और कृषि उपकरण (Farm Equipment) पर चर्चा | Ace Tractors | Green TV")

1 Like

1 Like

Interesting Summary in this report, i do not have access to this report, pretty premium price ![]() If anyone has access and can summarize the impact to ACE, that will be helpful.

If anyone has access and can summarize the impact to ACE, that will be helpful.

India Crane Market - Strategic Assessment & Forecast 2021-2027 (reportlinker.com)

This kind of market survey based research reports on construction sector are very common and they have their own business purposes. Personally I don’t provide much importance since the summary of all are quite same. I receive a lot of them everyday,sharing few for better understanding.

2 Likes

This has logged its All Time High today and closed on a high too prior to the result next week. Something big is definitely happening in this sector and company. Expecting some acquisition announcement too from the company in Concall. Let’s see how it pans out.

1 Like

Please share the source of your comment,otherwise this will be treated as speculative personal assumption without any evidence,without adding any value to this thread. This forum doesn’t work this way I guess.

2 Likes

1 Like

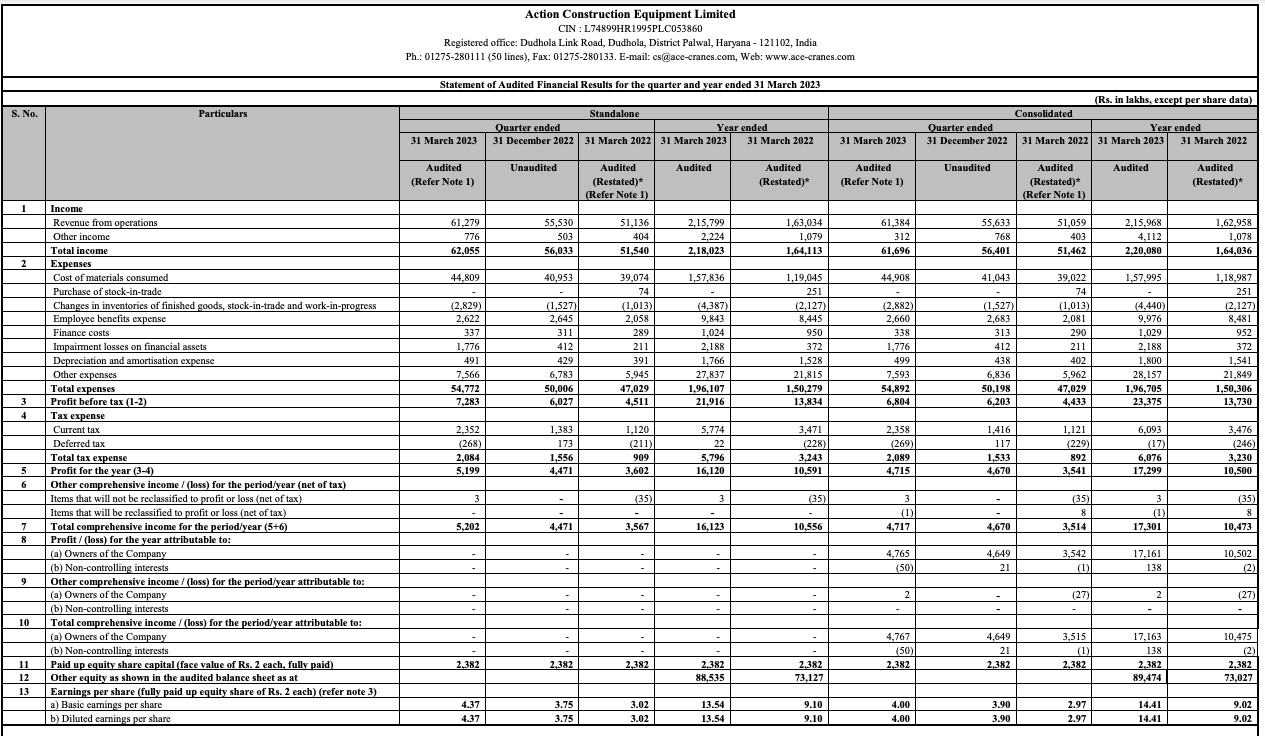

Decent Q3 Result…

ACE - Action Construction Equipment Unveils India’s First Electric Mobile

Crane & Expands Product Range with New Launches at Bauma Conexpo 2023

1 Like

1 Like

Great numbers

Capex Theme

#CraneCompany

ACE

consistently delivering at these valuations too.

