Here is the 2nd stock in my portfolio that I own -

Dr Lal Pathlabs Ltd

I have always been keen on investing in the diagnostics sector in India. This is because of the large unorganized segment present in the market, and the high CAGR of the industry itself.

These twin tailwinds of size of the pie growing, along with the opportunity to grab of a larger slice of the pie for oneself, has the potential for outsized rewards in the long-term. (Demonstrated by PE/VC investments in the space, looking for abnormal returns.)

However, one must be wary of key risks, especially pertaining to Dr. Lal, which are -

- Acquisition Risk (Inorganic Growth)

- Evolving Business models (which makes the industry somewhat unpredictable)

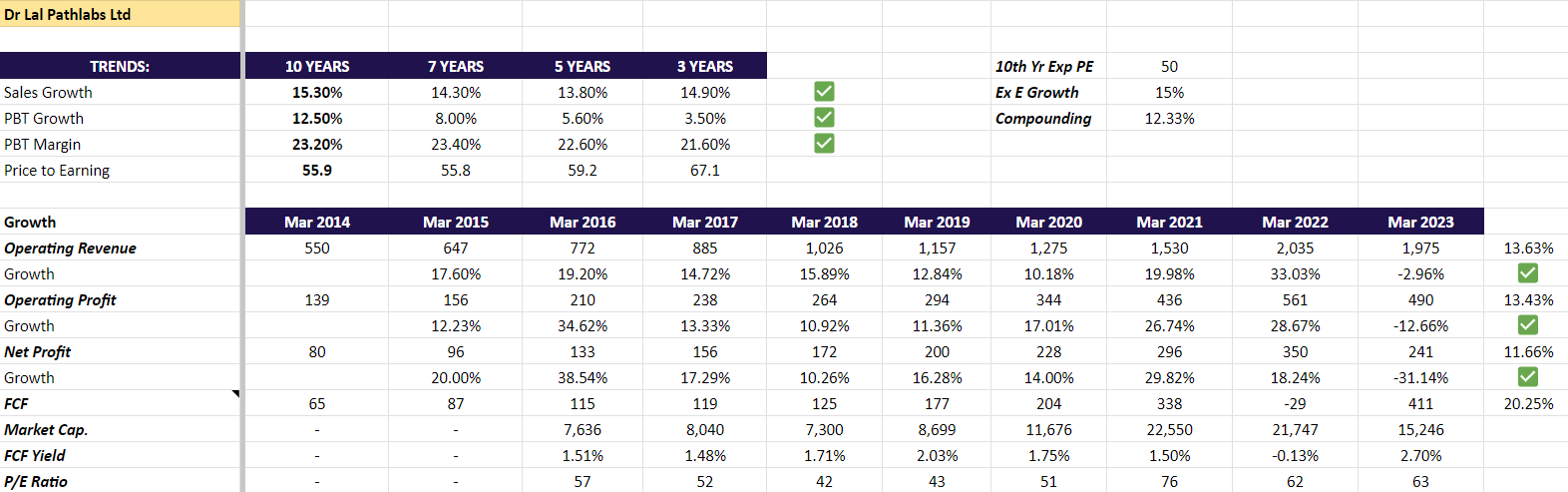

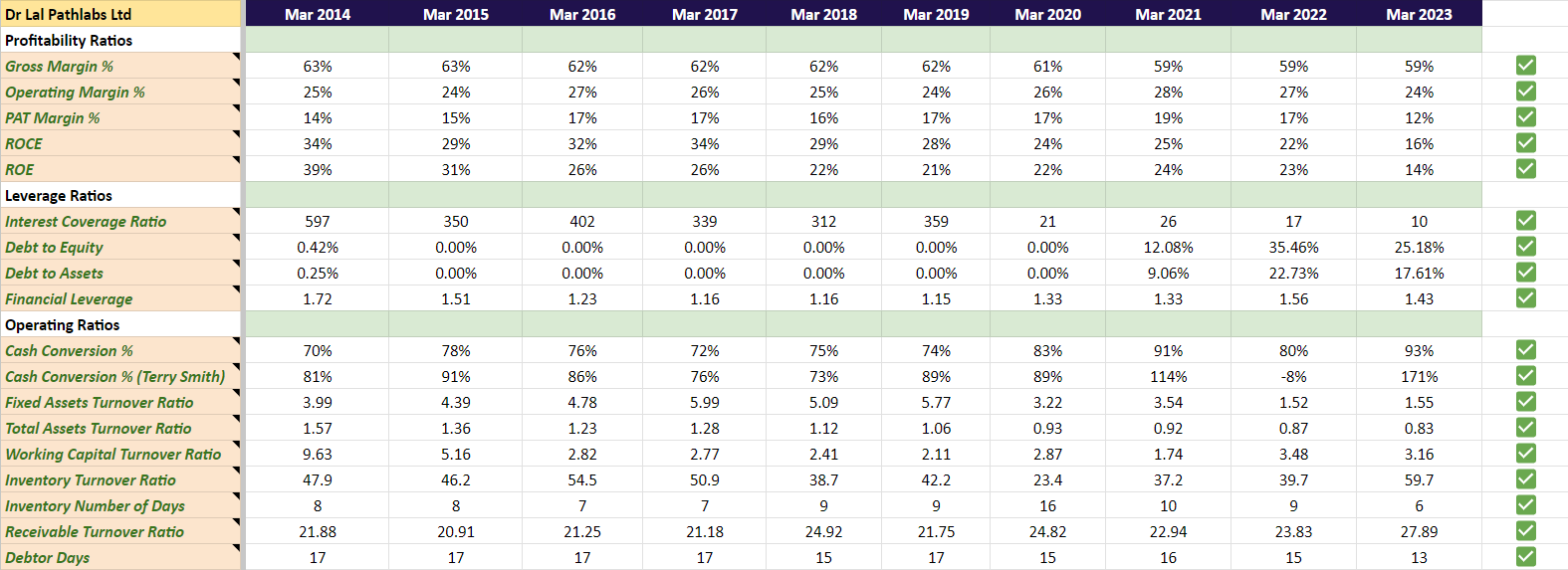

Quantitative Analysis

Ratios - Profitability, Leverage, Operations

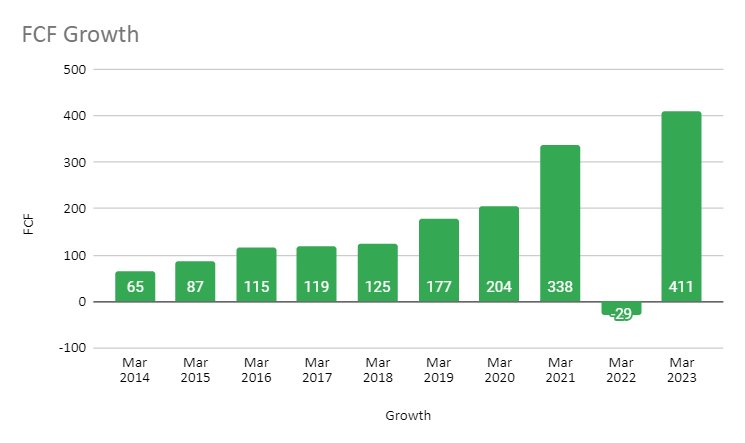

Free Cashflows

I can infer from the numbers above that -

- Dr. Lal has maintained high ROCEs consistently in the past 10 years (adjusting for COVID)

- It has also grown operating revenues consistently in the past 10 years (adjusting for COVID)

- Healthy and improving gross, operating and PAT margins - Profitability Check (adjusting for COVID)

- Leverage is not an issue - Leverage Check

- Healthy Fixed Asset + WC + Inventory + Receivable turnovers in the past 10 years - Ops Check

- Resulting in a growing stack of FCFs YOY - (adjusting for COVID)

Qualitative Analysis

Management Quality

- Does the management have a track record of good governance and clean accounting?

Yes. There have been no corporate governance issues in Dr. Lal in it’s history and has clean accounting.

- Do the owners of the company have connections to political parties?

No, they stay out of the limelight.

- Does the company have a strong track record of efficient capital allocation?

Yes, they have maintained high ROCEs in the past. A decent part of the net income has been invested back into the business for acquisitions and capex. Fingers crossed on the Suburban brand turnaround and scaling.

- Do the promoters have a track record of remaining focused on their core operations?

Yes. They have not invested in unrelated businesses.

