COMPANY OVERVIEW

Advanced Enzyme is an India enzyme manufacturing company led by Chandrakant Laxminarayan Rathi. The technical definition of an enzyme is “a substance produced by a living organism that acts as a catalyst to bring about a specific biochemical reaction”. Enzyme manufacturing companies cater to a wide variety of industries such as human health care and nutrition, animal nutrition, baking, fruit and vegetable processing, paper and pulp processing, biofuels, biomass processing and biocatalysis, etc.,

Global enzyme market is growing in single digits. The market segmentation for various areas of application shows that 34% of market is for food and animal feed folowed by detergent and cleaners (29%). Pulp and paper share 11% while 17% of the market is accounted for textile, leather and fur industries. Source: http://nopr.niscair.res.in/bitstream/123456789/17451/1/JSIR%2072(5)%20271-286.pdf

The biotech industry in India accounts for just 2% of global biotech markets and is set to grow at a faster rate when compared to the global growth rate. Even though there is a prevailing domestic demand, the segemt is largely export oriented.

Global enzymes market share is consolidated in nature with Novozymes, Danisco, and DSM dominating the overall industry demand. Novozymes is the largest manufacturing company and offers various products for household care, food & beverages, bioenergy, agriculture & feed, and technical & pharmaceuticals applications. The company puts in massive efforts to retain its market share by continuous innovation and R&D. Other industry players include Royal DSM N.V, BASF, Chr. Hansen, Enmex, Roche, Lonza Group, and Adisseo. Source: Enzymes Market Size and share | Industry Statistics - 2024

Technology disruption - With many global companies investing on R&D there might be unforeseen risks arising from technology disruption/innovation

VALUATION

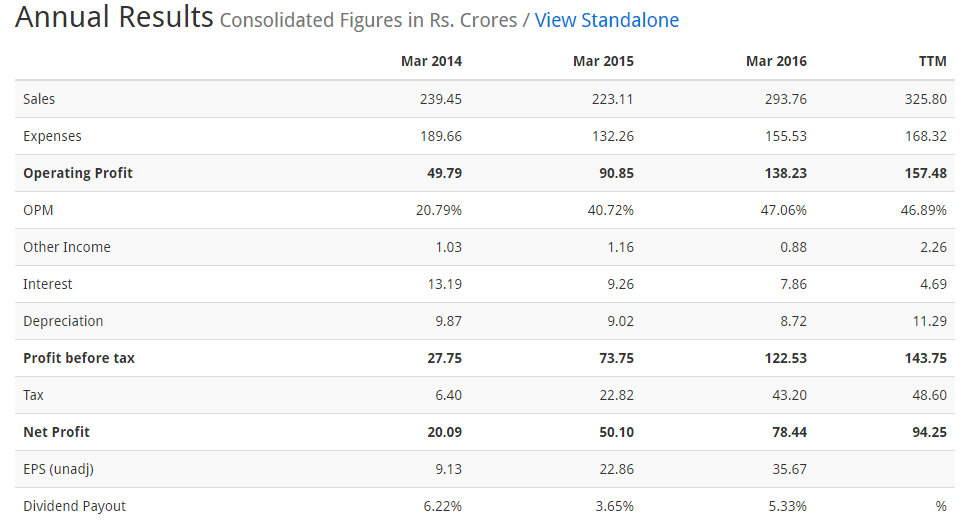

The current market cap of Rs 3500 crores values the company at ~38 times TTM. As per the management commentary the company is expected to grow at 25% bottomline for many years to come. Global leader Novozymes trades at 28 times earnings and 70 billion market cap.

DISCLOSURES

I have bought shares in the last one month.

I had got allotment in IPO and exited at around 1400 because of rich valuations. It continued to rise and at these levels, the growth of next two years is priced in. So nothing much is left on table as of now IMHO. But of-course, Mr Market has its own ways of valuing such high margin, niche players. So I could be completely wrong.

Hi, What is the entry barrier to this business? Are the products co-developed with the end user? How easy is it to switch from one supplier to the other? Why was there a sudden jump in OPM in FY15?

Specialized business has high entry barrier. The enzyme industry is very concentrated and consists of very few players. Factors such as technical and specialized nature of the business, heavy reliance on research and development and dearth of qualified professionals with experience in enzyme and biotechnology industry operates as an entry barrier to new players in the market.

The company has a diversified product portfolio and wide customer base. AETL has a de-risked business model with Top 10 customers accounting for 41.48% of the total revenues on consolidated basis for the fiscal year ended March 31, 2016. AETL offer more than 400 proprietary enzyme products developed from 60 enzymes to their global clientele of more than 700 customers spanning presence across 50 countries worldwide.

