Ganesh Benzoplast a competitor of Aegis, has released a statement about its JNPT LPG terminal (covered here), that its 2 partners have withdrawn their involvement in that project. Need to see plans of Aegis, since they also had got a land parcel in JNPT, and planned for liquid capex. LPG was not yet finalized, but this development from GB might change things for Aegis.

Updates on IPO of Aegis Vopak Terminals: Latest details as released are given below.

Aegis promoters have always treated minority shareholders with equality,visible from the price offered in the AVTL IPO~235. Whether the IPO is over priced or whether AEGIS shares are over priced,it is for the market to decide. Market values pointers such as: sticking to announced capex ,sticking to timelines, prudently managing debt,not making over the top announcements. I am thankful to the value pickr community for Introducing me to this company through the Collaborator’s corner. A shout-out here to @ashwind for keeping us posted with the devlopments with the company,these small updates helps in holding on to the stock during market turbulance. Disc- holding since 2022–5% of pf

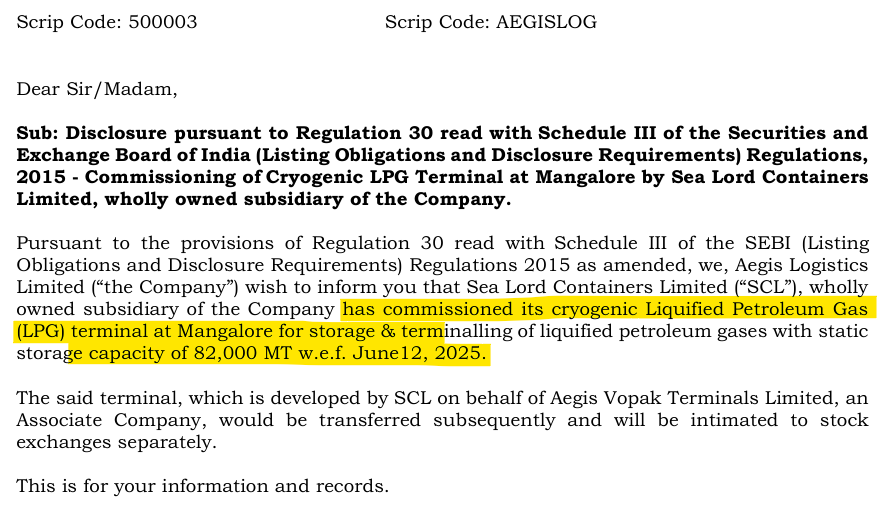

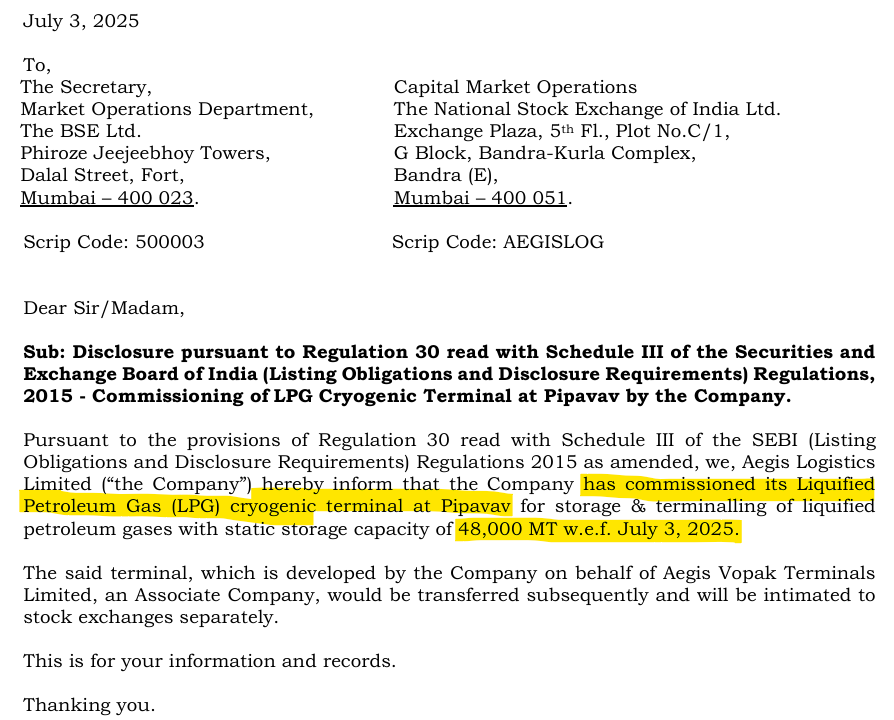

As shared in the Aegis Vopak IPO DRHP, the Mangalore LPG terminal is commisioned. We now wait for the LPG deliveries to start from here, generating revenues for AVTL. I know Aegis was just building the terminal using its EPC expertise, so expect some closing payment in Q1 FY26.

