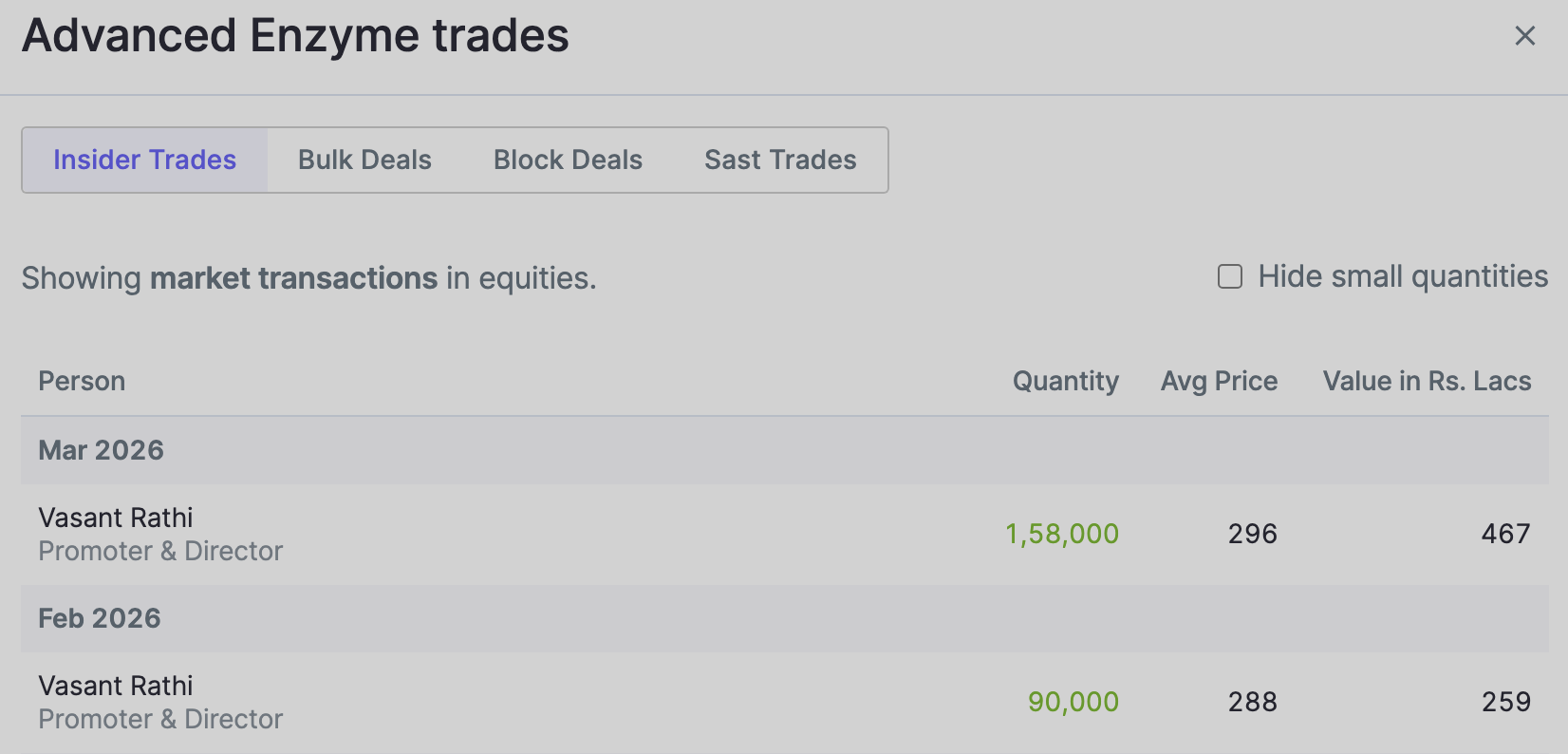

Just an update on the recent promoter buying.

Recently took a 2% allocation after seeing this.

Will track it closely after the coming quarterly results.

Sharing my thoughts on Advanced Enzymes, would love to get feedback. Feel free to point out inaccuracies, or help me improve my understanding.

Starting with optionality…

1. EU sales could increase with the new approvals and eVoxx starts to support sales of products, in addition to continuing R&D.

2. Acquisition a strong possibility, done in past, acquisition of JC Biotech, SciTech, eVoxx.

3. Growth in US business a possibility, but will take some time (“Mr. President is busy”).

4. Bio-Catalysis for API mfg, under trial with a few customers, is a focus area.

5. Working on a few products/solutions already. New R&D center will help develop more products.

6. Probiotics, working on new products, market is highly competitive, but is also big.

7. Wellfa, B2C business, lots of trials and errors may happen, B2C can be a difficult business, have a dedicated team which is a good sign, shows focus, but challenging.

8. Novel Food Ingredient in EU (Serratiopeptidase)…time consuming and very difficult approval process, but once approved, will grow well in couple of years post approval.

Now some numbers…

EV = 3150 (mcap) + 20 (borrowings) - 600 (cash+investments) = 2570 Cr

CFO = 140Cr

EV/CFO = 2570/140 = 18.3 (for a business which converts 70% of Operating profits to CFO but is not growing, this number is not cheap, but acceptable. If going forward there is growth, then current valuation starts to look cheap).

EBIDTA = 200 Cr.

EV/EBIDTA = 2570/200 = ~ 13 (Its cheap for a 30% margin business, which is debt free, has superb balance sheet with cash which is conserved for acquisition, and does not need lots of cash for regular capex).

Net profit for FY’26 could be between 145 to 155 Cr.

EV/Earnings = 16.5 to 17.7

So the business is reasonably priced, but if there is no growth, then can be a value trap. Having said that, there are multiple levers of growth. Management has hinted at possibility of surprises, so I am inclined to believe some positive developments will happen, will look for some concrete developments in the upcoming quarters.

Disc: Invested, biased

They have been saying it for some time now. A lot of R&D - not sure for what? last 5y sales 7%, last 5y PAT 0%

Sr. VP and Marketing head resigned this month.

I agree nothing new seems to be coming out of R&D, but at the same time their approval process is also long. For example EU is pretty strict with approving. The Novel Food Dossier that they have submitted, that is taking very long time, and one doesn’t even know if the approval will come through. If you look at the total EU contribution, its pretty low at 6%, and that has not improved in the last 5 yrs. But this year hopefully it will do better.

Also if we see their segments other than Human Nutrition, all are showing slight upward trend, indicating slowly but surely things are improving.

Regarding the resignation of the SVP, people leave, hopefully that shouldnt impact the company.