Hello everyone,

As clichéd as it may sound, I too have been a long time lurker in this community, which I have browsed in search of informed opinions with respect to my own stock picks, diverse investment philosophies, and approaches to investing in general. I would like to thank the many contributors to this forum which make it a goldmine of learning for newbie investors like myself. After dabbling in publicly listed equities for almost a decade, I think it’s time for me to share my own investment approach and receive feedback from the wider public.

Why do I invest in equities?

It is an asset class which is the least risky in the long term, because it enables real wealth creation through value addition to society and civilization. What helps additionally is that it also liquid, capital gains are conservatively taxed (till now), and there is no minimum ticket size required for me to participate. This makes it the best asset class for me in my unique life situation for wealth creation.

What is my investment philosophy?

I wish to be a permanent owner of a high quality business.

I believe that picking individual stocks and creating a portfolio is an exercise of stacking odds in your favour, so that a desirable outcome maybe achieved in due time (measured in decades).

Stock Screening Filters - (These filters ensure the long term survival and prosperity of minority shareholders is NOT in jeopardy)

- Clean Promoters and Management

- Avoiding Leverage

- Avoiding M&A Junkies

- Avoiding Turnaround Situations

- Avoiding unaligned owners (PSUs, Large Corporate Houses, MNCs with unlisted subsidiaries)

- Avoiding unpredictable, fast changing industries

The checklist has been borrowed from Pulak Prasad’s book. He has articulated the why’s far better than I can. But essentially, avoiding these risks reduces errors of commission at the expense of increasing errors of omission (which means we live to fight another day.)

Adding to pt 6. I also avoid all industries/sectors where the historical ROIC - WACC spread is insufficient. This indicates that industry dynamics are brutal, and do not allow even it’s dominant players to consistently earn a ROCE above the COC.

Therefore, I only stick to these sectors (where the long term ROIC - WACC spead is tilted in my favour) -

- Consumer Staples

- Consumer Discretionary

- Pharma, Healthcare, Diagnostics

- IT Services

Incidently, this idea is borrowed from Terry Smith. (All my ideas are borrowed from investors I admire.)

After I have filtered out the potential candidates for errors of commission (pt. 1 to 6), and candidates not belonging to the aforementioned sectors, I apply my next set of financial filters.

TRIGGER WARNING - I am an admirer of Saurabh Mukherjea and Marcellus Investment Managers (including their books and newsletters). Those who do not subscribe to his views will not agree with the following approach. So be it.

Financial Filters -

- ROCEs above 18% consistently for the past 10 - 15 years (with exceptions for COVID and other such calamities)

- Operating Revenue Growth of above 10% for the past 10 - 15 years

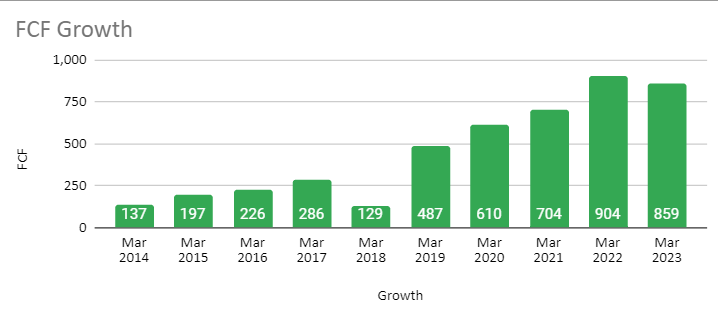

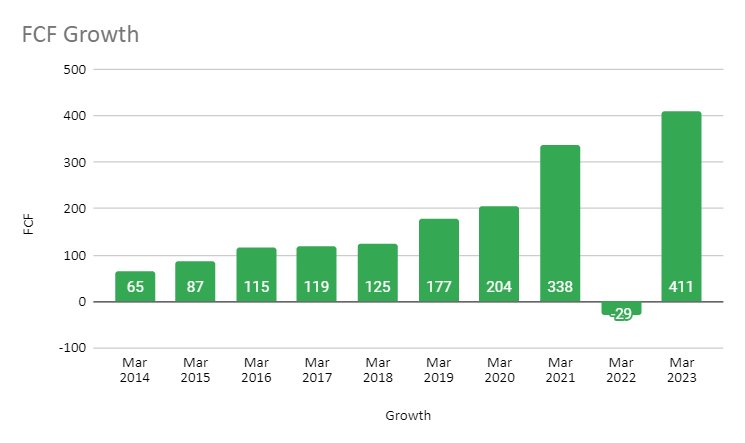

- FCF Growth - General Upward Trend

- Cash Reinvestment rates - (Increase in WC + Increase in CAPEX/CFO) between 50 - 80% - 3 or 5 year average annualized

After applying the following filters, I am left with very few businesses that would interest me. I now try to answer the whys?

- Why consistently high ROCEs?

- Why consistently high Revenue Growth?

- Profitablity, Leverage, Operating ratios - do they make sense wrt the industry and do they sync together?

- Risks to survival/existence 20 - 30 years from today

- Porters 5 forces model, Cost Leadership vs Product Differentiation, Big Fish in the value chain, Niches, Sir John Kay’s IBAS framework.

The next pertinent question that I ask myself is with respect to valuations - What is a price that I am willing to pay for them?

I anchor my price to the median TTM P/E of the market index, and do not pay for any multiple above that price. I will also look at the median TTM P/Es of the sectoral indexes to fine-tune this anchor. I might occasionally overspend a little bit for a franchise that I truly appreciate. But that is it when it comes to valuations.

I do not indulge in forecasting (DCF valuations) or any other excel wizardry for valuating a business.

Selling - I never sell a business until the business has obviously lost the plot (like DHFL or Vodafone India) or if the inital investing hypothesis does not hold true anymore (management makes a large unrelated acquisition, leverage, etc.).

I hope that I have been able to illustrate my investment philosophy adequately. I invite everyone to poke holes in it, or ask for further clarity on any of the topics.

I think there’s been more than enough gyaan in this next post. In the next post, I will try to argue the case for a particular stock that I own in my portfolio and do so for each stock in the weeks to come.

Happy Investing, and all the best.