A long wait, and A excellent set of results by Aegis.

Consolidated Profit at 787Cr for Fy25 vs 672Cr in FY24.

Final Dividend for FY25 of Rs.6 and Interim Dividend for FY26 of Rs.2 announced.

Mangalore LPG Terminal transferred to AVTL for 671 Cr.

Pipavav Ammonia Terminal transferred to AVTL for 157Cr.

Kandla assets transferred to CRL (AVTL subsidiary) for 49Cr.

Per Investor Presentation updates:

KEY HIGHLIGHTS

Successful listing of Aegis Vopak Terminal Limited(AVTL)

Started Ammonia storage terminal development at Pipavav for the capacity of 36k MT LIQUIDS DIVISION

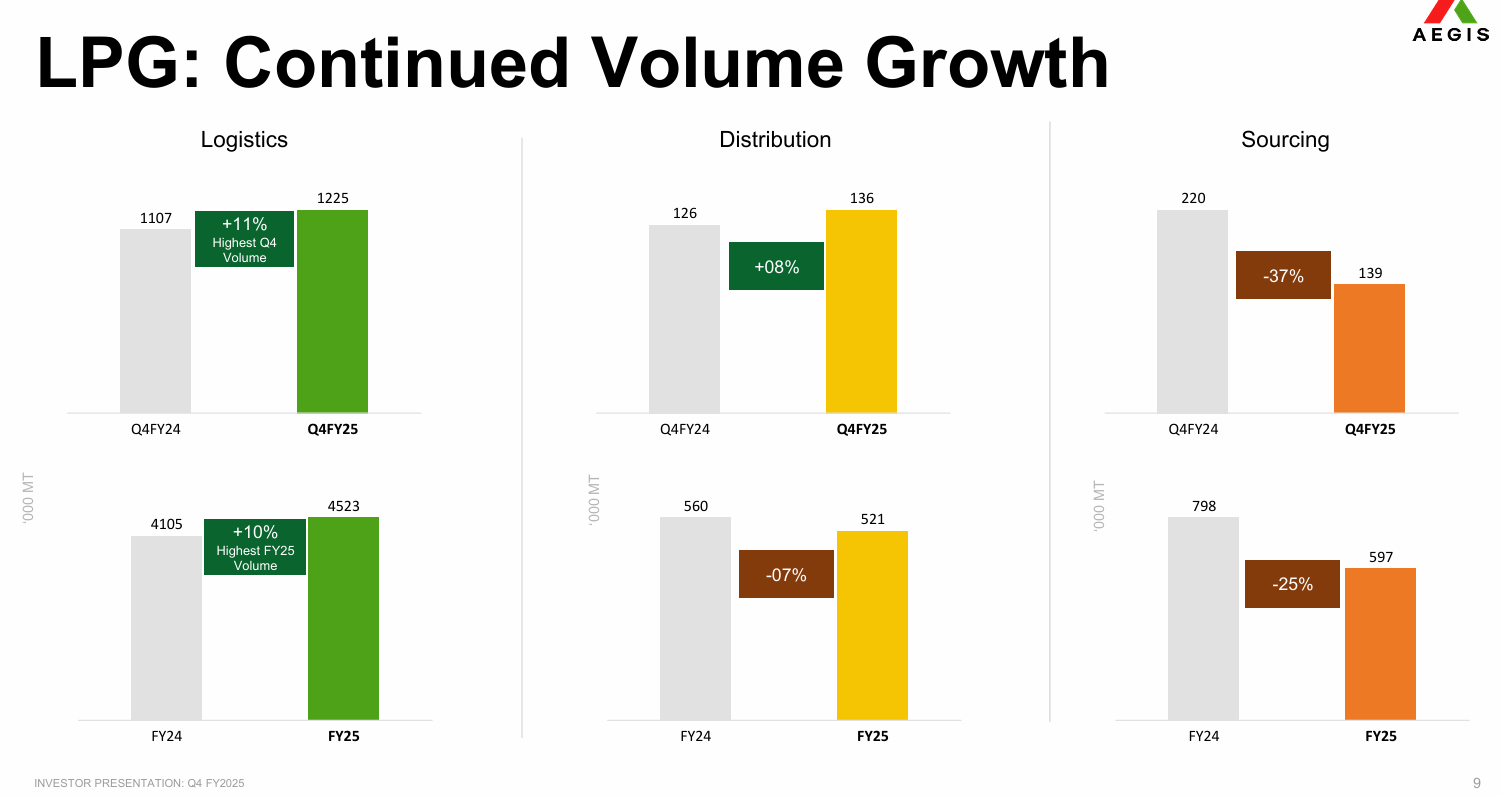

Recorded Highest ever Revenues and EBITDA inQ4

Full commissioning of JNPA liquid storage terminal

Full commissioning of Mangalore Liquid storage terminal GAS DIVISION

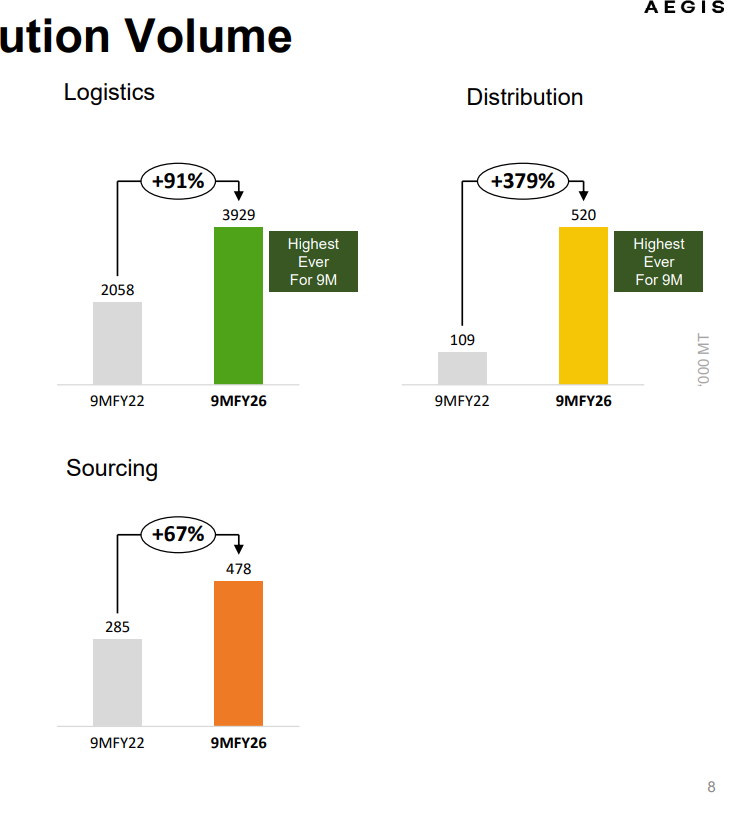

Record Logistics Volumes in Q4

Waiting for Conf calls to restart after the AVTL IPO silent period from this quarter onwards. Also start of revenue generation from Mangalore LPG terminal and announcement of any new projects are eagerly awaited

