Nice summary thread on this business.

Posting India’s quarterly LPG import numbers from now on, instead of monthly. The idea is to look at the broader trend and match the narrative of increasing LPG imports with the actual numbers.

| Apr-Jun '22 (MT) | Apr-Jun '21 (MT) | YOY change |

|---|---|---|

| 4246 | 3495 | 21.4% |

The source of the 2022 data is here and the historical data is here

The above numbers are not exactly comparable as Apr-Jun 2021 was the peak of Covid 2nd wave in India and the growth numbers may look inflated. However, even if we look at 2019 or 2020 numbers, there has been a growth in LPG imports. The “Apr - Jun '19” imports were 3258 MT and the “Apr - Jun '20” imports were 4063 MT.

India’s quarterly LPG import numbers for Q2 below:

| July - Sep '22 (MT) | July - Sep '21 (MT) | YOY change | Apr - Jun '22 (MT) | QoQ change |

|---|---|---|---|---|

| 4463 | 4687 | -4.7% | 4246 | 5.1% |

So, a 4.7% drop on a YoY basis but 5.1 % increase QoQ.

In Q1, FY23, Aegis did 637 MT of gas volumes (slide 5 of investor presentation). With India’s total import volumes at 4246 MT in Q1, that implies 15% market share.

Aegis has been hovering around the 15% market share for a while now. It will be interesting to see how that number moves with VLGC compliant jettys coming in at Pipavav and Kandla terminals getting operational.

There are two threads on Aegis, realised it today. Not sure, but will add updates on this thread. Some immediate term good news is that Aegis might get boost in gas distribution volumes due to probable pice differential increase between LPG and Natural gas.

Two news - Govt cuts agri cess (15%) on LPG and Gujarat Gas hikes natural gas rates by ~6%. this might benefit Aegis gas distribution volumes.

Aegis Logistics

ALL is present in 2 segments, Liquids and Gas. In liquid division, ALL provides import, export, storage, and logistics services, as well as all types of chemicals, petroleum, oil, lubricant (POL) products and vegetable oils. In gas division, ALL captures the complete logistics value chain starting from sourcing, terminaling to distribution of LPG. The consolidated LPG static storage capacity is 115,000 MT & total liquid storage capacity of 1,603,000 KL, to import/export LPG, chemicals and petrochemicals, across Mumbai, Haldia, Kochi, Pipavav, Kandla, and Mangalore

| Date of report: | 01-07-2024 | Competitor PE | 53.5 | Sector | O&G (Mid and Downstream) |

|---|---|---|---|---|---|

| CMP: | 859 | Current PE | 50 | No of Years | 68 |

| Market Cap: | 28312 | Highest PE | 53.5 | Key Products | Gas and liquid fuels’ logistics and trading |

| ROCE / ROE | 15% / 15% | Lowest PE | 3.5 (2013) | Key Competitor | Confidence Petroleum, GSPL, Petronet LNG, IMC, Petregaz, Kiran Group |

Business Model and Industry Analysis

Overview:

Aegis primarily operates in 2 segments, viz. Liquids and Gas.

Liquids Terminals - 3rd Party liquid logistics provider for oil and hazardous chemicals serving oil marketing co, refineries and other MNCs. In Liquids, contracts are usually 1 year - fixed price Take-or-Pay, providing revenue visibility for the capacities. Some spot contracts and sales do happen though. Nature of liquids store largely govern revenue (Vegetable oils are lowest revenue, whereas acids/hazardous chems might pay 8-10x more than vegetable oils). Liquids contribute to 5% of the revenue and ~33% of EBITDA

Gas Terminals - 3rd Party Gas logistics providing storage and terminal solutions for LPG, Propane and other gases. This division, along with other gas business contributes to 95% of the revenue & ~67% of EBITDA

Other Gas business - Gas sourcing and trading (60% JV with Itochu), LPG distribution (Home, Commercial, Industrial, Auto LPG)

Other business – Supplying Bunker (Marine) fuels (Negligible contribution to revenue/EBITDA

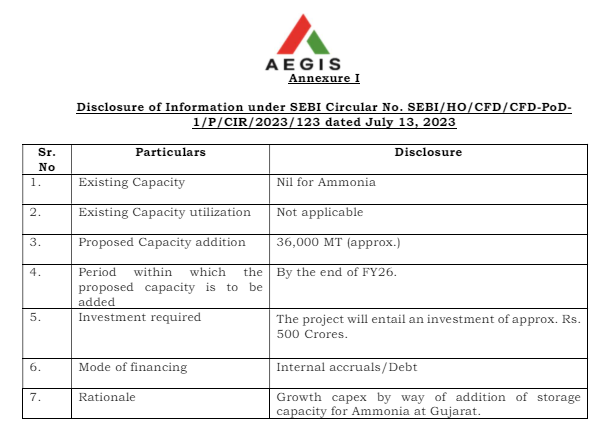

Aegis has also started constructing Ammonia terminal of ~36,000 MT at Pipavav catering import/export. EBITDA potential for the plant is ~120 Cr at max asset turn (3x). Growing demand from chemical sector is expected to further increase demand for Ammonia handling capacity. Currently, all major chemical and fertilizer plants have their own storage facilities

