AGREE.

If they get their act right, which I hope they will, it can be a superstar.

AGREE.

If they get their act right, which I hope they will, it can be a superstar.

did you see market share numbers for sundrop? how is it doing well?

Hi v4value,

Yes the mkt share has slipped wrt Saffola and to some extent Fortune. However its volumes are growing and the catageory ( premium cooking oils ) itself is showing good growth. ( bcoz of people upgrading to better oils ).

It is just that it is growing slower than saffola and hence the aberration in mkt share.

Hi @ranvir I also feel that branded cooking oil in all categories even bottom pyramid is replacing unbranded oil.

Even Pincon oil brand has shown very high growth, which surprised me.

Do you have some data source on this?

Here is one link- showing the growth in branded oils and fall in loose oil sales.

Agro Tech management is focusing on food business. They have clearly said that they are happy if Sundrop, Crystal oil sales remain as it is – it is used to pay the bills of the company but focus is on the snacks business. So we should not invest in this company if your thesis is growth in branded oils. For the latter Marico is obvious choice.

disc - invested in AgroTech

Bhaskar my worry is if Agrotech loses share in Sundrop, teh only bargaining chip they have at distribution, how will they compete with an ITC suite of products? They will be neither here (oil) nor there (food)

We should remember that as a company AgroTech was a pioneer and started the retail popcorns business with its Act2 brand. We don’t have any other big competitor in this business. Then they started Sundrop Peanut butter, tortilla chips and other bag snack products. Though there are few big competitors in these businesses including Doritos,ITC, regional players like Tasty Bites etc.

They can also bring-in other products from its parent ConAgra in the future. As a strategy I would also want them to concentrate equally on both the oil and foods business but they are very clear that their focus is on ramping the food business.

We should not expect any short or medium term gains with this stock. This stock/company will test our patience. My thesis behind investing is captured in my blog - https://indianvalueinvestorblog.wordpress.com/2016/01/24/agro-tech-foods/

disc - invested in AgroTech

Absolutely agree with Bhasksar.

Lets see how it goes. Patience shall be the key here.

Short Summary of Q3 conference call:

we have also prepared few other summaries. Sharing here: https://goo.gl/5RTk0o

To get mail alert for daily updated summaries, pls fill in mail id in form here: https://goo.gl/forms/rKVCPDBBdCSsUZHB3

Read disclaimer for summaries here: https://goo.gl/HELov8

Cycle seem to be turning in favour of the company

Agrotech foods was a Stalwart Advisors pick. They have now given exit recommendation because of lack of price movement was inflicting a loss of opportunity cost.

But technically, the stock is now under volatility compression on long term charts. A huge breakout seems to be inevitable in the next 2-4 months…

I am given to understand that this has been a Prof Sanjay Bakshi pick too…but not sure.

Anyhow, i have purchased a good qty of Agrotech foods…i find the downside risk to be quite limited to 450…and upside potential to be quite good. Fundamentally, the stock continues to remain a good pick.

Risks:

Disc: Invested recently (minor allocation). Have been patiently nibbling around 500-520 level.

I share the views. The stock is cheap with low downside but capped upside till it actually is able to deliver on numbers. It has fatigued investors patience to a dropping point. The competition is hotting up with domestic and other foreign brands already establishing market presence. The management commentary during con call has always been positive but the realization in numbers is key to watch out for. My guess still a long way to become a visible FMCG player. Odds still in favour of the company for the price is still a bargain at CMP.

Source: http://www.bseindia.com/xml-data/corpfiling/AttachLive/7dfa5598-a304-404e-99bc-e32d9b9036a0.pdf

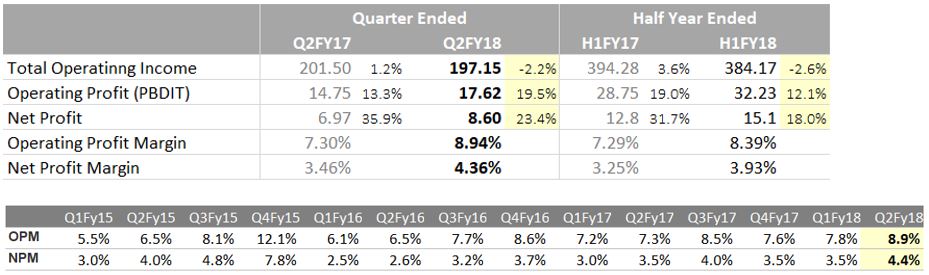

Isn’t flat sales a bit concerning? after all the capex it is doing for so many years, top line is not moving, not just this Q but for last several years. Why all this capex not generating sales?

Growth in Operating Profit also due to cut in advertising which means future sales are likely to be flat as well.

Couple of reasons (Source: Management commentary) -

I think ATFL should be judged on how they perform in foods business. Peanut butter revenue up 70% and Act II Ready-to-Eat revenue up 46% YoY in Q2Fy18. Foods business reported growth of 20% this quarter. Foods share of the business rise up to 27% this quarter. More Indian snacks coming under Sundrop brand in next 6 to 12 months. ATFL has increased distributors by 20% in last six months. If they are able to do the same in next 6 months means 35-40% increase in a year. That is a biggie. Basically, as product portfolio increases, distributor traction increases. More distributor, means more city/town coverage. Ultimately wider coverage will result in sales growth in days to come.

Advertising and Promotion expense is lower by 3 cr this qtr YoY. 10.8cr v/s 13.8 cr. This reflect two things -

Only thing they can vouch for so far is their RTE popcorn a far cry from what it could have done in past 6 to 7 years. Stock languishing as the management is bz with Conagra losing marketshare in US. It did create good infrastructure but ITC after selling this business has moved up the ladder chain much faster than Agro tech. It has potential will it create the magic only time will tell.

Hi, Is there any concrete news for move for more of 40% in recent months?

Or it is just discovery of the stock having a huge potential in packaged food segment. Next frontier of FMGC

Still below <2000 cr market cap and subsidiary of one of largest American food companies.