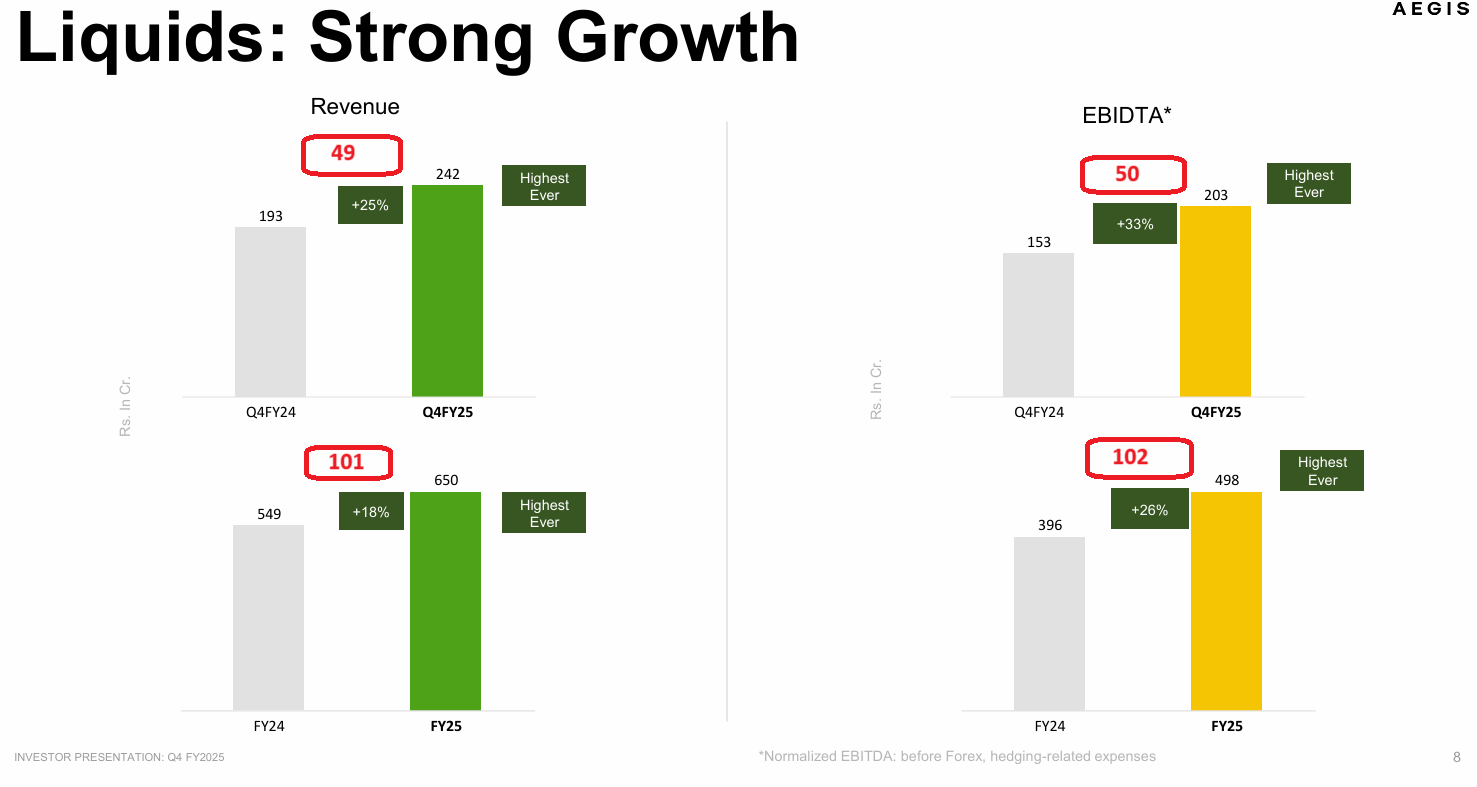

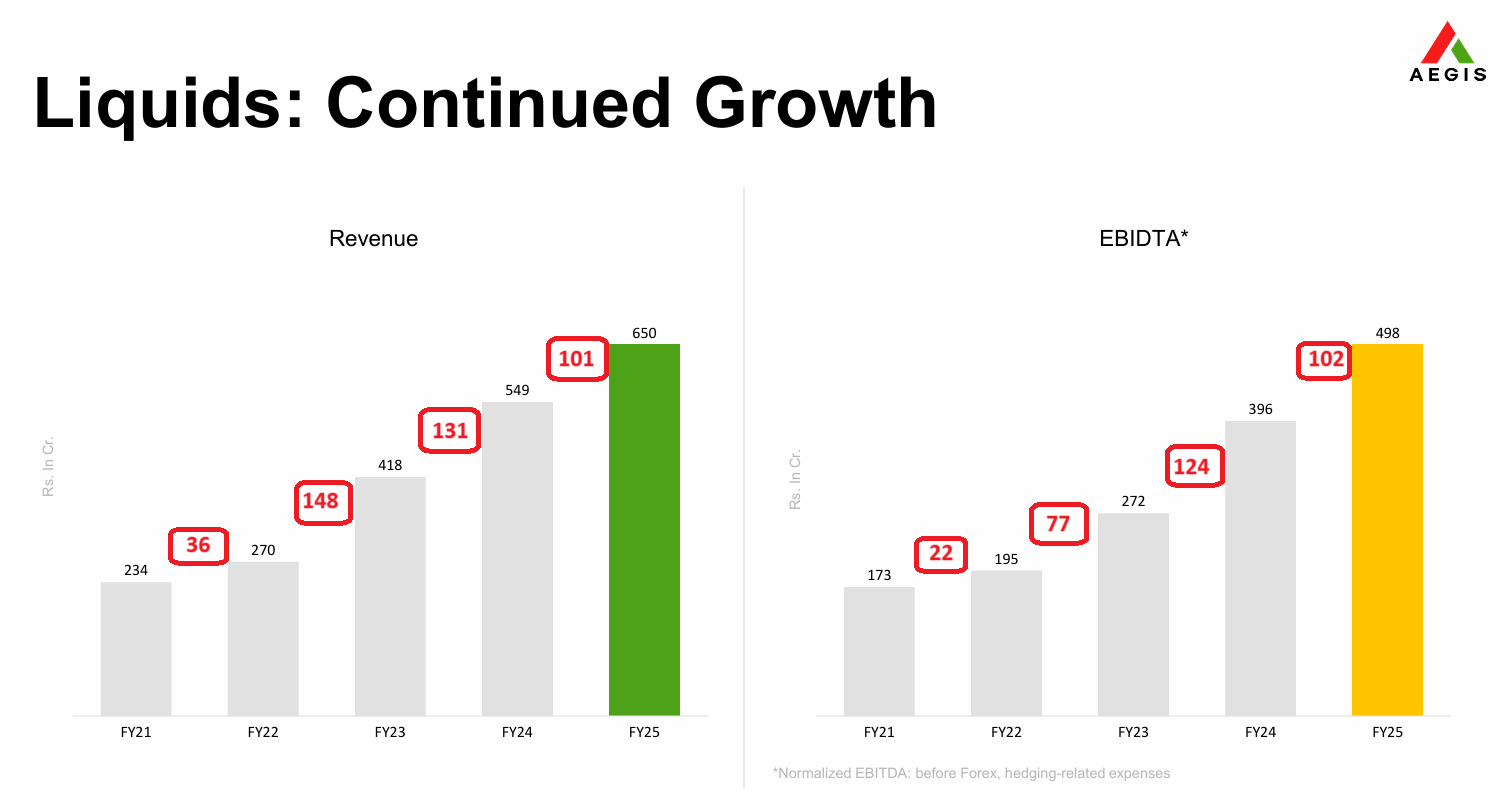

These slides from the Investor Presentation tells a story of operating leverage on Liquids Division. All the additional revenue, is flowing down to EBITDA, basically no additional operational expenses as revenue increased in this quarter. I would invite thoughts from other readers, if they have other insights to add to this.

