IFRS 16 / Ind AS 116 – Leases (Right-of-Use Asset)

Para 24 – At the commencement date, the lessee shall measure the right-of-use asset at cost, comprising:

(a) the amount of the lease liability;

(b) lease payments made at or before the commencement date;

(c) initial direct costs; and

(d) estimated dismantling / restoration costs.

Other unrelated pre-operating expenditures cannot be added to the ROU asset.

Any idea what’s comprises of this defered expenses.. most of the expenses are allowed but training cost of pilot or salary / admin cost needs to be expense off

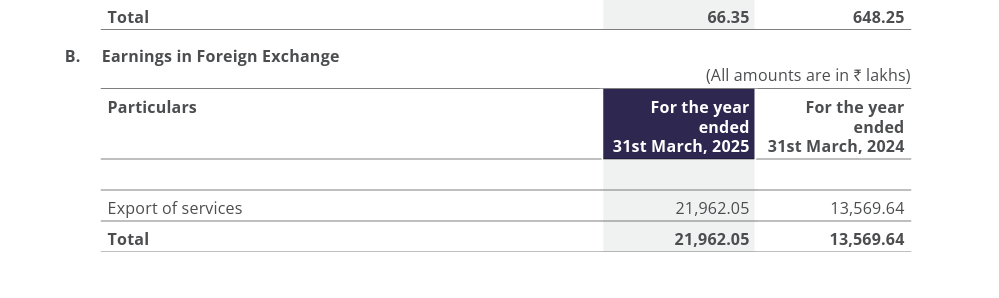

InterGlobe had a ₹1,000 crore loss due to forex impact from the rupee’s depreciation. Since most aircraft leases in aviation are dollar-denominated, this risk is hard to avoid.

Will Afcom face similar issues? I’m not fully clear on this and would appreciate some insights

Afcom’s case is different. InterGlobe earns majority of the revenue in rupee terms but its expenses (lease + fuel) are in dollar terms hence it will affect more if rupee depreciates. But in case of afcom, it earns in dollar (export services) and hence it should benefit if dollar is appreciating or rupee depreciating.

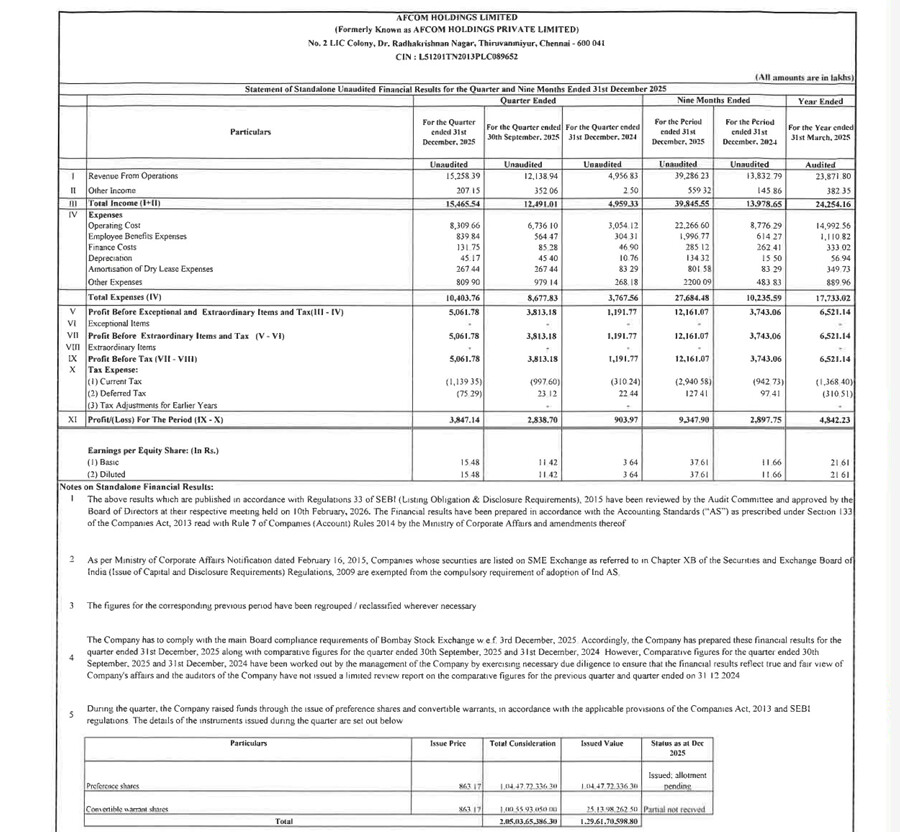

Q3 results looks better than expected to me. I assumed Q3 to be very similar to Q2. But looks like something is getting better. It could be utilization/pricing or just currency effect. Will wait for the IP for more insights.