Industry Attractiveness & Company Positioning

High historical long term ROIC - WACC spread in the industry. It allows dominant players to earn and keep a profit.

- Is the company’s business heavily dependent on government regulation?

Until now, the industry has been unregulated. Only 1% of the labs in India have NABL accredition. Majority of the labs do not even have qualified pathologists running operations. Any regulation in terms of QC or minimum standards will hit the fragmented 47% of the industry first, with the organized players already having the checks and QC is place. The ICMR has published a National Essential Diagnostics List (NEDL) which does not talk about price caps, but more about procedures and QC. There have been price caps for endemic seasonal diseases like dengue, malaria and COVID 19 in the past, but they do not erode margins significantly for the business in any time period.

- How many competitors are present in the industry and how strong is the competitive intensity?

The market is divided into the unorganized & standalone labs (47%) who mostly do high volume/low cost testing as a service. There is little value add for the customers here. The next segment is hospital based labs (37%) who cater to the patients who are admitted there. The last segment is the organized sector which is dominated by 4 players - Dr Lal, SRL, Metropolis and Thyrocare (which is now acquired by Pharmeasy). Dr Lal has dominated the north and east market (2%), while metropolis is strong in the south and west (1%). The sector is very price competitive (also because of PE/VC funded labs) and the only way to grow the topline is by volume growth. Price hikes have been rare in the diagnostics space.

- What is the overall size of the industry and its growth potential?

Diagnostics in India today offers a huge market opportunity at ~Rs. 70k-80k crores which is growing in double digits. This is led by faster growth in elder population, increase in evidence-based treatment, and increase in health awareness (especially post covid). Rising incomes which will lead to higher per capita spending on healthcare, increase in lifestyle diseases, and adoption of health insurance also help.