Industry Growth:

Aegis is planning to play on transition to cleaner fuels (Primarily LPG and CNG/PNG. Aegis plays in LPG). Currently, 17% of India’s energy needs is catered by biomass. Bulk of the industrial fuels used are dirty fuels (45% being coal). Government’s policy push towards a more gas-based economy is also expected to play a large part. The largest benefit of LPG over CNG is portability, where LPG can be transported by pipeline, rail, road etc, natural gas can be transported only by pipelines, limiting its reach.

Currently, domestic LPG demand is ~31 MnT, of which ~67% is being imported (Till 5 years ago, domestic production exceeded imports). This is further expected to grow at ~6-7% pa. LPG is also used in production of fertilizers, apart from its use as fuel

The consumption of chemicals in India is expected to rise by 9-10% annually over the next few years

Capacity Utilisation:

Gas terminals are currently being utilized at ~50%, whereas liquids are being utilized at ~87%. Further capacity utilization is expected in gas business

Opportunities:

Growing chemicals and fertilizers sector, government’s push towards gas economy, LPG’s inherent benefit in terms of cost and portability over CNG as well as government’s policy push towards cleaner fuel all are big tailwinds for Aegis. The group has demonstrated execution capabilities in the past as well and has made their JV with Itochu work. Same can be expected with Vopak JV, where bulk of the business is being housed and all future growth is expected

Risk:

- Policy risk – Strong policy support for LPG and clean fuels have driven gas segment’s growth. Also, liquid division is dependent on policies regarding ports and infrastructure, chemicals business as well as trade agreements. Should the push turn towards NG instead of LPG, it can hurt Aegis. However, Aegis is entering gases other than LPG (Ammonia to begin with) and LPG has some inherent operational and cost benefit over CNG

- Higher calorific value - 12500 kcal/scm against 10,000 kcal/scm of NG

- Easy storage requirements - Natural gas requiring -160°C and 200-bar pressure

- Portability – Can be transported over road/rail/pipeline against NG (Only Pipeline)

- Cost – LPG is ~6-7% cheaper than CNG

- Geopolitical risk – Geopolitical issues impacting O&G, chemicals trade will impact the terminals business in a significant way. The Liquids division is generating ~33% of the EBITDA and bulk of its revenue comes from ~1-year fixed price take-or-pay contracts, so part of this risk is mitigated.

- Exchange rate risk – Company has managed to keep its foreign exchange losses to a minimum. Bulk of the foreign exchange risk comes from the gas sourcing business, where the company has managed to enter back-to-back contracts with common pricing terms, forex rate, and credit period terms. Further, balance open exposure is hedged using derivatives

- Business Model Risk – Company faces threat from following areas -

- PSU refineries are also building LPG and liquids storage terminals. They are key customers of Aegis

- CGD penetration pushed by PNGRB can lead to increased use of PNG over LPG

Future Expansion:

Aegis usually incurred 200-300 Cr capex/year till now. Post merger with Vopak, JV plans to incur 500-600 Cr/year over the next 5-6 years to execute “Chain of Pearls” strategy of terminals across India’s coast

Currently, it is undergoing expansion at Kandla (Lq), Mangalore (Lq), Kochi (Lq), Pipavav (LPG). It is also constructing new LPG facility at Mangalore (85,000 MT) and new Liquids facility at JNPT (110,000 KL)

Post expansion, total liquids facility is expected to be ~2.3 Mn KL by FY25 and Gas facility to be 245,000 MT

Competion:

Currently, Aegis is the dominant player in liquids and gas handling business. Although, it faces significant competition in LPG distribution business from OMCs. Further, OMCs are also building their own liquid and gas handling capacities at the port

Management:

- Management is clear and genuine on communication. Further, their acquisitions are all on point, and fit well in overall story. Capex are done with IRR target of 25%

- Positives: Salary in line with profits (<5%), no anti-minority shareholder decisions, RPT (No significant RPT), resignations, family and succession planning, excessive salaries and other extravagant spends, civil/criminal cases, fraud/scam involvement, royalty/brand fees/other means to defraud minority holders, complex business models, unnecessarily complex/flowery language in communications, consistent dividend payment

- Concerning Points – Lack of clarity on debt reduction plan. Company has long runway to invest additional capital at ~20-25% IRR, however debt reduction plans are not mentioned in communication as such

Institutional Investor:

FII and DII continue to hold 23% (17% in Jun’21)

Historical Data and Financials

Profit N Loss Account:

* Sales have historically grown at **7%** over last 10 years and at **22%** over the last 3 years