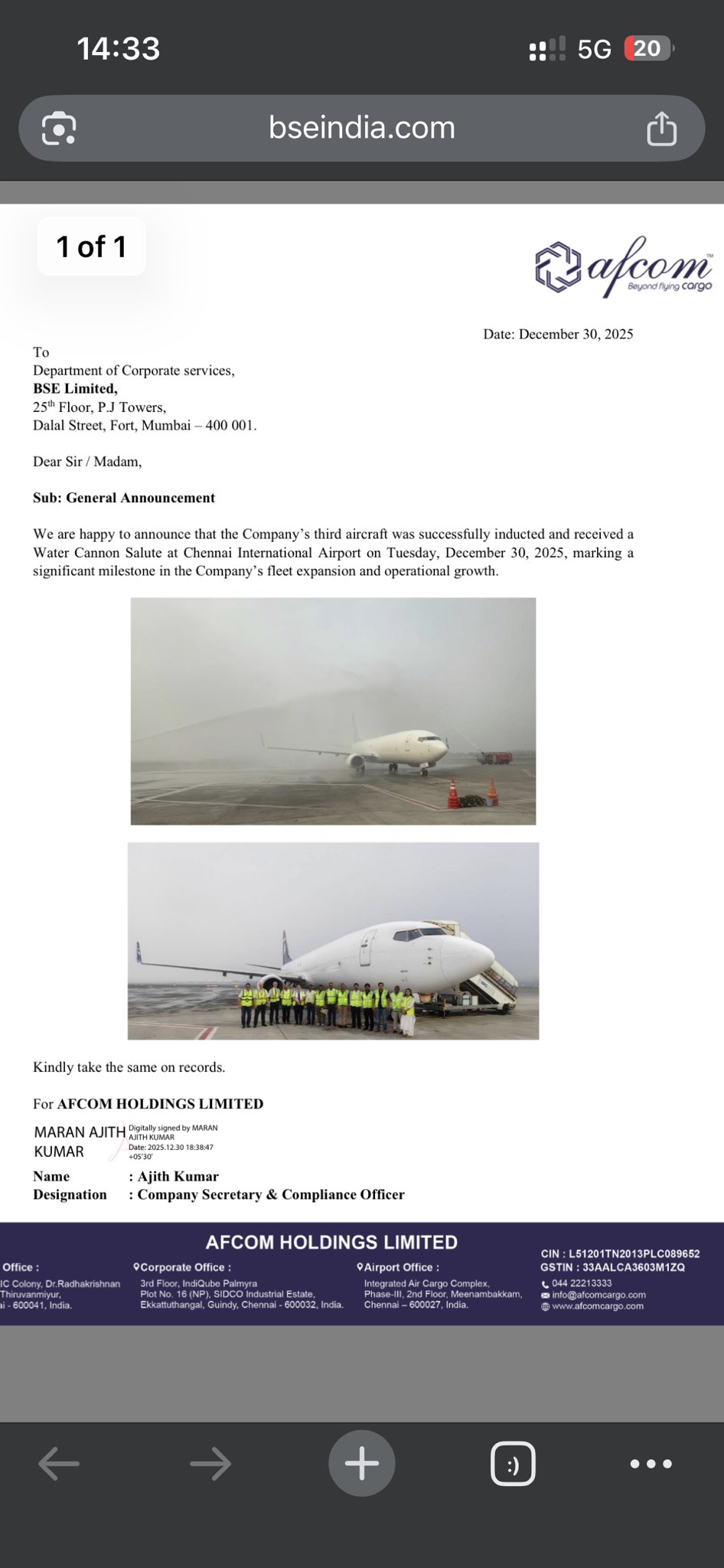

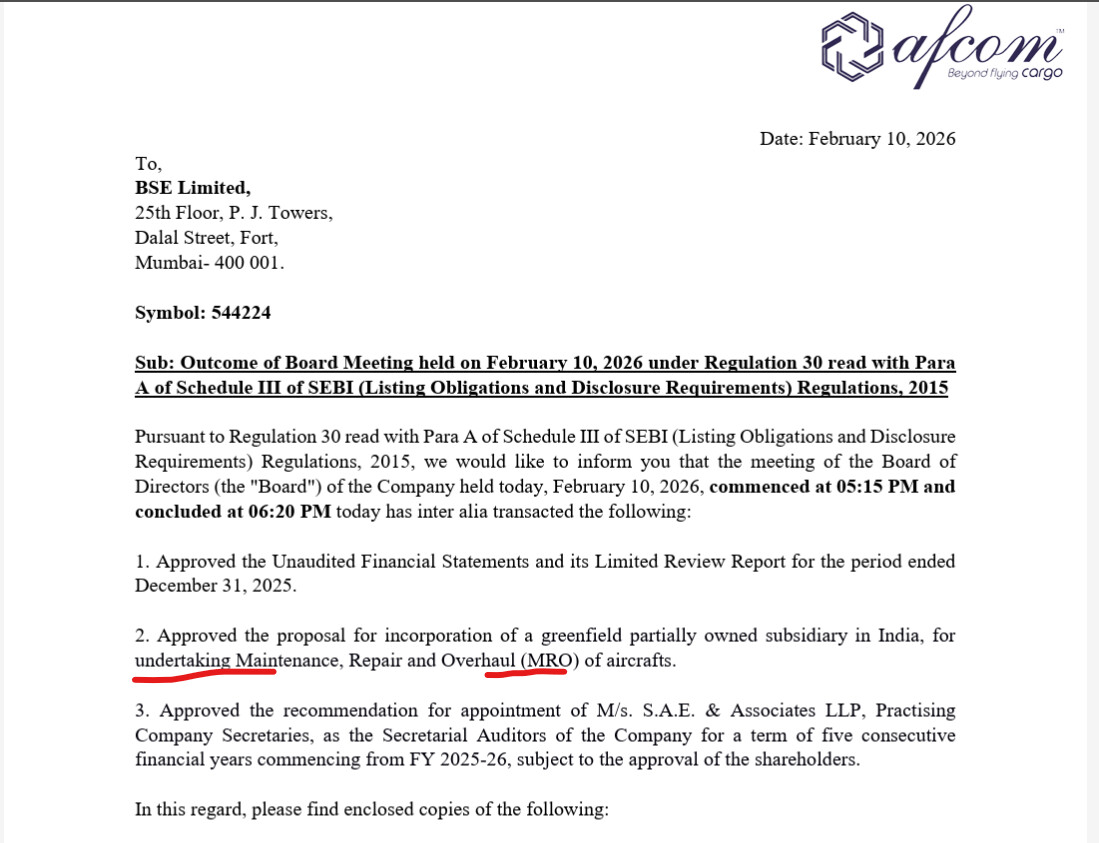

MRO is a positive news. Let’s see how markets takes it.

MRO is a surprise move. If they decide to onboard 3rd party customers that’ll be additional revenue, on top of the savings made on maintenance of their own planes.

