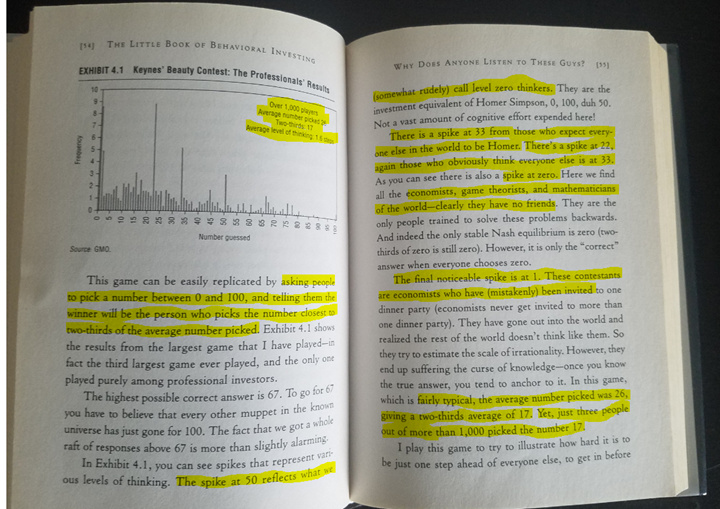

There are two things in this post - Somwhat mathematical, somewhat probabilistic and behavioral, maybe even philosophical (they are all inter-related anyway). Some things I have have been ruminating over the last few hours. The payoff from this could be useful in current markets - Or so I think.

It started with this puzzle I received in a whatsapp group.

“There is a long line of people waiting outside a theatre to buy tickets. The theatre owner comes out and announces that the first person to have a birthday same as someone standing anywhere before him in the line gets a free ticket. Where will you stand to maximize your chance?”

This is a very simple-sounding puzzle where the brain naturally thinks that standing further back in the queue increases our chances of a sure win (More birthdays to choose from, for your position) - For eg. if you stood at 366th position, you have all 365 unique days to choose from - Surefire win - But at what cost? As you go further back, hoping for the high probability of a sure win, you also give others a chance to have a go - For eg. A person at 365th position has 364/365 birthdays to choose from and a very, very high chance of winning. So you must optimise and find an appropriate position. Where will that position be? What’s the number that your brain intuitively comes up with? Mine said somewhere in the middle - Say around 180 should be good for me. Am neither too greedy, nor too fearful at 180. Right?

So I set myself down to solving the puzzle and optimising for both variables and what I found was completely non-intuitive (Unless my solution is wrong, in which case, please PM me).