* Margins have expanded from 4% in FY15 to ~13% in FY24

* Earnings have historically grown at **21%** over last 10 years and at **37%** over the last 3 years

* Ammonia terminal and added capacities are expected to grow EPS by 25% over coming 2-3 years

Balance Sheet:

* AVTL has taken on debt to fund the purchase of assets from ALL. Historically, the company has managed to keep debt well within the limits. Interest coverage ratio is at 8. Similar increase in cash balance can also be seen, and net debt/equity is at ~0.2

* Receivables have fallen from 19% 3 years ago to 6% in FY24

Cash Flow:

CFO/PAT good (124%) over long term

Valuation and future potential:

| Particular | Current | 52W High | 52W Low | Historical High | Historical Low | Industry Median |

|---|---|---|---|---|---|---|

| Price | 807 | 888 (06/2024) | 106 (5/2023) | 888 (06/2024) | 2.8 (2009) | - |

| PE Ratio | 50 | 51 | 19.5 | 96 | 3 | - |

| EPS | 16.2 | 16.2 | 16.2 | 16.2 | - | - |

| Price/Book | 7.3 | 7.4 | 2.8 | 14.1 | 0.7 | - |

| EV/EBITDA | 26.2 | 26.6 | 10.7 | 41.2 | 1 | - |

| ROCE | 15% | - | - | - | - | - |

No direct competitor listed (GSPL, Gujarat Gas, Confidence, Petronet etc are competing in few segments)

Valuation:

- Company is growing revenue (22% CAGR over last 3 years) and profits (37% CAGR over last 3 years) at good rate, however, it is valued at a PE of ~50, with no growth/re-rating scope left

- Risk for this band being company might revert to mean-valuation of ~25-30 (Last 3 years) which presents a downside of ~40-45% (Considering increase in EPS as well)

Future Potential:

- Company is expected to grow and hit ~10,000 Cr revenue by FY26 with maintained OPM margins

- At current valuation, there is no scope for re-rating. For me personally, having entered at ~400 in early Feb, that provides some margin of safety

Soft factors for consideration:

- Company has good management and has executed capex well in past

- Long runway for additional capital investments with high IRR (~25% is management’s usual target)

- Company has prudently used inorganic acquisitions & JVs to grow, partnering with the big names in respective industries

Disclaimer: This is a study report prepared to track a personal position, not for any decision making or investment advisory.

Made by: Yash Chandak (72193 98497)

Date:1st July 2024

Aegis has announced filing of the Draft Red Herring Prospectus for IPO of AVTL for raising Rs.3,500Cr. I do not see the DRHP link on the SEBI website yet( SEBI | Public Issues), so cannot share more details.

Proposed initial public offering (“IPO”) of Aegis Vopak Terminals Limited

So recently that had done a Private equity placement with the 360 One Funds, @Rs.235/share for 475Cr. (Link)

Since the IPO is a Fresh Issue for Rs.3500Cr, and assuming same valuation of Rs.235, this will be for 14.89Cr shares. But I suspect this might be at a higher valuation. Current equity is 98.88Cr, this will be a ~15% equity dilution. This also pushes Aegis equity stake below 50%.

At Rs.235 IPO Price, Aegis stake will be ~43.54% post IPO, whereas at Rs.350 ![]() IPO Price, Aegis stake will be ~45.5% post IPO. I do not know what the IPO price will be, with market conditions like this.

IPO Price, Aegis stake will be ~45.5% post IPO. I do not know what the IPO price will be, with market conditions like this.

I suspect till the actual offer opens for bidding (~3-6months), we might get a lot of news/new projects (ammonia, etc) related coming out to higher the IPO price.

Is it just me, or are others also noticed it?

Aegis did not have a Conf Call after the Q3 results. I know there were some Investor Gatherings (2 or 3) in Mumbai in Feb 2nd/3rd week. But they could have a conf call in 4th week of Feb.

The long awaited KGPL pipeline will be opened by June 2025 as per this article. With not much to impede or slow down progress (elections, weather, etc), we should see this open before the monsoons.

Aegis had built Kandla and Pipavav terminals for LPG with this pipeline in mind. With a capacity of 8.3 million tons of LPG per annum, this pipeline can be used to evacuate most of the terminal capacity of Aegis. We will need to see how quickly the LPG rampup happens post June. Per the earlier news items, some segments of the pipeline were activated earlier.