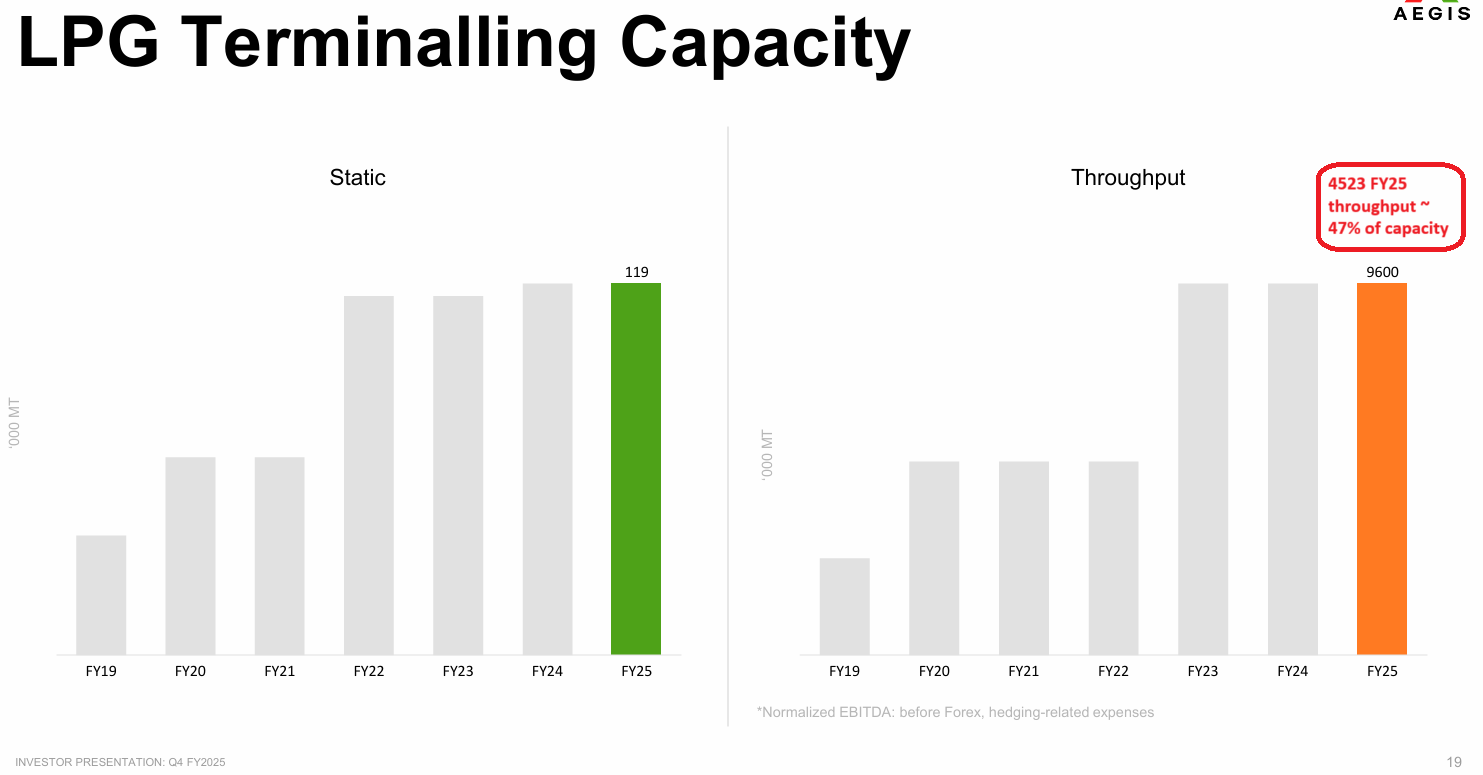

Gas Division was at ~47% throughput capacity utilization, so head room for operating leverage is there, But with Mangalore LPG coming online this % will reduce further + Mangalore operational cost will need to be added. Think there will be adequate spare throughput capacity.

I dont know the revenue breakup of the Gas Division across the Logistics, Distribution and Sourcing divisions. Need to check the AVTL presentation, since it will have only Logistics numbers.

AVTL has only 71,000 MT static capacity (Kandla & Pipavav) compared to Aegis 119,000 MT, so the revenues are difficult to compare. Also AVTL gas division revenue was 276Cr for FY25.

One query please. Will Aegis logistics still be able to consolidate vopak terminal’s result in its financials. Since they now hold less than 50% asking this.

I think till Q4FY25 vopak terminal was a subsidiary of Aegis, as stake sale was in May-25. So, as you said Q1FY26 result will be interesting since it is the first time it will become non-subaidary.

And I feel how the accounting/ consolidation will have a huge impact on Aegis’s result.

Aegis Logistics declared their Q1 FY26 results last week. Links are given below for Aegis and AVTL results, investor presentations and Audio conf call. Quick Summary of Updates are:

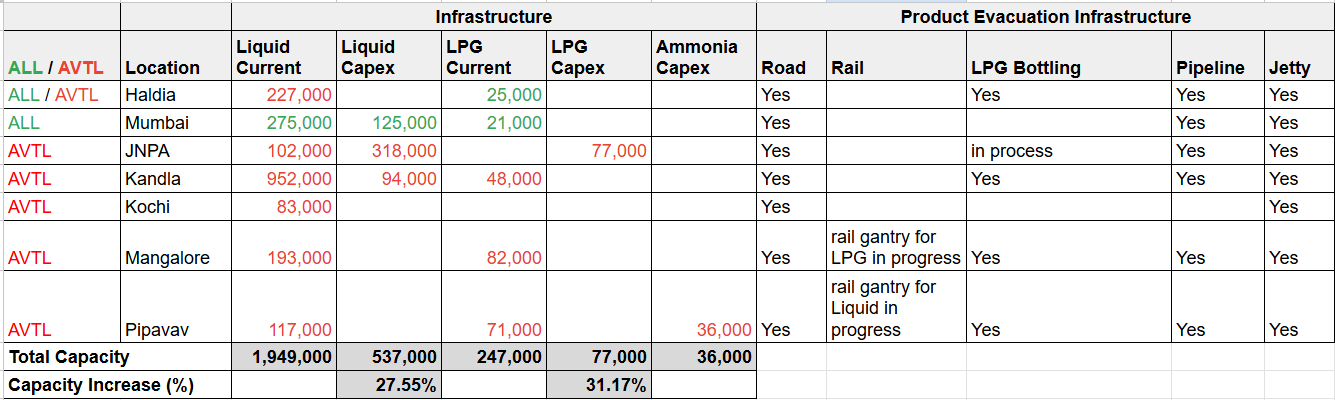

Started Ammonia storage terminal development at Pipavav for the capacity of 36k MT