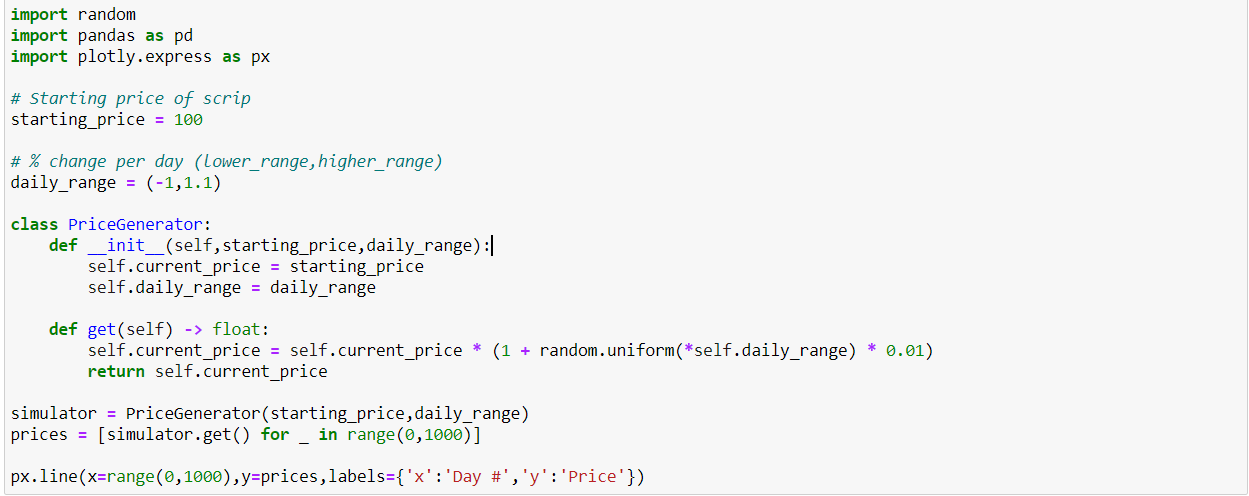

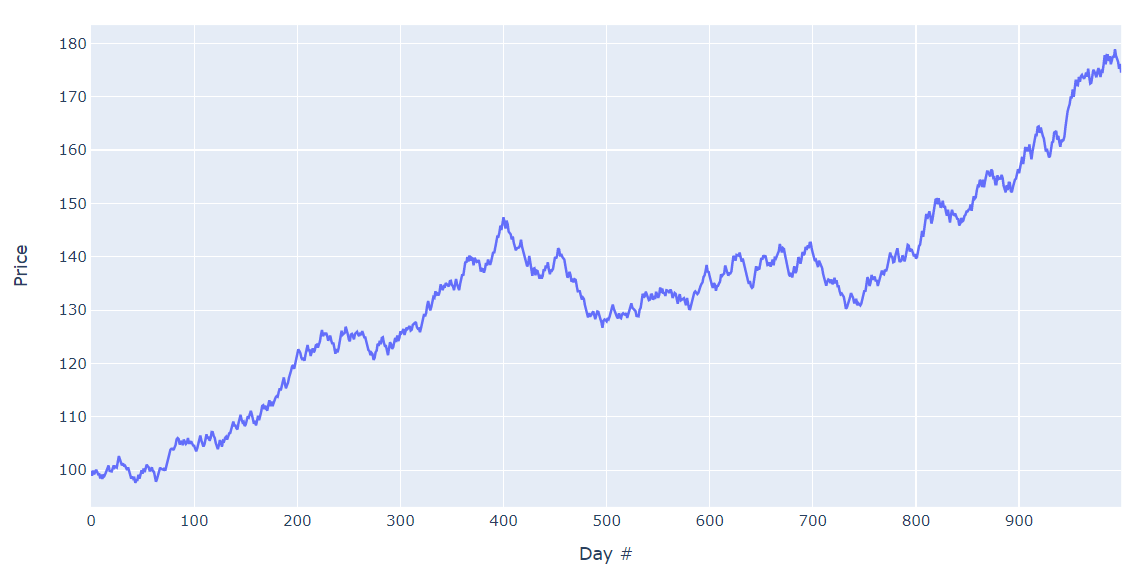