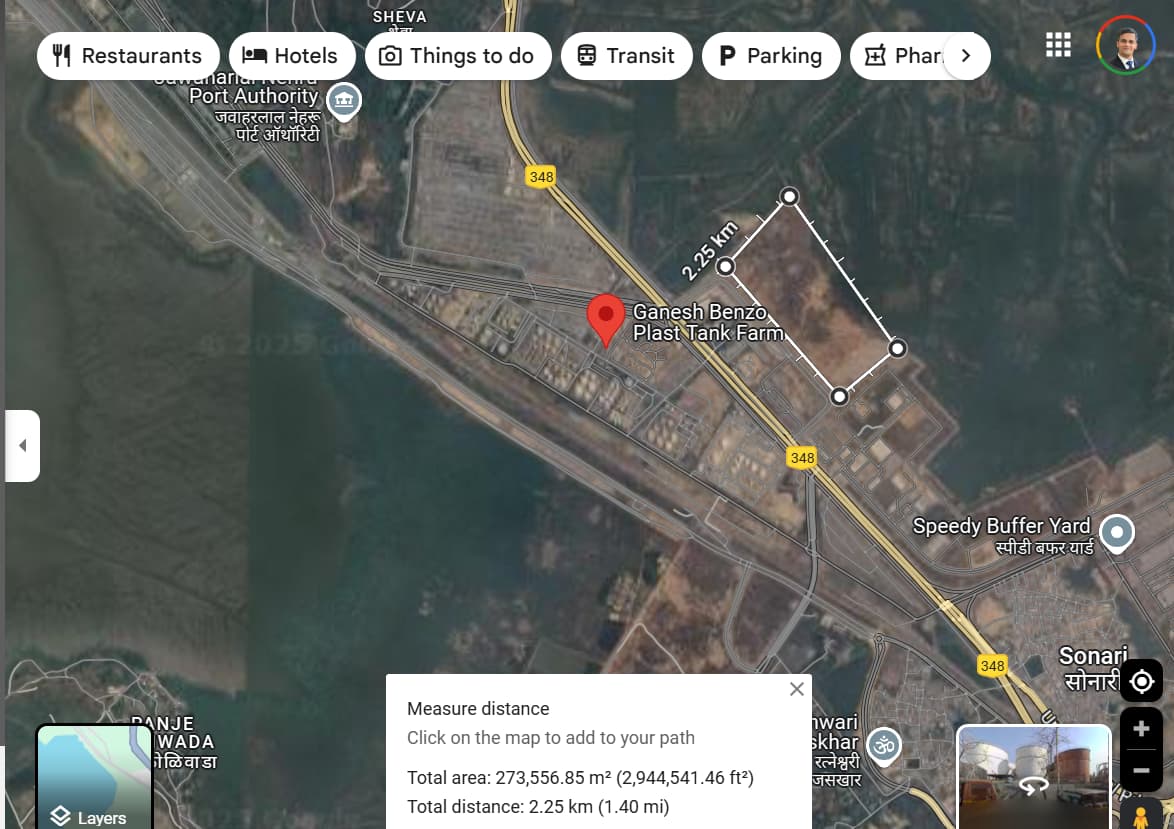

One more update on JNPT location of Aegis - my update on Ganesh Benzo thread - Ganesh Benzoplast - Cash rich chemical storage/tank king - #308 by ashwind Aegis location is approx spot marked by white rectangle (some portion of this).

The opening of the Kandla-Gorakhpur LPG Pipeline (KGPL) by June 2025 is likely to have a significant positive impact on Aegis Logistics, particularly with respect to its Kandla and Pipavav LPG terminals. Below is an analysis of how this development could affect Aegis Logistics based on the information provided and broader context:

Background Context

KGPL Pipeline: The Kandla-Gorakhpur LPG Pipeline, spanning 2,805 km, is a major infrastructure project jointly managed by Indian Oil Corporation (IOCL), Bharat Petroleum Corporation Limited (BPCL), and Hindustan Petroleum Corporation Limited (HPCL). With a capacity of 8.3 million tons of LPG per annum (MMTPA), it aims to transport LPG from import terminals and refineries on India’s west coast (Kandla, Dahej, and Pipavav) to bottling plants across Gujarat, Madhya Pradesh, and Uttar Pradesh.

Aegis Logistics: Aegis is a leading player in India’s LPG logistics sector, operating terminals at key ports including Kandla and Pipavav. These terminals were strategically developed with connectivity to the KGPL pipeline in mind, positioning Aegis to benefit from efficient LPG evacuation and distribution.

Potential Impact on Aegis Logistics

Increased Throughput Capacity Utilization

Aegis’s Kandla and Pipavav terminals are designed to handle significant LPG volumes. The Kandla terminal, with a static capacity of 45,000 metric tons (MT) and a throughput capacity of 4 MMTPA, and the Pipavav terminal, with a static capacity of 22,000 MT and throughput capacity of 1.4 MMTPA, together contribute to Aegis’s total throughput capacity of around 10 MMTPA across its facilities.

The KGPL pipeline’s 8.3 MMTPA capacity can evacuate a substantial portion of Aegis’s terminal throughput. This could lead to higher utilization rates at both terminals, boosting revenue from storage and handling fees, which are tied to throughput rather than just static storage.