Announced Phase 2 Capex at JNPA for LPG 77k MT, Liquid 318k cbm and LPG Bottling Plant

Announced additional Liquid Terminal of 94k cbm at Kandla

Location

Updates

Haldia

Participated in additional land tenders

Mumbai

125K Liquid Capex - 50% in Q2 and 50% in Q4 FY26

JNPA

30 acres of land alloted, 1675Cr Capex (Liquid 318k, LPG 77k + bottling plant)

Kandla

Q2 pipeline connection will be available for LPG, VLGC will start working Additional land allotted, Capex in FY27 Signed non binding contract with L&T green ammonia storage in Kandla

Kochi

Allotted additional land for capex of liquid

Mangalore

Allotted additional land for capex of liquid Rail gantry for LPG in progress

Pipavav

Ammonia capex to be ready by Q1 FY27 Rail gantry for Liquid in progress

One more new port is in works, location not disclosed

Long Term Capex: To reach capex of 1.2 billion dollars by next year and expected to reach 5 billion dollars aggregate capex by 2030 funded by a mix of internal accruals and utilizing debt prudently i.e. with a debt gearing ratio of 0.6x capped to 3.5 times of EBITDA

With 25-30% new capacity in the Gas and Liquid segments expected to be operational in FY27, along with a new ammonia terminal, there is a good visibility on growth for FY27.

The management is on target to reach 10,000crs capex by FY27, with 50-60% already capitalized and around 30% in CWIP

The company has a 30% market share in the LPG and Liquid segments. The Gas distribution and Ammonia distribution businesses are 100% owned by Aegis

Discl – Invested for long-term, not a buy sell reco.

I feel it really helps to look at Aegis Logistics on a standalone basis.

EBITDA breakup

FY25

FY26e

Gas

151

159

Liquid

79

118

Distribution

185

236

Total

415

512

I am assuming these numbers for the standalone company. There isnt much details available for distribution, logistics and sourcing business. I feel that piece of the business now contributes almost 50% of EBITDA.

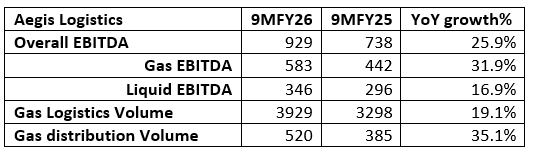

There is a material change in 9MFY26 numbers over 9MFY25 numbers for this piece of the business. But not much details available here. Would be helpful if someone can throw some light on economics of the business; I know EBITDA from distribution is ~Rs.3000 per tonne. What are the growth prospects here and how does logistcs and sourcing contributes to the numbers on revenue and EBITDA.

With the Iran war, and the shortage of LPG (??) reported in multiple cities/sources in India, that begs a question. How did we end up with a shortage within 2 weeks of supply side disruption? Morbi user has to say below:

At his sprawling plant, one among hundreds in Morbi, Vinod Ambani says the industry had last faced such a fearful crisis during the COVID-19 pandemic in 2020-21. Speaking with Mint on the phone, Ambani fears that if gas supplies don’t resume by 15 March, not just his but all factories will have to shut down. refer -

Aegis utilization of all its LPG terminal storage (200k+ MT) was always low, but such a quick run out of gas, indicates the JIT model the entire chain works on.

Aegis always says they earn on throughput on LPG, not on storage. Seems the throughput was taking care of only 1-2 weeks supply, although a bigger part of storage was idle.

Will this change how storage is used in the future? Will this preempt HPCL/BPCL to leverage Aegis infra more to ensure supply is for 4-8 weeks? Can Aegis /AVTL leverage this crisis to increase market share? Interesting challenges for mgmt to overcome.

