Ques: What does the company do?

Ans: Cashew Processing & Trading Business

Ques: What is cashew processing?

Ans: Aelea imports Raw Cashew Nuts (RCN) from various African nations.

including Benin, Tanzania, Burkina Faso, Senegal, and Cote d’Ivoire,

requiring substantial working capital funds. It specializes in trading RCN

and Cashew Kernels and also trades in by-products from sugar mills, such

as bagasse.

Ques: When was this company established?

Ans: Aelea Commodities Limited (Aelea, the company) was established in 2018.

Ques: What is the category of business? Is the business having a high entry barrier?

Ans: A business with many firms and low barriers to entry is typically called monopolistic competition.

Ques: What is the market share of the company? There should be some reason to study this company.

Ans: The market share is around 3%

Ques? Then what is the reason to study the company?

Ans They have done massive expansion. More on this later

Ques: Is it B2B or B2C?

Ans: Both B2B (90%) and B2C (10%)

Ques: Who all are clients of the company?

Ans:

Ques: What are the product categories in B2C?

Ans:

Ques: Could you please walk us through the process of the cashew nut that comes to our home?

Ans

Ques: What is the revenue breakup on cashew processing and trading, and what is the future goal?

Ans: It is 55% Cashew and 45% Trading agro, In the future, the aim is to make 70%. Cashew and 30% Trading.

Aelea Commodities Limited is at the forefront of India’s agri-value chain transformation, specialising in cashew processing, international agri-trade, and allied commodities

Adding pictorial representation

• Cashew Processing: This is the company’s core business, supported by a fully integrated processing facility in Surat, currently operating at a capacity of 140 metric tons per day. It has robust backward integration through direct sourcing of raw cashew nuts (RCN) from Africa, and strong forward integration into value-added products. The company serves a diverse client base that includes premium snack brands like Haldiram, leading ice cream brands like Amul, and well-known names such as Bikanervala, Star Bazaar, Jabsons, Farmley, and Reliance18.

• Trading Business: The company emphasizes that trading is not its primary focus. Instead, trading activities are carried out strategically to remain informed and engaged with products that may be relevant for future food processing initiatives—serving as a “future pipeline.” The revenue contribution from trading is expected to decline significantly, potentially falling to just 10%–15%.

Ques: Why are we studying this company?

Ans: This is a cyclical company where the margin fluctuates based on the raw cashew price in the market. As there is a lot of competition in the market, if the raw cashew nut price increases, they cannot increase the processed cashew nut price proportionally. The best time to study a company is when the margin is at the bottom end, and also this company has done the capex from 40 MTPA to 140 MTPA—a huge capex.

Margin at the bottom and huge capex and good valuation are often a time to study a company.

Ques: Why was the margin down for a company?

Ans: Regarding margins, the company typically targets 12% to 13% margins on its processing capacity at a standardized rate, which was observed in FY '24. However, H2 FY '25 experienced significant margin pressure. This was attributed to

• Inventory build-up for the revised capacity: The company began building inventory for the new capacity, which is more than 3x the old capacity, and the cost of raw materials was higher compared to the previous year.

• Delays in expansion completion: The expansion, initially targeted for December '24, was completed in two phases (first week of February and end of May '25). This delay meant that the expected profits for the last four months of FY '25 did not materialise.

• Reliance on intermediate products: Due to the gap between the two expansion phases and the initial part of processing (cooking and shelling) not being completed, the company had to buy intermediate ‘shell kernels’ from external processors. This significantly squeezed margins because these small-scale processors have higher costs, and Aelea’s scale meant it was difficult to fully utilize its partial facility with such sourcing.

Ques: So why are we expecting margins to go up in the future?

Ans: Capex (Phase 2 is completed, and there will be full utilization of the capacity; hence, we expecting margin will go up from here)

Ques: All hunky-dorey or any negatives that we should watch?

Ans: We should take note of their working capital. The company in its introduction itself mentioned this.

Any significant price fluctuation in raw cashew and forex could dent the company

Ques: Numbers, please?