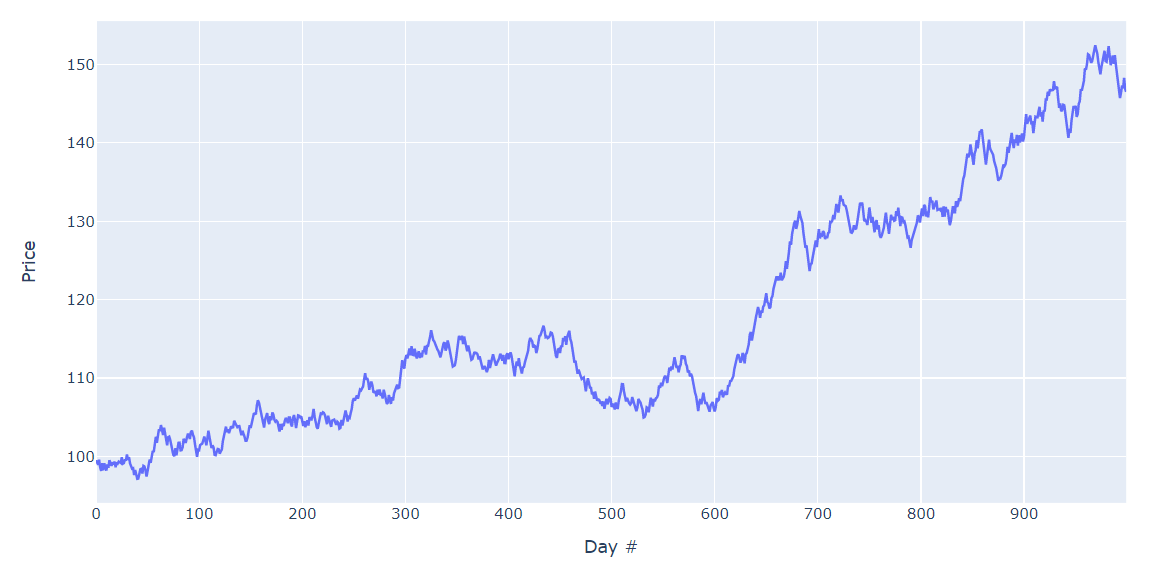

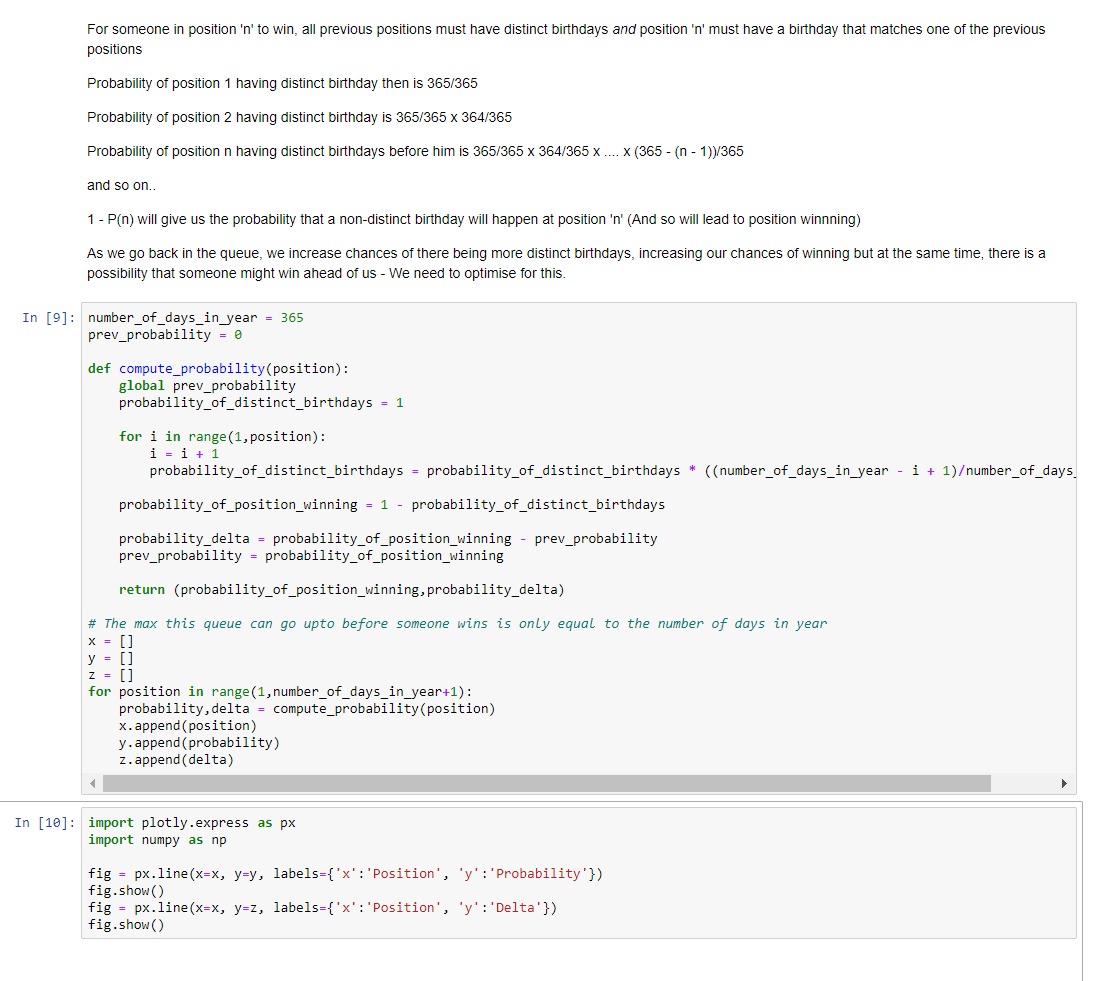