Capex theme

#CraneCompany

Proxy to the Capex that’s happening across agri, logistics, warehousing, ports, Airports, railways, Housing, road and Manufacturing

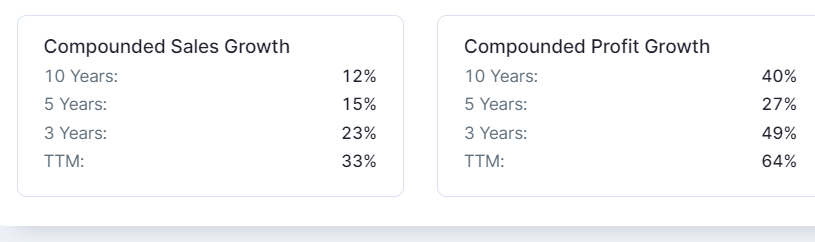

50% EBITDA growth

33% PAT growth

Total income 2x in 3Y time

PAT did 3x + in 3Y time

4 Likes

Very bullish commentary from management on the con-call. My notes below:

-

Contribution of export segment which is at about 6% currently is expected to grow to 9-10% in current year and 15-20% in the medium term.

-

Expecting15-20% growth in Crains, material handling and agri during FY 2024.

-

Expecting 30-35% growth in construction equipment’s segment - should hit a revenue of 300-350 Crore during current year and grow to 500 Crore the year after!

-

Margins to improve due to operating leverage and product mix change.

-

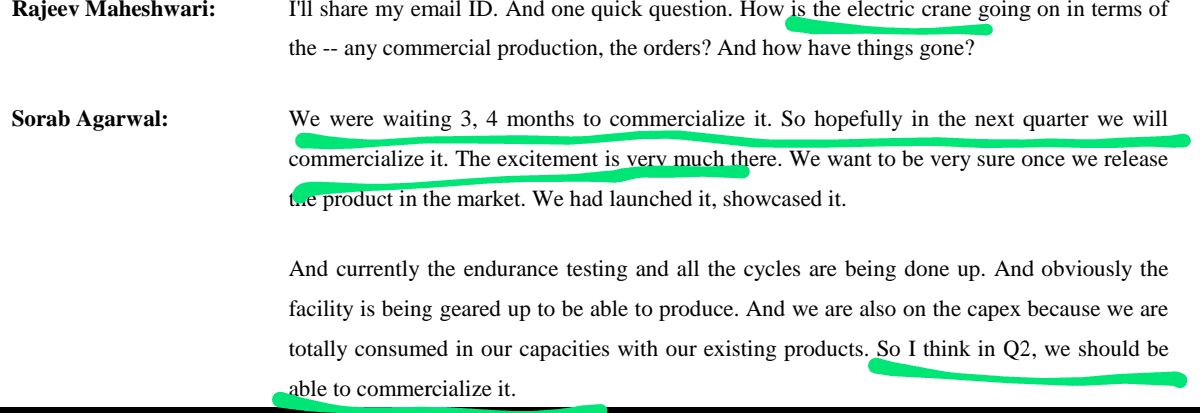

Electric Crains will be commercialised in Q2.