CFO TO EBITDA ( Cash and carry model)

109 %

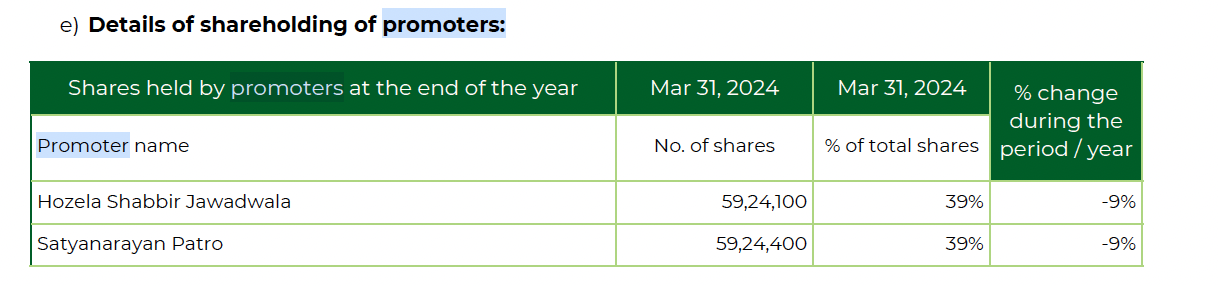

Promoter holding

63.7 %

Pledged percentage

0.00 %

- Secured loan₹ 39.7 Cr.

- Unsecured loan₹ 1.03 Cr.

Ques: Could you please go through the annual report and let us know about remuneration and cash flow?

Ans:

1) CashFlow:

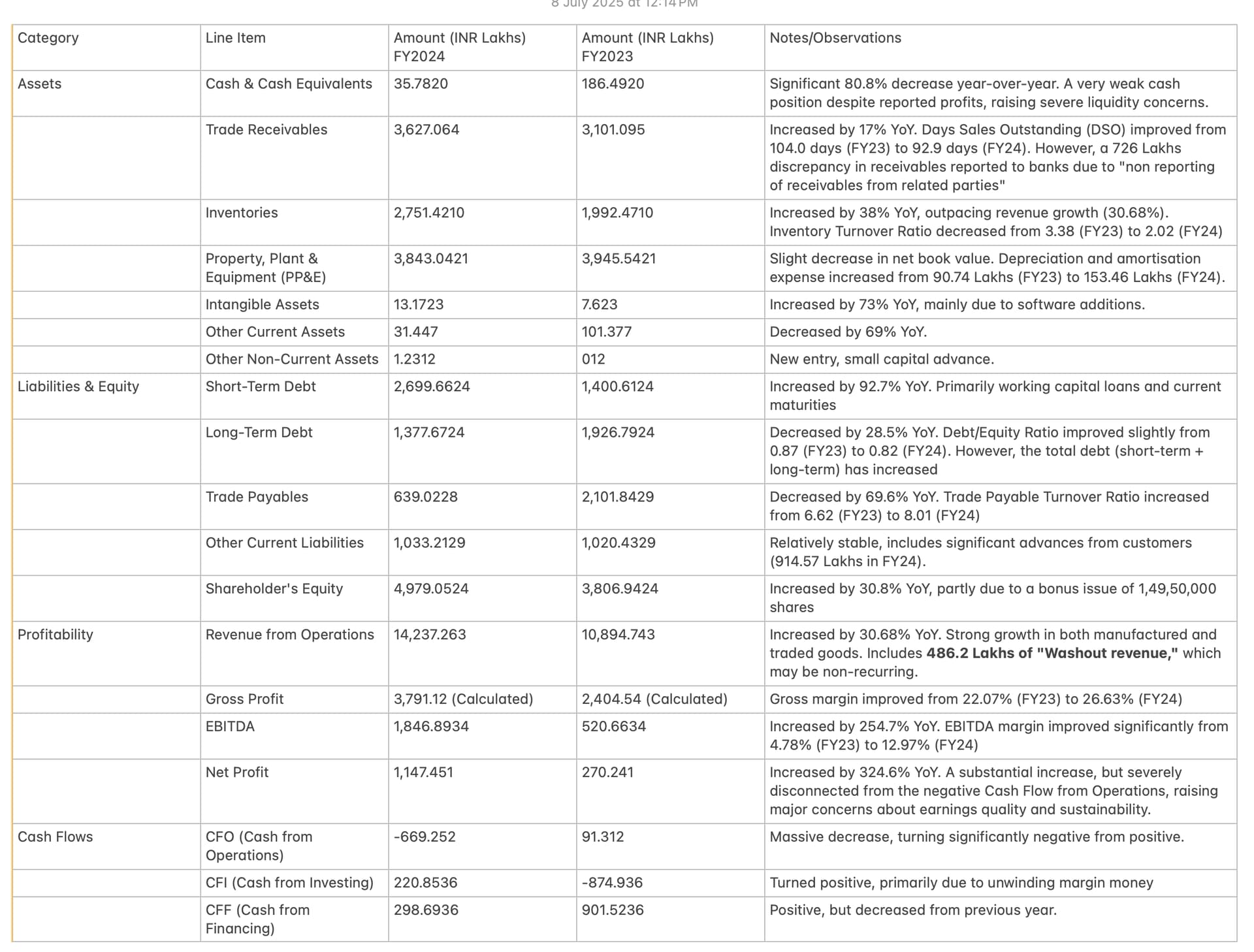

In FY2024, the company reported a net profit of 11.47 cr, but cash flow from operations (CFO) for the same period was (-)6.69 cr.

Net Profit from 2021-2025 is 37cr

![]()

But CFO is not something in accourdance with profit

![]()

This we should track it

-

The TATA ratio (Total Accruals / Total Assets) jumped significantly from 0.0173 in FY2023 to 0.165 in FY2024 - which shows large part of earning is not converted to cash

-

Ratios from Screener

Reason of increase in inventory days is because of the capex the inventory days are increased and in future we can see it going down

-

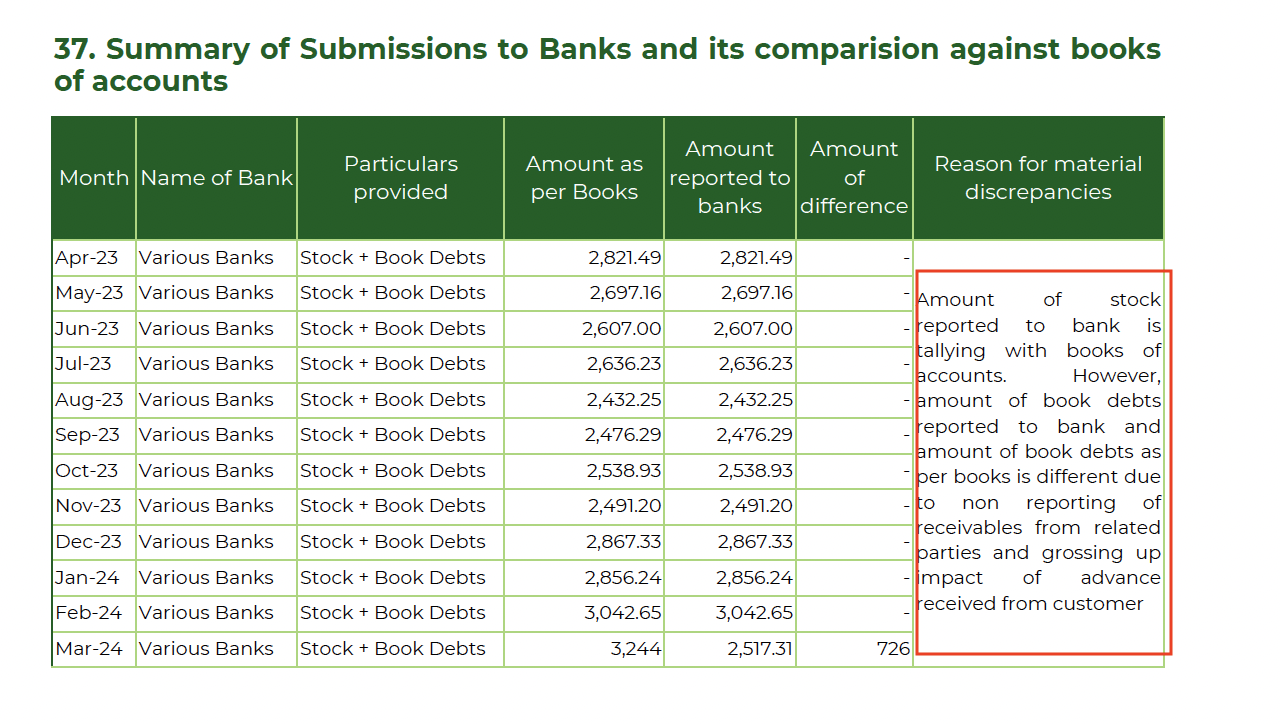

If we look in annual report and debt reported on books, we should keep a watch on receivables