The core competency of AETL’s business is its R&D Capabilities which it has developed over almost three decades of operation. The company spends around 6% of total turnover every year in R&D activities.

Regarding co-development and customer switching

AETL is an integrated company with presence across the enzyme value chain, covering the entire range of activities from research & development, commercial-scale manufacturing, to marketing of enzyme products and customized enzyme solutions which enables AETL to be cost effective and competitive.

The company has not entered into any long-term or definitive agreements with its customers. Any failure to meet customers’ expectations and if customers choose not to source their requirements then business, financial condition and results of operations may be adversely affected.

Specialised products will be patented and that is the entry barrier. What proportion of sales is this specialised products? Is it reasonable to say the balance is a commoditised business?

How much pricing headroom is there in the existing contracts with customers?

Any idea if FY14 OPM was depressed or something dramatically changed in FY15?

They have not provided the breakdown of patented vs non patented. They have been working on this for decades and not many people have been doing this for as long as they have been. That in itself gives them the niche. In one of the interviews the management talks about prices been going down in general with increasing areas of application which is making up for it. In FY14 they did a voluntary product recall which led to the profits going down. From what I gather they are operating on a fixed base and any incremental increase in orders will result in higher margins.

Sir you had a specific program, which started in Q4 of last year on a new enzyme and supply. If you recall the numbers were hitting about 80 Crores to 90 Crores per quarter, we still could not understand the extent of drop which you have seen this quarter in the revenue line that is one question? Second question even the gross margins have contracted, if you could give some more knowledge or light on the current quarter performance and second how do you see this panning out over the next one year?

CL Rathi: Thank you so much. Actually it is only that one customer who overbought and that is why the numbers would got skewed because they suddenly bought because as you know we are a biotech company where we have very high margin business and our other expenses are more or less very static like same number quarter-to-quarter. Now when you have a low number sale, then you will see all number changing and when you have too much higher sale, again you see too much variation there. Otherwise when look at from year-to-year perspective what we have been communicating right from the day 1 to all the investors that listen, this is a very steady business, very, very sticky business. Our customers are very, very sticky, but because of B2B customer sometimes they do make error in their own projection.

My guess is that USFDA and regulators can come into the picture either directly or indirectly in the Human Nutrition segment, other industrial enzymes may not come under their purview.

I think something that is ignored is that Enzymes are like 2% of the product cost for the end customer. That usually is a good thing (see AIA Engineering) because the cost of failure is too high to take a risk but in this case I feel like it will be the reason they cannot deliver on their growth. Advanced Enzymes may be much cheaper than Novozyme, but Novozyme being the run away leader may compete much much more on quality than on price because of the nature of the industry.

So, while this is no doubt a high quality company, I am wary of paying such a steep price for it (it has gotten more expensive after the Q3 results too!) as I can see scenarios where the growth doesn’t play out.

I am invested in this company since 1435 level. Since the valuations are rich, I have only invested 25% in it right now and plan to pick more at every 10-15% fall. However I think the company should do well for the next 3-5 years at least.

Below videos might help understand the company further.

Disclosure - Holding only tracking position right now.

CL Rathi talks about promoter buying happening over the last few days

We are the leader in this industry and we see huge future for us in nutrition growth along with animal nutrition and we also have a lot of niche market in palm oil extraction and various biocatalysts

We are also a normal investor like anybody else. We will work within guidelines, we do not want to breach anything in the process and at the same time we think it is a good opportunity

AEL has sent intimation on face value change from 10 to 2…How this is going to create value for investors? Will this improve liquidity in the market and lower price tag psycologically attract people? Requesting views.

In my opinion this split will not add any value in the long term. Company needs to deliver results for stock price to move up

Stock is already priced at 40X plus FY17 earnings. Last qtr was a aberration as per the company. If this quarter or some of the next quarters in near future also have such negative surprises, stock might lose its premium valuation (split or no split)

This will be classic example for the scenario mentioned in the Book" Value Investing and Behavior Finance". New Tech companies come up with IPOs in the Bull period and they get hefty valuations. People jump in a frenzy to grab the pie but get disappointed. Here investor needs to see other factors as well.

If the company is not able to keep the growth momentum then the stock will see more lows.

Hi @nityanandparab,

I find that they have technological moat in making Enzymes, the only one in India and no. 2 in the World… Don’t you see that this is an investment opportunity/ opportunity to accumulate? They command high multiples because of their specialization I guess.