.

Overall a promising story and the only joker in pack is the edible oil business which we need to watch carefully.

Disc: invested and added more after the result and conf call.

8 Likes

thanks for succinctly summarizing the key takeaways from the call. One minor correction- the ad spend is focused on RTC and peanut butter both and not only on RTC.

I certainly feel the texture of the business is changing and had ATFL not been in the midst of a edible oil pricing upcycle…numbers would have surprised the most optimistic assumptions.

One very interesting thing to note from the numbers Mr. Sachin Gopal mentioned on call, Edible oil gross margin this qtr was around 10%. I think in terms of edible oil margin erosion, the worst seems to be behind them as many players would either walkaway from business below a certain margins or they will take price-action to maintain/improve margins.

2 Likes

Hi Dhwanil, in the recently disclosed ‘related party transaction’ I noticed the Royalty paid to parent ConAgra, has increased substantially by more than 100% yoy for half year ending Sep 2019 vs Sep 2020. Sales for the same period have hardly shown a 10% growth. Any idea why such big divergence? I recall there was a change in Royalty commission earlier this year but not sure if it was in tune to that effect. Appreciate your input if you have any clarity on this.

Regards,

Ram

Royalty is mainly on the Act-II brand of popcorns; and this year RTC segment has seen high growth even though overall sales is lower due to RTE segment.

1 Like

any one attended the Invester meet ? Any link for video recording ? Presentation is uploaded on the site as well as BSE however curious to hear management commentary. Overall great outlook and path forward.

1 Like

Stellar performance from the foods business continues and provides some assurance that the increasing trend in RTC consumption was not a windfall gain form lockdown and part of the growth is sustainable.

Disc- invested and continue to add.

5 Likes

Who is the top customer contributing 14% of revenue for the company?

I have seen that they are unable to maintain supply of items other than popcorn and oil in stores. I used to love the peanuts , but finding them is a hit or miss… Similar with the ragi choco fills.

1 Like

Edible oil continue to drag the overall performance, otherwise the growth momentum continues for the foods business.