-

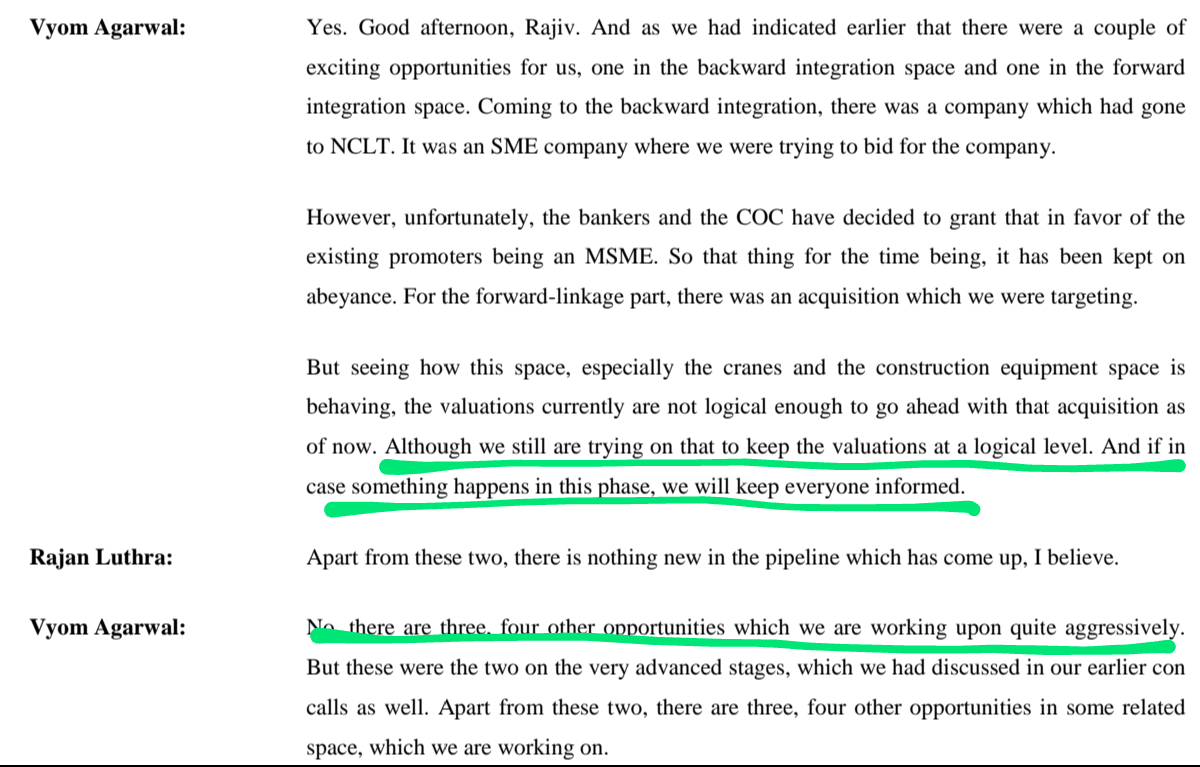

Looking out for acquisitions provided they come at the right price. Expect an announcement within the next 2 quarters.

-

Revenue Mix - Construction equipment share which is currently at 11% may go up to 14% in about 2 years.

-

Investment in Ghana: Discussions with Ghana government continuing. Will start work only one advance payment is received. Issues are expected to get resolved by Q2.

-

Agri equipment annual revenue to hit 300-350 Crore by FY 2025. This is when the operating leverage is expected playout leading to margin improvement from this segment.

-

ESOP program is rolled out to employees. Need to understand this better and see how much dilution in equity is expected.

-

Management is committed to double the revenue in 3 years.

Link to concall here.

Thanks,

AJ

Disclaimer: Been holding some shares from 2019, added after listening to commentary. Views are biased.

6 Likes

Thanks @AJ41. So far management seems to have been walking the talk. I am expecting to see them gain more market share in Cranes and CE. Agri has been a laggard for them. However, keeping an eye on the constructions activities going on around the country, company has high hopes (so do I) on them going strength to strength in next few years.

Holding since few years and adding at regular intervals.

Views: biased.

2 Likes

Earnings Call highlights

• Revenue guidance: Total 15-20% growth for FY24 with a possible upward revision in coming quarters. Crane, material handling and agri equipment segment growth is expected at 15-20% while construction equipment segment growth is expected at 30-35%

• EBITDA margins for FY24 are expected to be up 100-150 bps YoY considering the company’s focus on cost efficiencies, higher operating leverage and better product mix

• Demand has been healthy in the cranes and construction equipment segments led by higher capex allocation for roads, railways and urban infra

• Capacity utilisation has reached peak levels in the cranes and construction equipment segments

• The company is growing better than the industry in cranes and construction equipment as its volume growth was at ~24% YoY and ~38% YoY in cranes and construction equipment segments, respectively