There is difference of 7.2 crore big enough for the type of balance sheet we are looking -

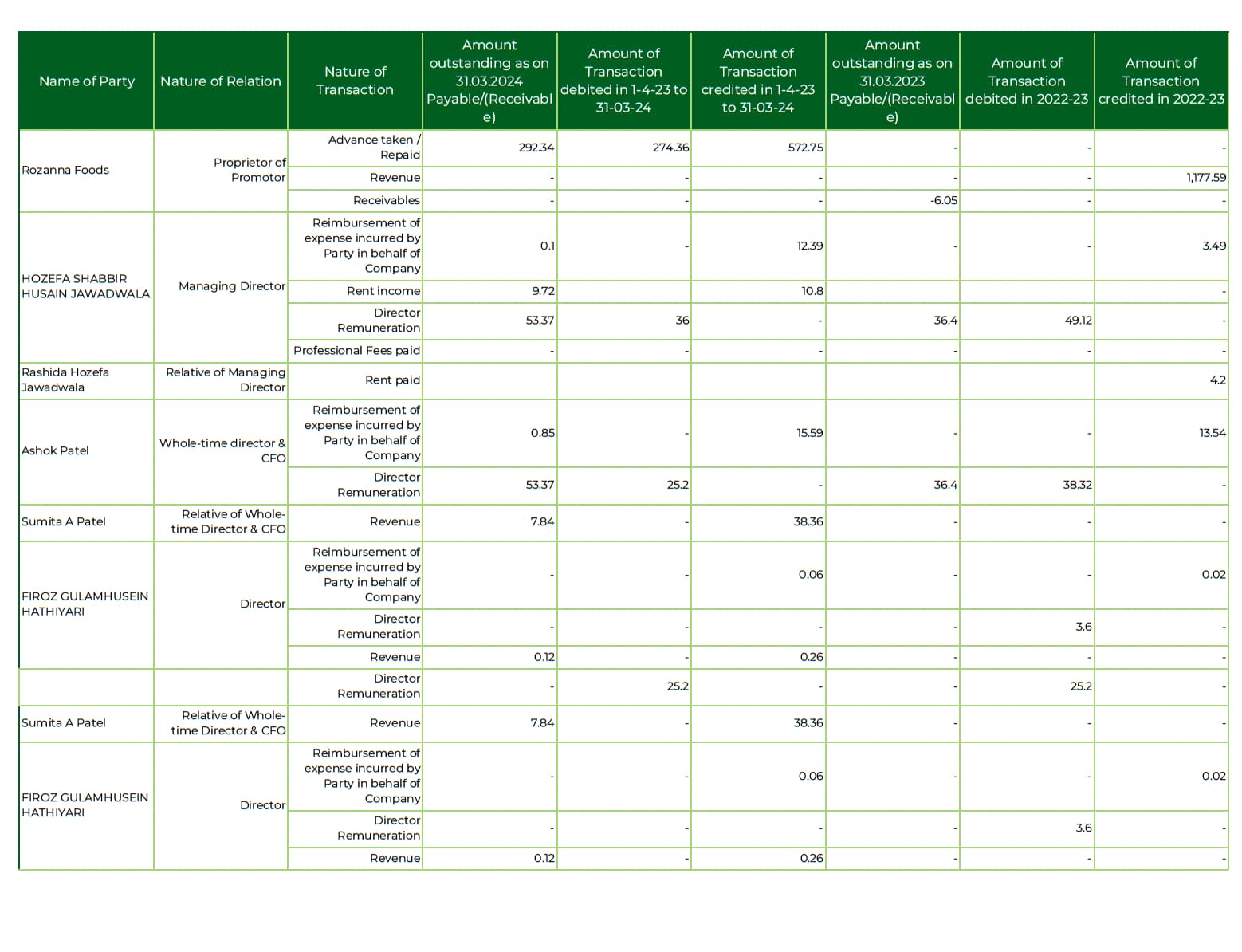

Related-Party Transactions - We need to keep a track of this.