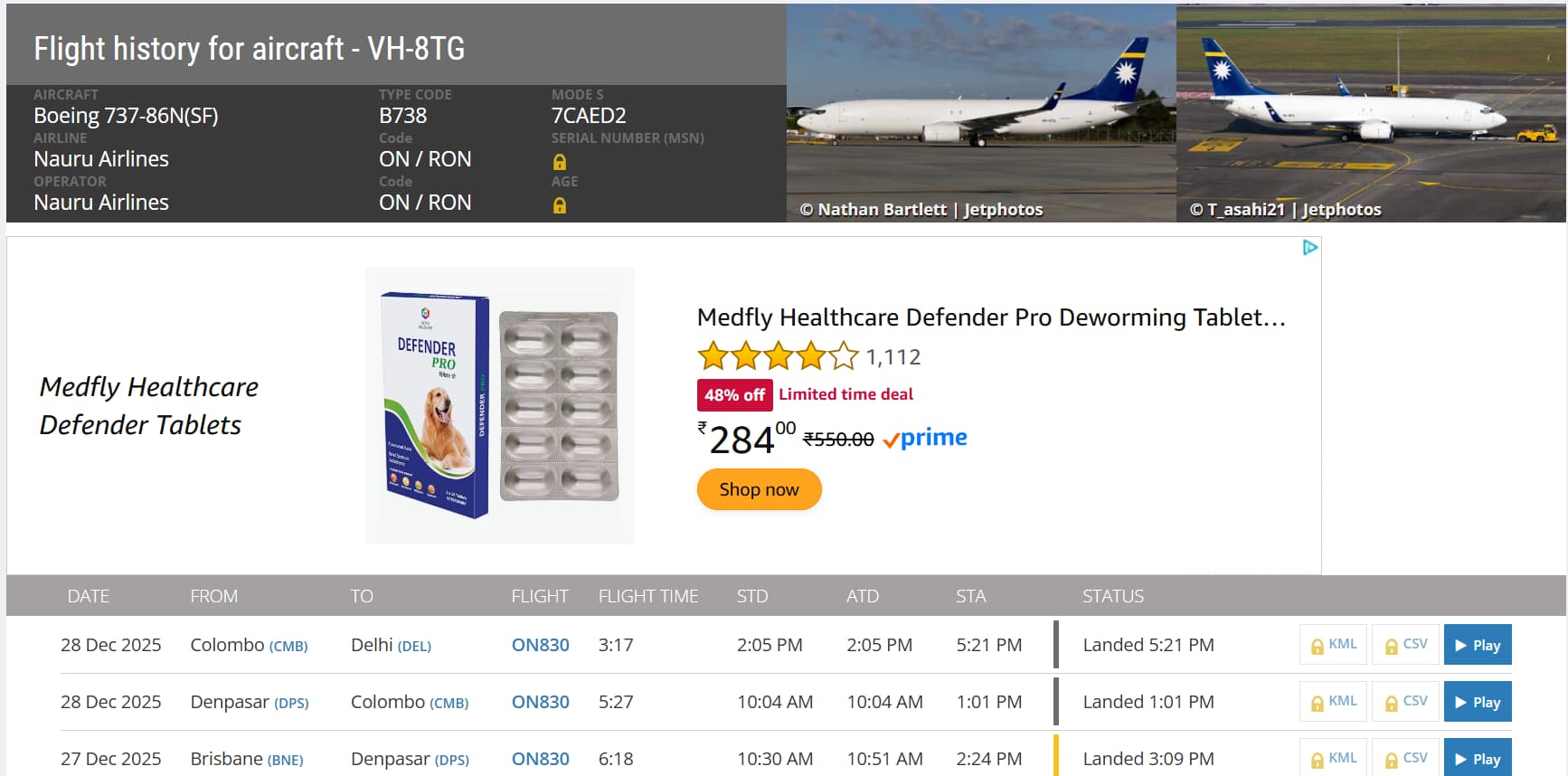

Just with 2 planes,.their revenue and profit is blasting.. I don’t think the 3rd plane is still in operation. It was came last month yet it’s not functional. Any idea about what’s going on 3rd and 4th plane?

Correct. Third plane isn’t in operation yet. One reason could be, there is still lot of procedural aspect to be taken care of after the plane is procured . Another could be, one of the planes is used as a kind of backup.

Worldwide there is a demand supply gap of planes and it’s getting tough to procure them. This is my understanding, but no updates from the company in this regard

currency effect won’t be more than ~2.3% (based on Q2 and Q3 average USD to INR data). Their Q3 grew by 20%+ QoQ. So must be better utilization/pricing/costs.