Revenue Growth

Aegis earns revenue primarily through logistics services, including storage and handling of LPG for oil marketing companies (OMCs) like IOCL, BPCL, and HPCL—the same entities managing the KGPL pipeline. With the pipeline operational, these OMCs are likely to increase LPG imports and distribution through Kandla and Pipavav, directly benefiting Aegis.

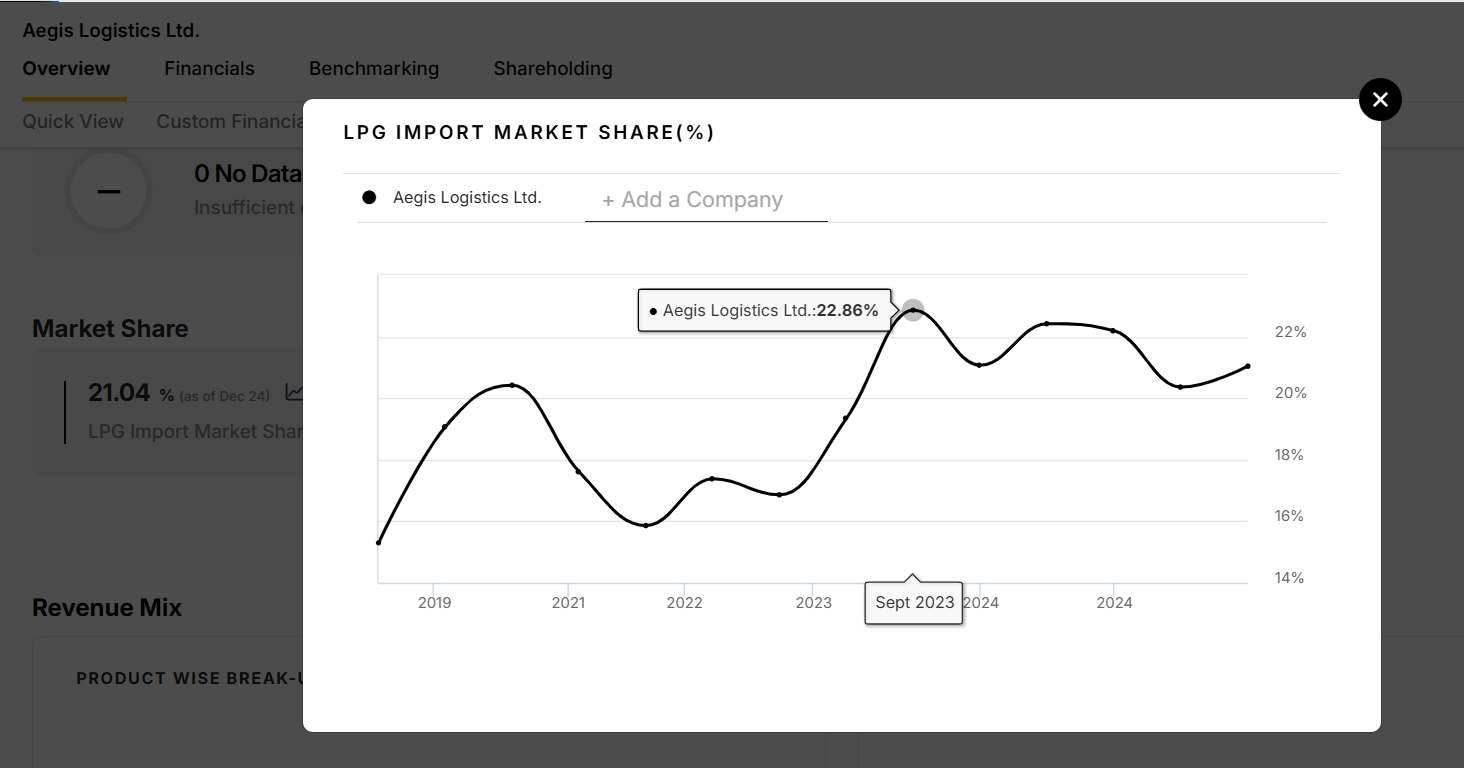

Historically, Aegis has captured a significant share of India’s LPG import market (around 19% in FY19, with plans to reach 30-33% in the medium term). The pipeline’s activation could accelerate this growth, potentially pushing Aegis closer to its target of 40% market share as its throughput capacity aligns with rising demand.

Operational Efficiency and Cost Benefits

The pipeline offers a safer, more economical, and environmentally friendly mode of LPG transport compared to road tankers. This shift reduces reliance on road-bridging, which is costlier and less efficient, allowing Aegis to optimize operations at Kandla and Pipavav.

With direct pipeline connectivity, Aegis can offer faster and more reliable evacuation to OMCs, strengthening its position as a preferred logistics partner.

Ramp-Up Dynamics

The speed of LPG volume ramp-up post-June 2025 will be critical. While some pipeline segments may have been activated earlier, full commissioning by June 2025 will enable end-to-end connectivity. The absence of major impediments (e.g., elections or monsoons) suggests a smooth rollout, but the actual pace of volume growth will depend on OMC bottling plant readiness and LPG demand in northern and eastern India.