I hope

Dear @ashwind I have been continously learning from your posts on aegis logistics since 2023 and have held on to the stock bought then despite the turbulations,thanks to your great insights. One thing I found strange is that Aegis runs its own LPG gas distribution network selling small and large capacity LPG gas cylinders by the name of Cikander,Magna etc. Inspite of such a differentiated and forward looking managemnet did the war caught them unaware! I was thinking that they would be using their idle capacity to store LPG and use the current crisis to their advantage. They have often referred to Morbi being an extremely price sensitive market. I would feel that if they had enough stocks Morbi based units would have shifted to Aegis rather than shutting down. In the last concall, management seemed more than confident than ever. Also on the price from Aegis is quoting currently at 14x EV/EBIDTA with is very close to the lowest of 12X which it has ever touched during covid and other such crisis. Sorry to ask you so outrightly ,keeping the uncertainity in mind would you be a buyer at the current price. I feel that given the superb execution track record,if one is buying at the current level or below 600/- it would provide Margin of Safety 3 years hence. Aegis already forms 10% of my Pf,seeking to double it to 20% using the current dust storms.

Thank you @Amit_Agarwal1 for the appreciation and compliments.

I continue to hold a similar view on Aegis, and forms a good part of my portfolio. I did add in the last 1 week and will look forward to participating at lower levels. This is a long term stock (5+ years) from my perspective, it will never give 2x returns in a year kind of stock. I just look at the business growth and the Infra platform that they are building. If the Infra build is growing at 15-20+% p.a. I think the revenue will certainly follow the trajectory. I track the infra build, and hope they continue to sustain the same momentum atleast for the next 4-5 years (handling these hiccups on the way).

I dont know if Aegis currently has sufficient stock or not. Mgmt or company never discusses anything outside the 1 hr conf call window. In a way that is good, I want them focussed on the business. If they missed out on having sufficient stocks (due to earlier business outlook), they now have an opportunity to see how Aegis can leverage its infra to support overall LPG suppy. If leveraged properly, they can grow faster than other competitors. They own the infra, so they are best to leverage. Might as well make the best out of this crisis to get their terminals connected to LPG pipelines and Rail Gantries ASAP. These 2 are the fastest evacuation modes that are available.

Thank you very much @ashwind for reaffirming my assumptions about Aegis as an infrastructure builder. Thanks to your earlier insights only I was convinced about not selling Aegis even when at 1000+ it was 5 times my initial entry price. I have not set in mind not a price target but to hold on to the stock till the time the company completes 10k Crs worth of Gross Block. With stated management intent of returning atleast 20-25% on Gross Block one can get a faint idea of future profits. It also ticks some other filters I am looking for: 1. Singularly focussed management with skin in the game(not a conglomrate) 2. Very long term execution record,delays if any were caused due to external factors,not due to management inefficiency. 3. Relativly less no. of retail shareholders. 4. Minority friendly and transparent Management.

So in effect, it seems wiser to have a closely watched nest rather than a large bucket of stocks.

Mgt Commentary - Similarly, if you look at logistics, throughput. So that gives you somewhere around INR1,100 as revenue. So you have the volumes of logistics, you can multiply by INR1,100. And then if you want the EBITDA, we have always said distribution EBITDA between INR3,500 to INR4,000. So that will give you the math. Is my understanding and calculation correct??

Thank you @Krishna_Kumar for sharing your workings here.

I am curious on the table you shared. If possible can you share, What data source you used to create the table? Are you trying to identify within GAS segment, what parts of the business are generating most revenue/profts, and which are growing at faster pace?

This is a rough draft, and wanted input from the VP Community.

I have attempted to break down the EBITDA of the three gas segments using management commentary on margins and volumes disclosed to understand why there is a significant difference in the earnings forecasts projected by Motilal Oswal and the recent report by IIFL. More over, to assess how much impact the distribution business— which is likely to pick up in the near future—will have on overall earnings.

Mgt commentary on 25% EBIDTA margin on Gross Fixed Asset matches with IIFL projections

Aegis owns about 45% of AVTL (Aegis-Vopak) and hence the consolidated EBITDA attributable to Aegis would be approximately 1200-1250crs (including other income) against overall EBITDA of 1560crs, resulting in EV/EBITA of 18 (around 5 yr median value).

Similarly, PE ratio based on the PAT reported (TTM PAT 970crs, EPS 28) would be 22 whereas the actual PE ratio based on the apportioned EPS would be 28.