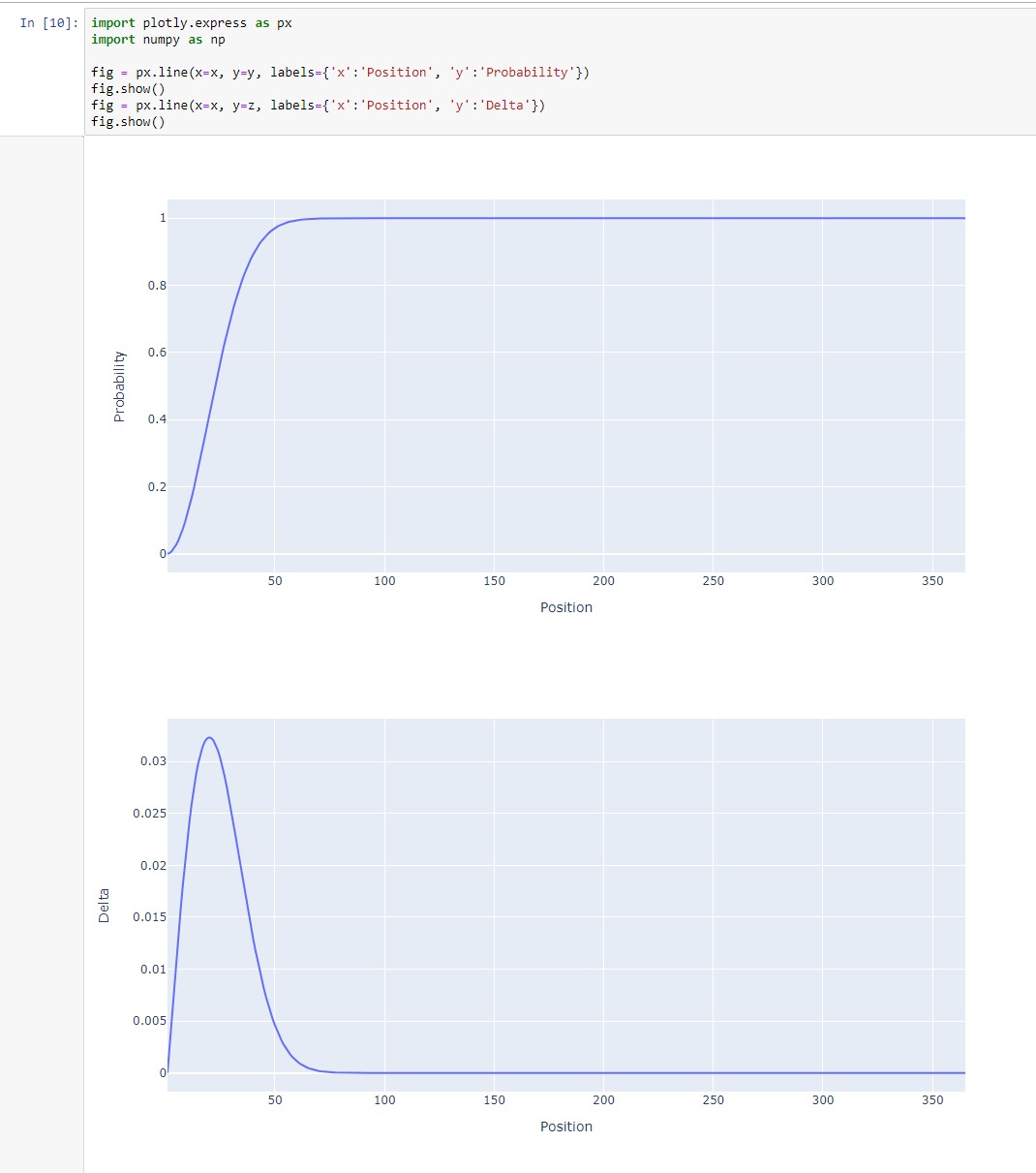

These are screenshots from my iPython notebook.