If the ramp-up is swift, Aegis could see an immediate uplift in throughput volumes. A gradual increase, however, might delay the full financial impact until late 2025 or early 2026.

Strategic Positioning and Market Share

The Kandla terminal’s location on the KGPL grid, combined with Pipavav’s planned connectivity by mid-2024 (as per earlier reports), positions Aegis to serve the growing LPG demand in northern and eastern India. This aligns with India’s rising LPG consumption (projected to reach 40 MMT by FY35 from 23 MMT in FY19), driven by government initiatives like the Pradhan Mantri Ujjwala Yojana.

Aegis’s partnership with Vopak (via the Aegis Vopak Terminals Ltd joint venture) further enhances its ability to capitalize on this opportunity, leveraging Vopak’s global expertise and financial backing to expand terminal operations.

Challenges and Uncertainties

Competition: Other players, such as APM Terminals Pipavav, are also enhancing LPG handling capabilities (e.g., Very Large Gas Carrier compliance and rail sidings). Aegis will need to maintain competitive pricing and service quality to secure volumes from OMCs.

Demand Variability: While LPG demand is stable due to domestic cooking needs, any delays in bottling plant integration or unexpected economic factors could temper the pipeline’s immediate impact.

Infrastructure Readiness: Although the pipeline is on track, any last-minute technical or regulatory hurdles could delay full operational benefits for Aegis.

Conclusion

The opening of the KGPL pipeline by June 2025 is poised to be a game-changer for Aegis Logistics’ Kandla and Pipavav terminals. It enhances Aegis’s ability to handle and evacuate large LPG volumes efficiently, likely driving higher throughput, revenue, and market share in India’s growing LPG logistics sector. The extent of the impact will hinge on the speed of the post-June ramp-up, but with Aegis’s terminals purpose-built for this pipeline, the company is well-positioned to see substantial operational and financial gains starting mid-2025.

Agree with most points, but want to caution that 19% market share rising to 40% is pretty stiff, but if that happens, the profitability will be huge, since most of additional revenue of the market share increase will flow to the bottom line due to cost dynamics of this industry.

On a seperate note the AVTL IPO, seems the current status is " Draft Offer Document in relation to which clarifications are sought by SEBI and response from LM is awaited" as of 25 February 2025. The IPO seems to be timed with the pipeline opening for sales/profits boost just around the IPO.

Very well written and lucid,maybe the market is pricing this development that is why Aegis has not corrected much ,it’s still up 100% on YoY basis. Disc- Invested since September 2023,from 300 levels, hoping to add when it falls,sadly no luck. Markets are smarter than individual investors.

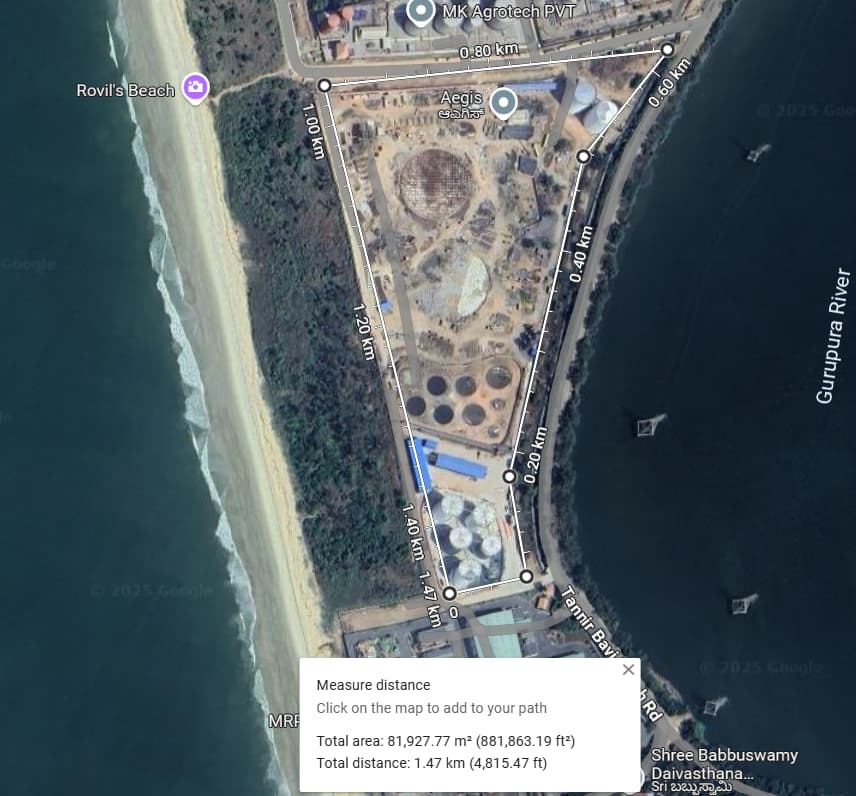

Mangalore LPG project site pictures.

