Warburg Pincus Backs Combination of Accelya and Mercator, Creating a Leading Global Solutions Provider to the Travel IndustryPress Release of combination.pdf (2.0 MB)

Open offer as well soon.

Warburg Pincus Backs Combination of Accelya and Mercator, Creating a Leading Global Solutions Provider to the Travel IndustryPress Release of combination.pdf (2.0 MB)

Open offer as well soon.

Accelya Kale reported its result today. Overall flat bottomline vs. Dec’15 quarter (standalone), while around 15% growth for consolidated figures.

Discl: Invested

Found this note from their Open offer

The Offer Price is INR 1,250 (Rupees one thousand two hundred and fifty), which is higher than (i)the fair value per equity share of INR 1,195 (Rupees one thousand one hundred ninety-five only) as setout in Bansi Mehta & Co.’s valuation report dated 2 February 2017, which has been computed in terms of the principles laid down by the Supreme Court of India in the case of Hindustan Lever Employees’ Union vs. Hindustan Lever Limited and others, and (ii) the equity value per share of INR 1,234 (Rupees

one thousand two hundred and thirty-four only) as set out in MZSK & Associates’ valuation report dated 2 February 2017.

Currently trading at 1500+ , Seems Overvalued

These valuation reports needs to be taken with pinch of salt. Has it accounted for future cashflows which can come from Mercator? Have they accounted for any synergies due to merger?

Vivek, I was tracking this from last 6 months but could not research on revenue model if it is footfall driven or fixed license cost. Want to understand if aviation industry makes losses, does it impact them.is there any correlation to revenue with footfall n crude price movement based client profitability situation ?

No, it doesn’t impact. The model is selling IP for small amount and then offering maintenance on per transaction basis (I think if you scroll above I have given these things in detail).

can anyone explain what are the impact of Mercator Combined with Accelya?

Prashant

They will have more synergy. Almost monopoly in airline IP based business. Also, incremental outsourcing from Mercator in long term will create incremental business for Accelya Kale. Also, now the group will have better pricing power due to merger.

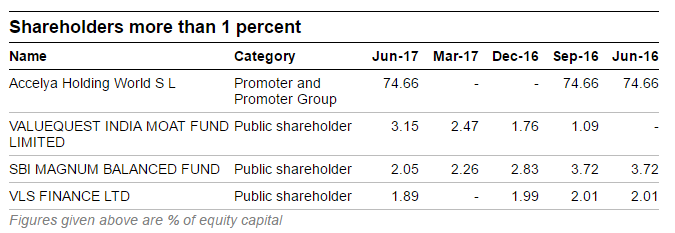

Value Quest fund increased their stake in Accelya during last quarter. This is as per latest SHP released by company today.

Disc : invested

Value Quest holding in Accelya

Sept 2016 - 1,62,429 shares 1.09%

Dec 2016 - 2,62,429 shares 1.76%

Mar 2017 - 3,68,774 shares 2.47%

Jun 2017 - 4,70,163 shares 3.15%

i searched for SHP information in bseindia site and accelya kale site. I am able to see the shareholding pattern data of Valuequest Holding till March 2017 in Accelya Kale site. can you please help me how can i get the SHP data for June 2017 of Value Quest holding in Accelya

Found this on ValueResearch

In this thread it was mentioned that all the debt is taken by the holding company and majority of the profits of subsidiaries are distributed back to the holding company (essentially capital allocation decisions are taken by holding company). Can anyone share recent data about the debt figures of the holding company? Thanks in advance.

Apart from the analytics trigger, is there any other trigger like adding a new airline that could improve the topline? Since everyone is bullish on the Indian Aviation Industry recently, how much potential does Accelya have to grow in this space say in the next 3 years?

Accelya declared Q4 results along with a final dividend of INR 40. For the full year, consol EBITDA grown by 11%, net profit by 10% over last year.

Disc- invested

Accelya Kale`s and Mercator offerings are fully integrated now and will be operated under Accelya brand, this is a huge positive according to me

There are only 3 major players globally catering to revenue accounting and financial solutions, Accelya - Rivera, Mercator - Rapid and lufthansa platform, now with mercator fully merging with accelya rivera`s platform, this becomes a global duopoly with wide moats.

Stock should start reflecting this fact soon

Also Rs 45 dividend is due, few days away from record date

Some useful numbers on the overall market for Airline Passenger Revenue Accounting

From the paper it seems that Mercator and Accelya together occupy about 18% market share.

33% of passengers seem to be served by internally developed revenue accounting systems so it seems like a good outsourcing opportunity available on that front.

Also consolidation happening in this industry. Amadeus acquired Navitaire from Accenture.

Great information.

Additionally, i believe Airlines inter operator clearing system (Under IATA or some alike named body), uses Accelya product. Some 300+ Airlines are member of this body and hence indirect user. Benefit may not be direct but still it will help in brand value and competitive edge.

According to the report, Accelya and Mercator together will have passenger base of ~60cr making them the market leader and is 50% more passengers than lufthansa.

As you have pointed out, there is ample outsourcing opportunity and the scale and synergies due to combination and a strong pe like warburg pincus and support by the likes of sanjay bakshi (~3.5% holding) further validates the case

ROCE of 100%, Div yield of ~4% and weakening rupee are added positives