The answer to the puzzle is 20. Yes, you must stand in position 20, if you are not too greedy or fearful as your brain claims yourself to be. This is where the probability is 0.5 for winning. This is also the position where the incremental increase in probability in moving back in the queue, maximizes out. This is completely un-intuitive to our brain as standing in position 20 sounds like a losing proposition.

So what happens if you stood at position 20 and you lost? There is still 50% chance of losing here. Handle it with equanimity, as you merely played the odds the way it should be played. What happens if you win? Hand over the credits to lady luck and take credits for computing the odds.

Standing anywhere after about position 50 to position 365, makes hardly any difference, probablistically speaking. Between 20-50 is the juice is.

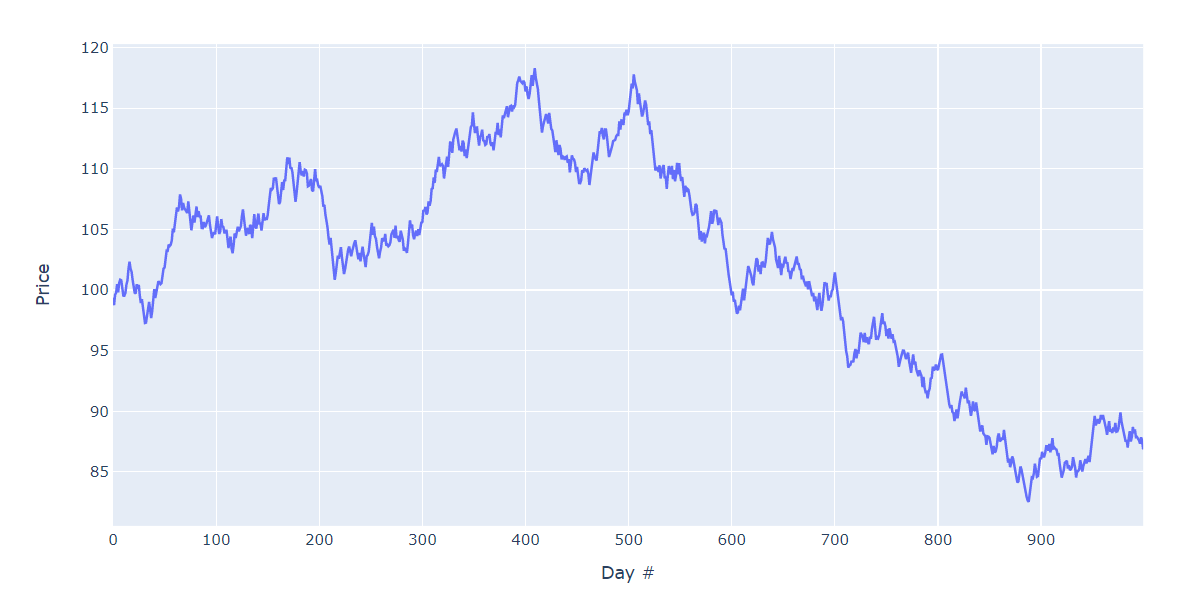

This is just like waiting for a market bottom, where you wait for great deals, giving reasonable deals a pass - reasonable deals which should at least probably be nibbled upon, while prepping yourself up for the great deals, if they do come - Again, let me be very clear that this would be overfitting a bivariate distribution to a multi-variate problem with a lot of uncertainties. But the concept is fairly similar and the takeaway should only be that our brain’s intuitive position in something like this, probably should not be trusted. Our brain is good at optimizing for one variable and it is very good at loss aversion and it is very good at holding onto a decision - all of these, most times in a combination can be harmful, despite our best efforts.

So how do you decide?

I have been using Kelly Criterion reasonably successfully for asset allocation based on risk:reward. Under uncertainty though, computing risk:reward is a fools errand. This is where I came across Minimax Regret from a post on Epsilon Theory earlier this week. The idea is fairly simple - You choose the course of action where you minimize your maximum regret. If you think that the course of the market running away from you is going to cause you maximum regret, you avoid that course - by buying a bit. If you think that market making bigger bottoms is going to be your maximum regret, you minimize it by not going all in - The point is, you don’t take either path if you think both will lead to maximum regret. This doesnt take into account external probabilities but works solely based on you and so will have different courses for different horses. Ruminate on that.