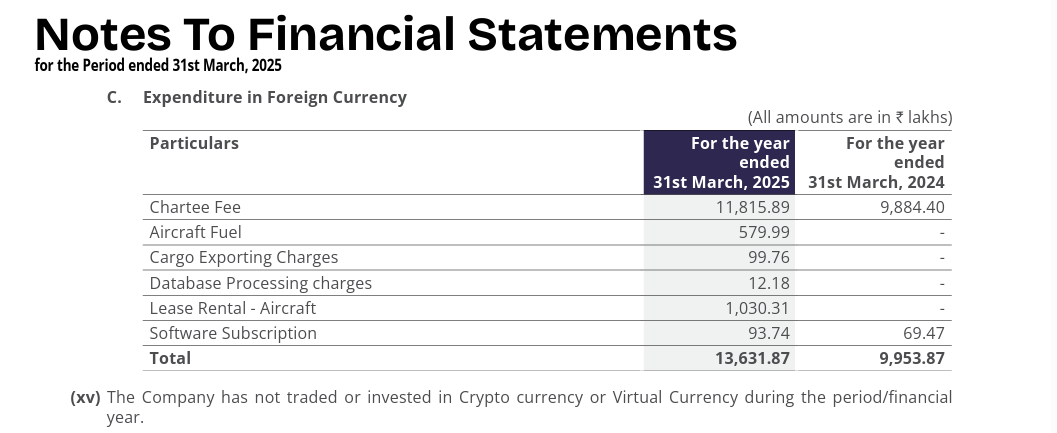

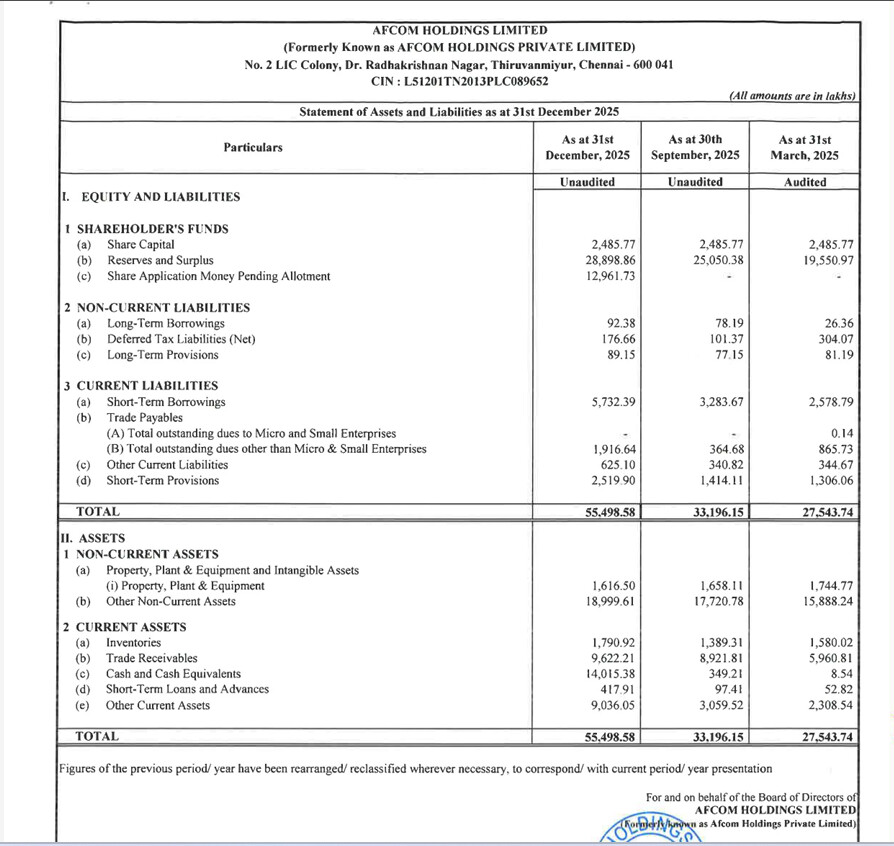

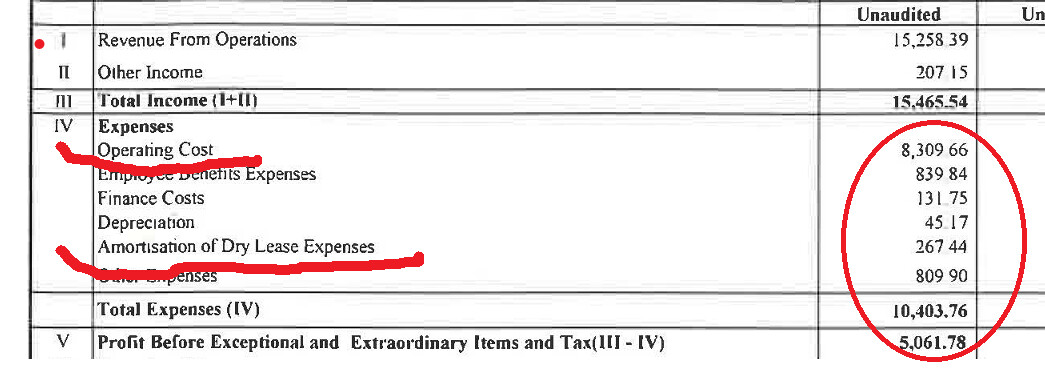

Anybody knows how much are the future committed lease rentals the company is liable for? The Amortization of Dry Lease Expenses (Rs.2.67 crore) appearing in the P & L pertains to the pre-operative period. Lease rentals for the two aircraft are being clubbed with other operating expenses such as fuel etc. and shown in a single line item as Operating Cost. This will now go up in Q4 with the third aircraft joining the fray. So I am not sure how to analyze this. I am surprised even the credit rating report does not mention or consider this (i.e. the future committed lease rentals).

Typically, they Amortize Dry Lease Expenses plus the associated costs of getting the freighter in air. So those will go up in Q4 only with corresponding topline growth. So not sure, if i understood the concern on analysis here.