• Volumes in agriculture equipment segment declined in FY23 as the industry is migrating from BS-III norms to BS-IV norms. There was an inventory level of only three to five weeks in agriculture equipment. However, volumes are expected to improve in FY24 led by better crop prices and expected normal monsoon

• Exports revenue share was at 6.7% of sales in FY23 and is expected to increase to 9-10% in FY24. The medium term target of the company in exports is to reach 15-20% of sales

• Capex for new capacity for manufacturing large cranes is | 80-90 crore. The capacity is expected to commence production from Q2FY24

• Potential turnover post commissioning of new capacity is | 3800-4000 crore

• Though there was a rise in imports of larger cranes from China, the company is setting up new capacity as demand has been robust

• The company’s focus is on increasing its market share in larger cranes like crawler & truck cranes. Moreover, the focus remains on maintaining its leadership position in pick & carry cranes

• Material handling equipment segment is growing at 10-15% but is expected to increase in the coming period led by industrial capex

• Regarding inorganic growth, the acquisitions that the company was looking for, have been kept on hold due to valuation concerns. However, there are three to four more opportunities, which the company is exploring

• The defence segment is contributing 2.5-3% to total sales at present. The company is aiming to increase this share to 8-10% in the coming period

6 Likes

Action Construction Equipment is included in the MSCI Global Smallcap Index. It was added to the index on May 31, 2023, as part of the quarterly rebalance. May be reason of recent rally in this stock.

4 Likes

4 Likes

Please see financial result below for last 2 years:

| FY 2021 | FY 2022 | FY 2023 | |

|---|---|---|---|

| Sales (Cr) | 1,227 | 1,630 | 2,160 |

| Sales Growth over PY | 33% | 33% | |

| Net Profit (Cr) | 80 | 105 | 173 |

| Net Profit Growth over PY | 31% | 65% | |

| ROCE | 21% | 22% | 29% |

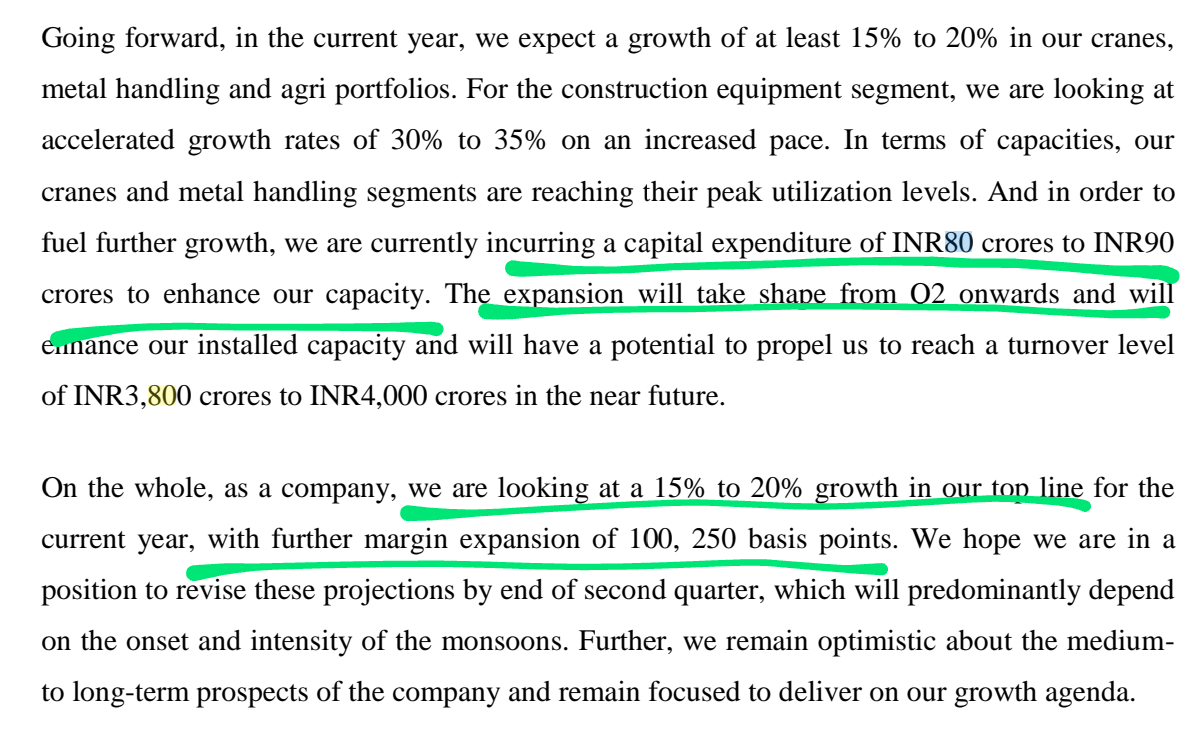

The company has been growing sales and profit at a very healthy rate since last 2 years. Even recent quarterly results are continuing to show good growth. In June 2023 concal, management sounded very confident of further growth along with margin improvement. Quoting below directly from concal transcript:

“On the whole, as a company, we are looking at a 15% to 20% growth in our top line for the

current year, with further margin expansion of 100, 250 basis points.”

Disc: Invested ~5% of portfolio from ~300 levels

5 Likes

Last quarter concall data points. Looks like some acquisition news is coming. Reason of this recent rally.

New product launch :

Acquisition :

Capex :

3 Likes

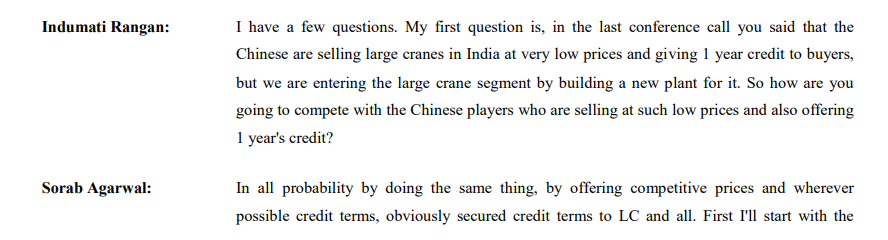

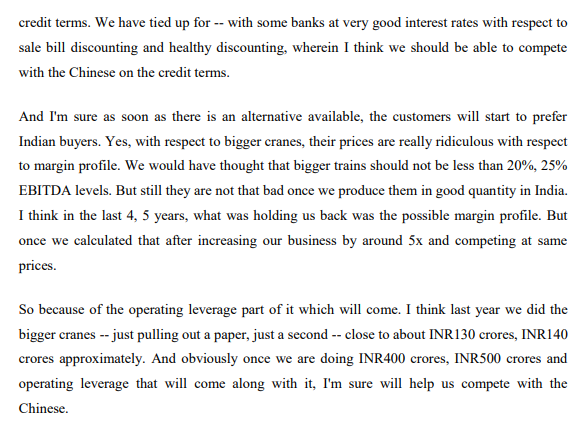

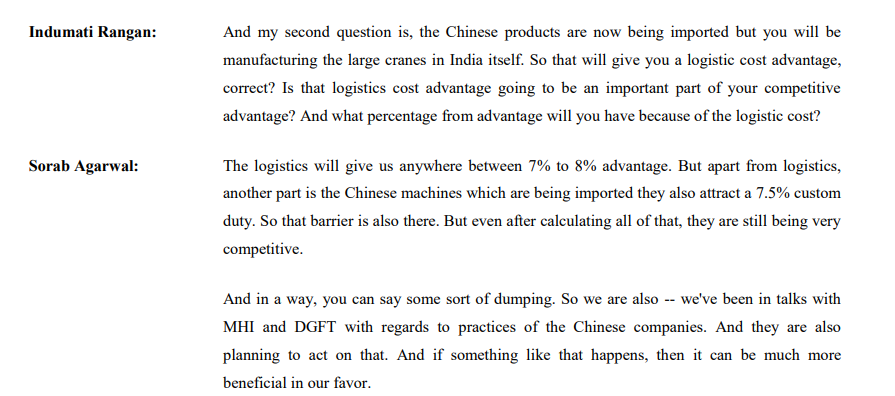

All I can say is very intense competition from Chines players and current valuation levels are skeptical about any fresh entry. Some thoughts to share from a recent con-call -

2 Likes

The above concall discussion is with regard to Large Cranes where company is not having much of presence /dominance.

1 Like

ACE