Investor Zoom call tomorrow, after a long time:

Source: https://www.bseindia.com/xml-data/corpfiling/AttachHis/43f9d425-9fc7-4d11-83a7-701a72145e8a.pdf

… the Company will be hosting investor and analyst conference call (group meet) on Tuesday, December 03, 2024 at 12:00 p.m. to 01:00 p.m. (IST) to discuss the Company’s Future plans and performance for the half year.

The call will be initiated with a brief management discussion on the Company, its product Categories, future plans and financial result for half year and future plans followed by an interactive question and answer session.

On behalf of the Company, the call will be addressed by Mr. Milind Padole, Managing Director and Mr. Rahul Padole, Director of the Company.

This meeting will be conducted online through Zoom Meeting mentioned as follows:

Launch Meeting - Zoom

Meeting ID: 885 6558 2773

Passcode: 367214

All the investors are requested to send their questions in advance to info@arapl.co.in.

Disclosure: I’ve been invested from lower levels.

1 Like

Is the company going to have a call…its been 2 quarters.

Does anyone have any idea whats up with this stock? heavy selling in the past 2 days. Is vijay kedia exiting ?

2 Likes

What would be the tariff rates of Robotic exports from India into USA ?

Will it be exempted as it may have electronics classification?

Will it be 25% , without the additional 25% tariff since it’s a machinery involving aluminium & copper

Or it would attract 50% tarrif rate ?

1 Like

The recent appointment of Mr. Neeraj Gupta as a Strategy & Growth Advisor doesn’t make much sense to me. His background is primarily in the transportation sector, with experience at Meru Cabs and later a travel company. I’m struggling to see how that expertise translates into value for a robotics and automation company.

If anyone has insight into how his experience could be relevant here, I’d appreciate your perspective.

1 Like

The promoter has sold 5 stake in the company, the price is below its right issue. See some short term pain, until they execute the said nos they committed in 2023 rights issue ppt

I asked a question regarding the RAAS guidance in the Arihant conference. The management sticks to their earlier guidance of $30-40M for RAAS in FY26, although their current orderbook is only $4M for RAAS. I am not able to comprehend this

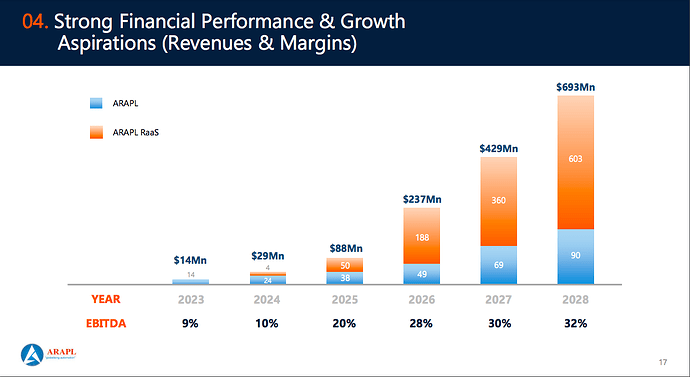

A simple way to assess them is to look at how they’ve performed since their last set of projections. In my opinion, there’s nothing wrong with being optimistic, but projections need to be grounded in reality. Take a look at what they said in Q2-2023.

3 Likes

This company used to trade at 300-400 pe. Almost 75% fall from there. What a wealth destroyer..lesson is alway stay away from companies giving rosy guidance.

4 Likes

The company has posted decent quarterly results - but volume uptick isn’t there - have written to mgmt asking for guidance

AFFORDABLE ROBOTICS AND AUTOMATION LIMITED ( ARAPL ) INVESTOR AND ANALYSTS CONFERENCE CALL - 31/10/2025

2 Likes

Some thoughts after listening to the Q2 concall

Interesting developments here… Beyond the just turned around quarter financials

Firstly… The business in its current state needs lots of funds… And so the promoter sells part holding in the market, (supposedly to a group of HNIs) and funnels those funds to the company as an interest free loan(to be converted to equity at a later stage). How much influence of HNIs would exert on the decision making in times ahead, or is it the level of confidence over the times lying ahead… One will watch.

The promoter and his team extended the call beyond the customary 1 hour session, so they were keen to connect and eager to take questions… Also committed to continue quarterly concalls and not miss, as was their form in the recent past

Humro/mobile robots seem to be the silver lining here, with built in capacity of 400 Nos per year, and a deployment of just 30-40 in US so far(6-7 only for PoC deployment at potential customers sites)… Two large clients have cleared the PoC stage, and likely to drive orders in the next FY. This is the key trigger to monitor, for this to emerge as a turnaround story (just one qtr is not evidence enough).

New to the company, so trying to develop my understanding here. The inputs of earlier contributors do give a heads up but wondering if…at close to all time low, is there value here or just a promise for growth and fund burn?

Thoughts of other contributors, on whether there is something changing here, would be really appreciated.

Disclosure… Tracking position.

2 Likes

Declining Sales, Rising Debt and heightened receivables are matter of concern for me.

1 Like