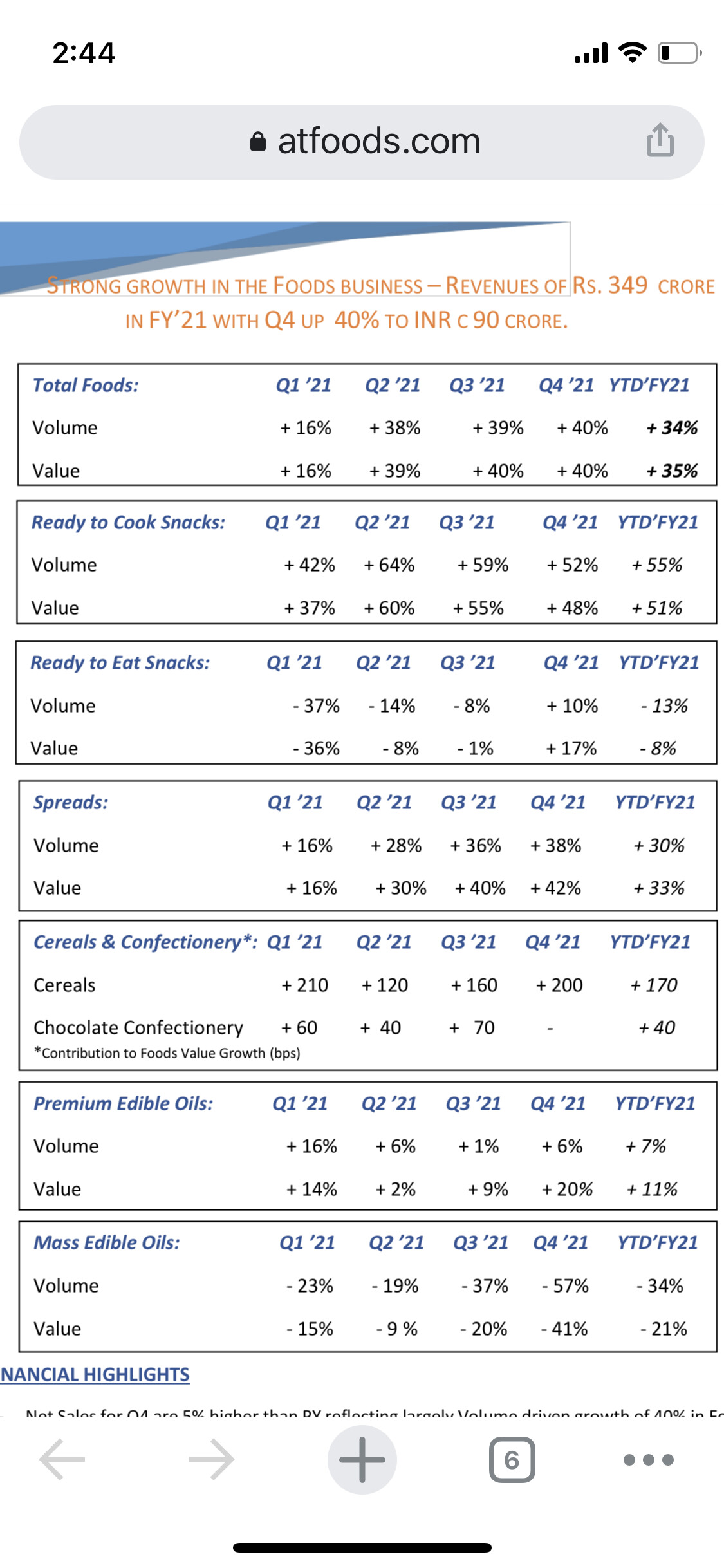

With 35 % YOY growth and revenue of 349 Cr, foods now contribute 39% of the overall revenue compared to 31% at the end of last FY.

At this rate, it should cross the 50% mark in next two years if not earlier, given the pipeline of new launches in RTC segment.

Within the edible oil, the premium category has shown decent vol growth but that came at an expense of margin contraction. Clearly showing no pricing power in the commodity type business.

Look forward for the conf call tomorrow.

Disc- continue to remain invested and part of core long term portfolio.

3 Likes

• Headline numbers from Agro tech are weak. Sales growth of 5% YoY in 4Q on a weak base decelerated versus 12% / 8% YoY growth in Sep and Dec quarters. Two year CAGR at 3% was also a bit weak versus what we have seen for other leading FMCG companies (Nestle 10%, HUL 4%, Britannia 6%).

• Margins performance was also weak this quarter. Gross margins at 28% in 4Q are actually the lowest in a few years and were down 200bps QoQ and YoY. This lead to EBITDA margins of 4% for the quarter which are again at multi-year lows. EBITDA declined 16% YoY and 2 yr CAGR decline was 22%. PAT declines 55% YoY due to one off tax increases.

• The only consolation is that all the pain this quarter has emanated from the oils portfolio. Edible Oils sales declines 12% YoY (2 yr CAGR of negative 6%). The two year CAGR is the worst in several quarters. The likely reason for this is threefold 1) price rationalization at the premium end to defend market shares 2) strategic defocus on mass edible oils 3) increase in RM costs in oils which could not be passed on due to the commoditized nature of the business and high competitive intensity.

• The foods business continued its strong momentum – 41% YoY with a 2 year CAGR of 19%. The strong pick-up from 3Q has sustained into 4Q which is heartening. Contribution margins in foods also improved as the business continues to gain scale. FY21 foods sales grew 35% almost completely volume led. Company continues to make aggressive ad spends in the foods portfolio despite the drag in edible oils.

• While the foods business momentum is encouraging, the drag from the oils portfolio is certainly higher than expected which will drag overall numbers for the company.

Call is at 2pm today but not able to find the call details; pls share if anyone has them, thanks.

4 Likes

Expect subdued nos from the current quarter as the spot market prices for the edible oils have sky rocketed in the recent past. Channel check suggest that consumer price for edible oil have doubled in 2021 than the avg price for it in 2020. This i suppose is mainly because of the higher input cost.

Hope the stellar run in foods and spread business will continue although it still have not reached a scale that will nullify the drag from oil business.

Disc - continue to remain invested.

3 Likes

Agro Tech Foods purchased land in Kothur (Telangana), which is adjacent to its existing plant and amounts to approximately 25 percent of the current land area of the existing plant. The land will be utilised for continued expansions of the company’s manufacturing operations.

1 Like

@ramdhawad and others…this Q again I see topline at approx same level since many quarters…and bottomline seems fluctuating and unpredictable since last few Qs…I understand maybe product mix is improving, but it should show in margins and better profits in same revenue? Pls correct me if wrong and also would be great if you could share your thoughts and details on this Q results and also overall last year’s trajectory, if possible…this is indeed one of difficult FMCG firm to predict numbers/understand so far…at least for me…thanks!

3 Likes

Came across this Duo chocolate commercial. Walking the talk of increasing an advertising expenditure on RTE and Chocolates.

Disappointed Q3 results, indicating either the demand uptick in previous quarter was one-off because of lockdown stocking up or the price hike has led to pressure on volume growth. Either way not a good sign.

Look forward for the quarterly call.