Can this change from a dividend play to a growth play?

This company is looking interesting with the change in ownership from Accelay Holdings Co. to Warburg Pincus. So far this was a delight for typical dividend hungry investor with tempting dividends. Munch this: Hefty regular dividends between 2012 - 16 with minimum limit being ~80%.  .

.

Genesis of dividend was Accelya holding used these generous dividends to fund their sundry ventures. They milked the cow to the most, so much so that company dig into its reserves and paid 700% dividend in YE June ’13 ( 70/- per share against earnings of 59 per share). Additional dividend out of general reserves & resulted in 138% payout ratio. This also resulted in reserves coming down to 87 Crs. as of June ’13 from 122.61 Crs. in previous year.

Retail Investors off course will love the windfall bounty. However, to me these dividends possibly had an opportunity cost attached - Opportunity to explore and expend in the growing travel IT business. They have garnered the place for themselves however limited to one niche of the entire spectrum of services needed by travel industry. Possibility of expending further on the growing travel IT business was somewhat plausible possibility given their deep penetration and relations over the period.

Width of Industry Horizon:

- overall addressable market of travel technology only at approximately 76 billion euros in 2016. Market sources expected to grow at close to 4%

- Trave lis one of the world’s largest industries, representing almost 10% of global GDP. It is also a growing industry, with Euromonitor predicting 4% growth per year to 2019.

- IATA reported 3.8bn air passengers for 2016.

- Relationship between GDP growth and air traffic passenger growth is not linear rather log normal-ish. Which means, exponential growth in air traffic beyond a certain GDP growth rate. Some estimates suggested air traffice grown at a multiple of between 1.3 and 1.6 times real GDP growth over a long period.

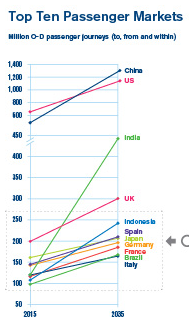

- Top 10 passenger markets from now to 2035. Dont miss to notice the steep green line representing India :

Opportunity:

Aviation Revenue Accounting Outsourcing Market Analysis by KPMG is an excellent source to understand the opportunity:

airline-industry-revenue-accounting-outsourcing.pdf (609.5 KB)

Some excerpt:

The market for revenue accounting outsourcing solutions continues to grow positively. The International Air Transport Association (IATA) counts 240 airlines as members, about 84 percent of total air traffic. Approximately 25 percent of their members are low-cost airlines. Currently, there are around 50 carriers with outsourced revenue systems, leaving 200 to 250 as potential targets for outsourcing. It is estimated that annually, 10–15 carriers outsource all or part of their revenue accounting systems. With well over 50 percent of the market working on a legacy platform, there is a large opportunity for outsourcing among large carriers particularly in North American and Asia Pacific regions with specific segment opportunity in Europe, especially among emerging carriers.

Triggers:

Basis my reading there are 3 specific triggers basis which outsourcing has became a necessity rather than an option:

- Industry consolidation

- Market Alliance/ Aviation networks

- Low cost carriers

Competition:

Page 3 of the NIIT whitepaper on Revenue Accounting is listing a high level industry mapping. Whitepaper - T&T - New Age Asset - Airline Passenger Revenue Accounting.pdf (2.4 MB). Basis my reading on this subject, travel IT company Amadeus is an upcoming challenger on the Aviation Revenue Accounting Outsourcing.

For context, Amadeus is a giant in air travel agency distribution business with a pole position of over 40%. Have reach to 350 airlines + 90 LCC. Recently acquired Navitaire’s New Skie platform to further strengthen offerings for Low cost carriers. Will be serving over 1 billion passengers by 2018 through Altéa, and well over 1.6 billion including Navitaire’s New Skies.

In terms of firepower to fight any long battles, Amadeus got top line revenue of 113,519 Mil Euro as against 2,490 Mil Euro by Kale for FY’17 - stark 45 times bigger. Couple of years back Amadeus has launched its own Revenue Accounting System to compete with Revera (flagship product of Accelya). They already have signed Saudi Airlines, British Airways, South African Airways and Vistara.

Scope for Accelya:

- Most important consideration from an investors perspective, change in strategical focus - cash cow to growth engine.

- Rational of merging Mercator and Accelya together is to chalk out a new growth trajectory for the combined entity.

- Cross selling opportunity across 400 clients and possibility to cover multiple touch points across value chain basis synergistic business.

Reference and resources:

20160908_AIT_Revenue-Accounting_HD.pdf (801.9 KB)

-airline-industry-revenue-accounting-outsourcing.pdf (609.5 KB)

PRA System Revenue Accounting.pdf (124.2 KB)

Disclosure:

Not invested as of now. Though not sole criterion, yet If DCF is anything to go by, approx 25% growth for next 6 years is fully priced-in.

This counter looks interesting so I may be interested whenever market obliges.

Thanks,

Tarun