- Is the company in an industry where the proportion of value addition is high?

Yes, the diagnostics industry is essential for the treatment of patients and to assess the overall health (in case of wellness testing). It is the 1st step on the way to getting better if unwell, or preventing any health risks before hand. The value addition depends upon faster + accurate test results which are consistent & fairly priced. The continued demonstration of these attributes lead to an increase in trust with doctors who recommend patients use a particular lab for diagnosis.

- What is the capital intensity and capital efficiency of the industry?

The industry has high capital efficiency. Organized players use an asset-light model for organic expansion which generates high ROCEs and FCFs consistently for the 4 players. Cash on the B/S enables acquisition of fragmented labs where there is no prior geographical presence. This makes sense as it takes decades to build trust with customers and doctors in a geography. On the whole, the capital intensity of the industry is low, with the fixed assets turnover being 4 - 5x. Imaging and Radiology are capex intensive. (Dr. Lal has stayed away from them). However, the FA turnover deteriorates temporarily with acquisitions and setting up of reference labs (hub for the spokes). The spokes are all franchise driven.

- Is the industry’s business dependent on India’s broader economic cycle?

The diagnostics space is secular and does not depend on the India’s broader economic cycle. As people fall sick and need to be diagnosed to identify the disease or deficiencies, they will require diagnostics. It has nothing to do with economic cycles. There is a 10% revenue contribution from wellness diagnostics, which might be impacted during recessions, but in the long term it will go up due to a multitude of other factors (D2C marketing, lifestyle diseases, rise in disposible incomes).

- Does the business generate excess returns for shareholders?

Yes. ROCE is 2x COC for decades. This results in free cash flow growth and excess returns for shareholders.

Sir John Kay’s IBAS framework

- What is the company’s track record on innovation?

Dr. Lal has been implementing automation in sample testing with intelligence fed from in-house data analytics to enable faster & less variable TAT and further improving accuracy of results. For example, the firm’s ‘control tower’ initiative which enables monitoring of a sample lifecycle and identification/ correction of bottlenecks has allowed Dr. Lal to meet the ETR (Estimated Time for Report) more than 90% of the time vs. 80% earlier. Additionally, the scope for real time tracking of samples by hospitals has also been increased substantially allowing for better management of the doctor’s time, further building the stickiness of the firm with these doctors. Dr. Lal has also introduced high end speciality tests to India, where samples had to be sent abroad earlier.

- What is the company’s investment in brands and reputation?

Dr. Lal enjoys immense brand equity and has a very good reputation in North India (NCR region) from where it began it’s journey approx 75 years ago. It is trusted by doctors and the public alike, and has also acquired labs with good reputations in their localities. (Hence it is leveraging the Suburban brand to expand in MH). It takes a long gestation period to build trust in the medical fraternity, and Dr. Lal being the oldest has an advantage here.

- How strong is the company’s architecture?

In the B2C segment (60% of revenues), diagnostic charges are borne by the patient; so, the industry has evolved into a service industry competing on consumer convenience (rather than being focussed on the clinical or medical side). Dr. Lal has the largest network of franchise PUPs, PSCs and clinical labs for home collection and walk-ins. This enhanced reach results in customer acquisition and market share gains by solving for customer convenience. Digitization of the user journey from booking appointments for home collection, to providing online reports has enabled Dr. Lal to compete with other tech based diagnostics startups. In the B2B segment (40%) - 36% of revenues are derived from high end speciality testing from hospital and standalone clinical establishments. The hospital lab management has a 4% contribution (where Dr. Lal manages hospital labs).

- Does the company own any strategic assets?

Strategic Assets: Expansive network and reach, brand equity and reputation, economies of scale and operating leverage, digitization of operations and customer interface, and a legacy of 75+ years.

- Does the company have ROCEs that are higher than the industry average?

Yes, Dr. Lal has ROCEs 2x that of the industry, consistenly well above its COC.

Miscellaneous

Things to watch out for -

- Entry into tier 2/3 towns - Accretive contribution to the topline

- Suburban Acquistion Turnaround and Scale Up

- Replicating the success in the NCR region to other geographies (market share wise)

Lindy Effect - The Lindy effect (also known as Lindy’s Law) is a theorized phenomenon by which the future life expectancy of some non-perishable things, like a technology or an idea, is proportional to their current age.

Dr. Lal has a legacy of 75 years, and has started expanding seriously since 2005, with 20 years of solid performance with Dr. Om Manchanda at the helm.

I think there is tremendous longevity and robustness in the business with the potential to grow. They are at 2% market share (market leader) in a rapidly growing industry, with all the systems and processes in place, cash on the b/s for acquisitions, and a large, fragmented, unorganized segment of the industry to prey upon.

Also Read -

https://www.ambit.co/public/Ambit_Disruption_VOL19_DLPL%20(1).pdf

Disc - Bought in Jan 2022 at ~ Rs. 3000 at a PE of about 60x. Holding.