-

Remuneration

Director remuneration increased from 112.37 Lakhs in FY23 to 116.47 Lakhs in FY24 (which is Ok)

- At glance

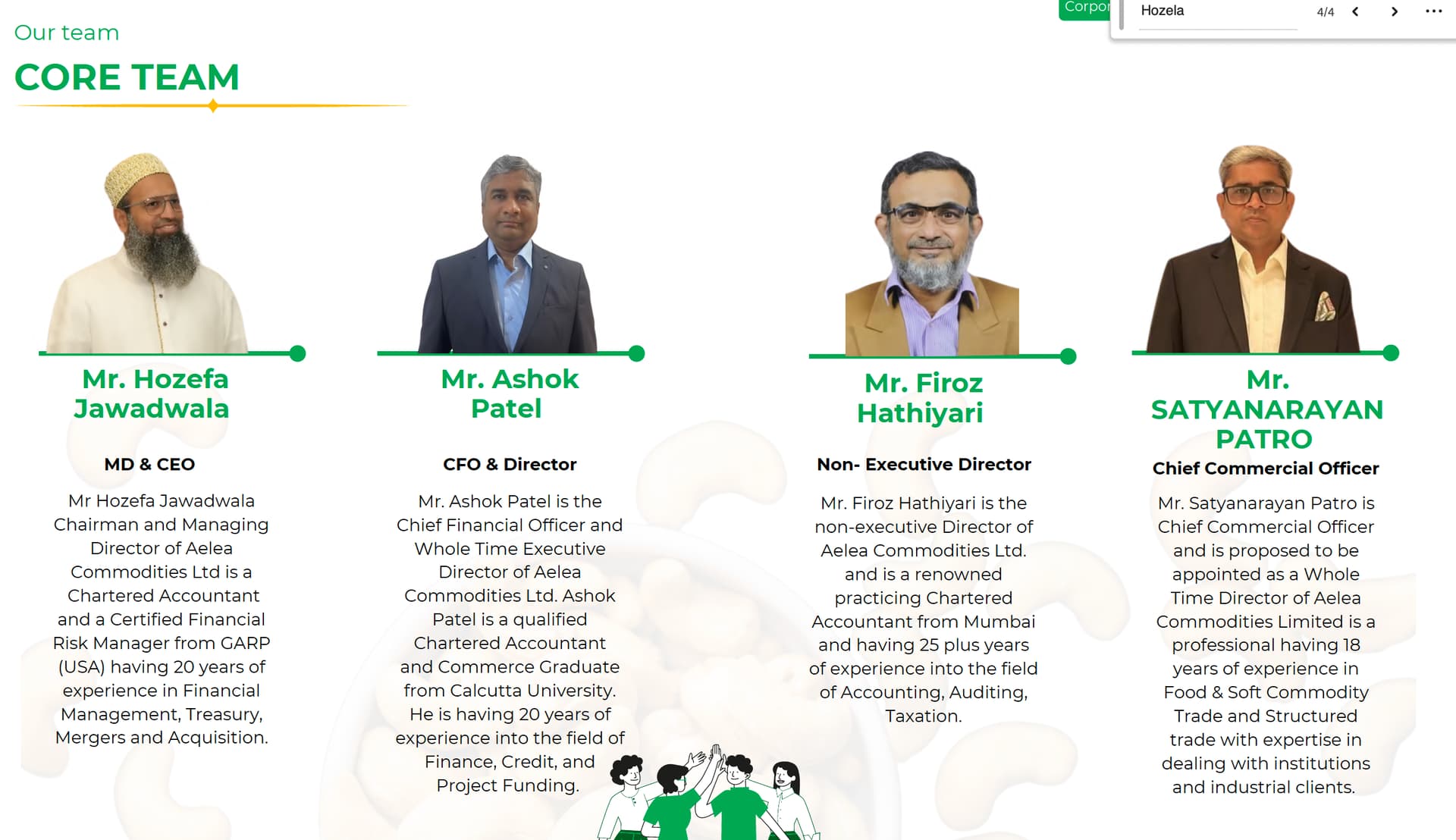

Ques : Tell me something about promoters ?

Ans:

i don’t see any negative news about promoter, please add if you have anything

Hozefa S Jawadwala

(https://www.linkedin.com/in/hozefa-s-jawadwala-7146a58/overlay/about-this-profile/)

This company was in my radar, and today i found out few other good investors also studying this company, so thought of putting the post. I will be adding more details on coming weekend

Bought few qty today to track and study

No recommendation, not a sebi registered. i will sell if i find something fishy