The 2 domes inner structure seems to be done, outer cladding work is in progress. Mostly side cladding is completed, but top is pending as per picture below.

Location Link - https://maps.app.goo.gl/FWEvzVSDxRYdMZ5E9

LPG tanker owners announce indefinite strike; six southern states to face supply shortage

Although the stike is by LPG tanker owners towards Oil companies latest rules/regulations, this will affect evacuation of gas from terminals, but Aegis does not have much in south India as of now. Will it benefit in any way? I do not think so.

Does anyone know what % of gas is evacuated from Aegis Terminals by Road, Rail, Pipeline, etc modes? And which terminals are heavily dependent on any particular mode?

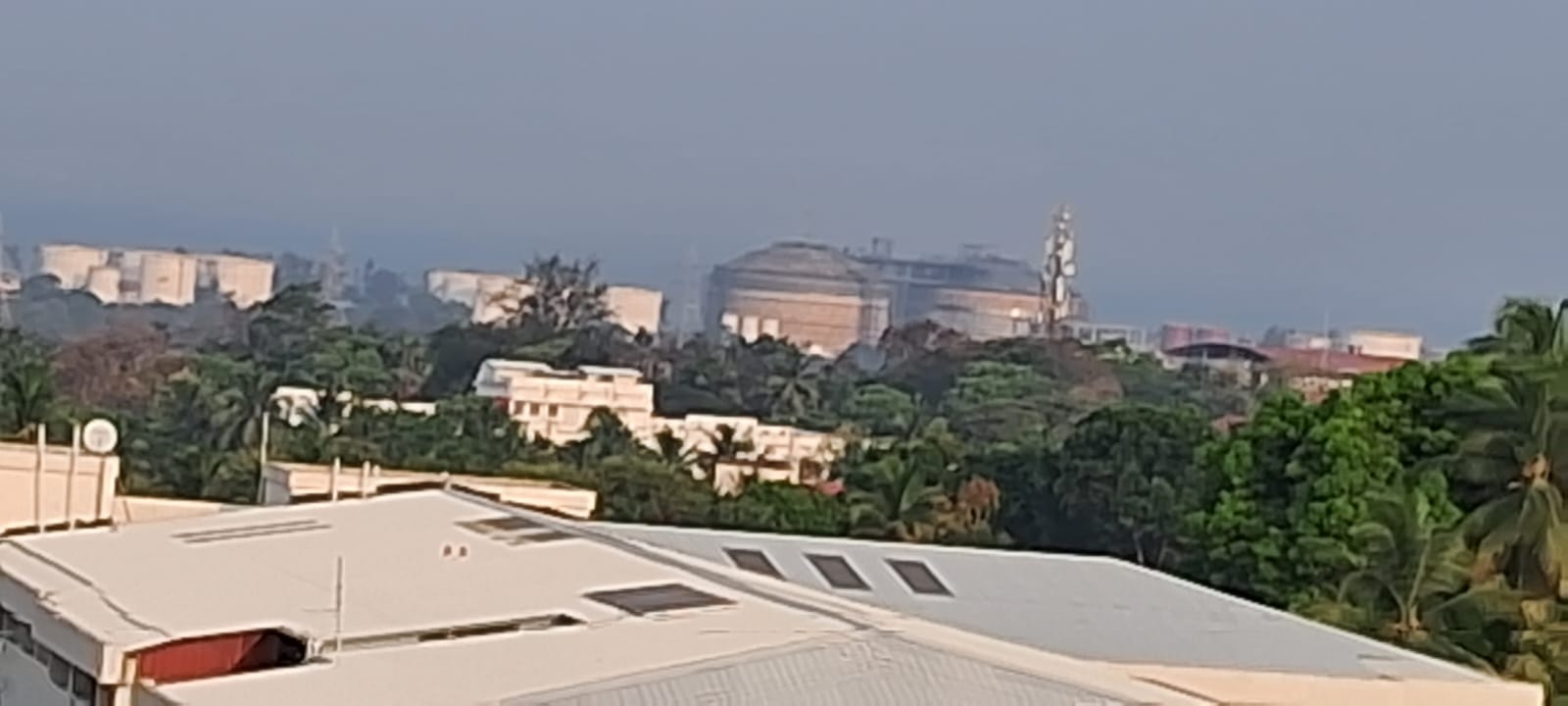

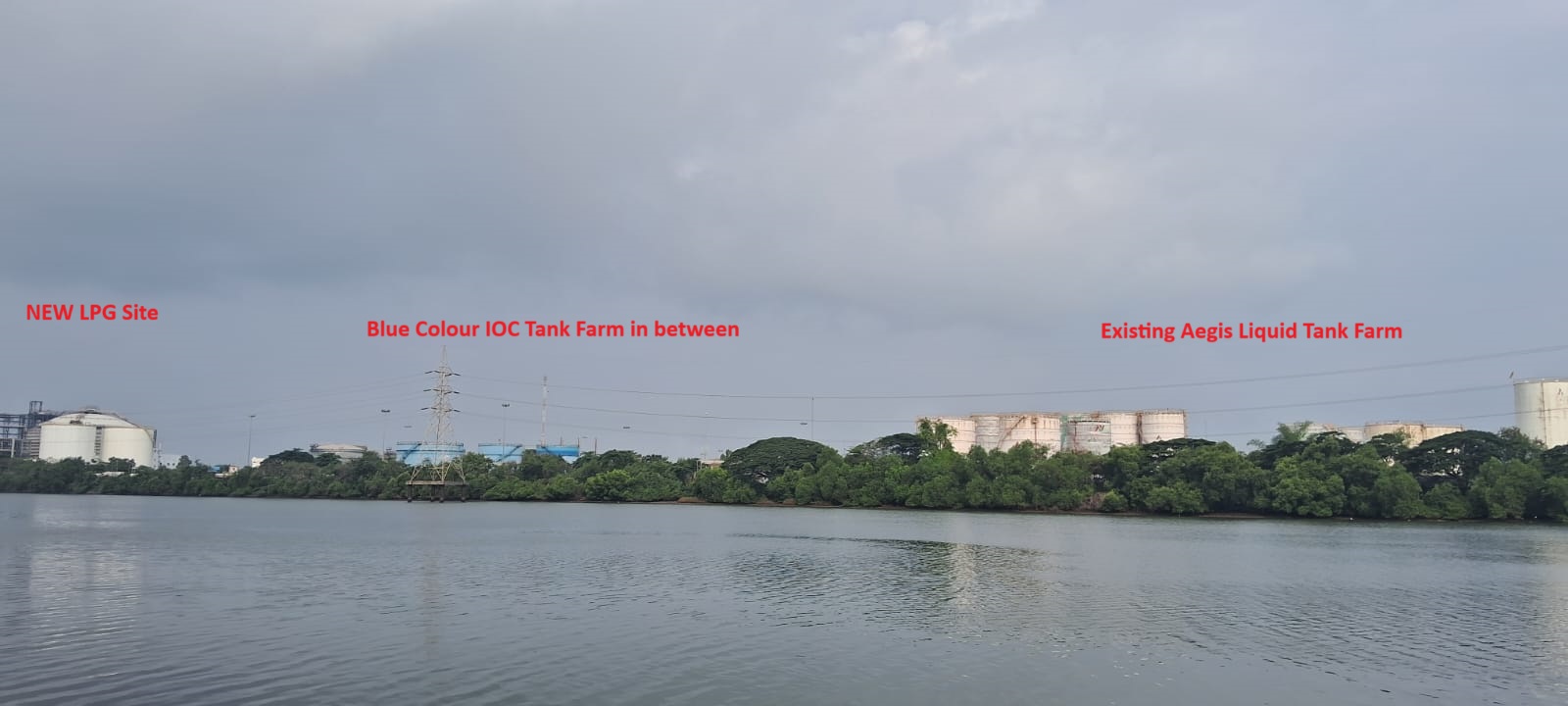

Mangalore Update for Aegis - Today morning was taking a stroll on the riverside oppposite to the Aegis Terminals (old Liquid and new LPG). Below are the latest photos.

The LPG structure is fully up, but I think the external cladding work is still not completed. Possibly another 6 months for completion. Hope they have the Conf call this quarter to update on progress.

Below is MAP of mangalore port - NMPA Map. The portion marked in RED are the Aegis Plots. Berths 9,12 and 13 handle LPG, and are near to the Aegis Plots, 7.3 MTPA total capacity. The capacity of each Berth is given below:

- Berth 9 - Multi user oil berth operated by NMPA. Draught: 10.50 mtrs, Length: 330 mtrs. For handling LPG/edible oil/chemicals Capacity : 2.20 MTPA

- Berth 10 - Oil berth operated by NMPA. Draught: 14.00 mtrs, Lenth: 320 mtrs. For handling Crude and POL products for MRPL(captive user) Capacity : 9.30 MTPA

- Berth 11 - Oil berth operated by NMPA. Draught: 14.00 mtrs, Lenth: 320 mtrs. For handling Crude and POL products for MRPL(captive user) Capacity: 8.70 MTPA

- Berth 12 - Muti user Oil berth operated by NMPA. Draught: 12.50 mtrs, Lenth: 320 mtrs. For handling LPG/POL products/Chemicals Capacity : 2.30 MTPA

- Berth 13 - Muti user Oil berth operated by NMPA. Draught: 14.00 mtrs, Lenth: 350 mtrs. For handling LPG/POL products/Chemicals Capacity : 2.80 MTPA