Good to read the rationale…

But seems par for the course. Every good company goes through such hiccups from time to time. If truly a moated and high management pedigree company then these reasons should not matter. In fact may be a great time to further accumulate.

hi…Have you got any news about 4th quarter results? hows the overall full year results? I am asking from the point of view of Mankind Phrama generic version of Dufasten…Is Abbott India recovering from that shock? and going forward, do you think it can overcome the attack from these two sides : 1) Generic version attack …2) National list attack

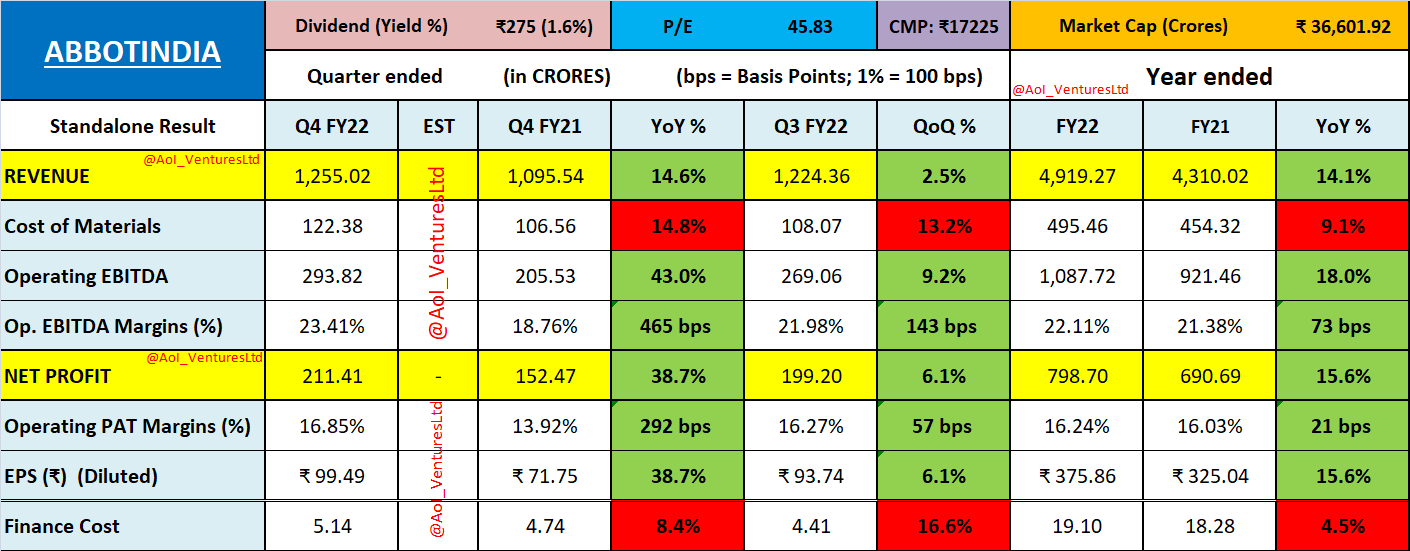

Yet to see company filing it’s Mar quarter results. Normally company announces a bit late on the earnings season.

I think replication of a generic medicine by a local player is quite an expected risk. It can happen with other medications also other than Duphaston and over time if profit pool is high it’s the obvious outcome.

Not bothered on a long term basis as company’s strategy is to continuously bring newer products from it’s parent’s portfolio.

National list is a concern and need to watch out how it affects and to what extent.

Generic substitution is an obvious risk, I agree with you…But does that risk has potential to disturb long term growth of the company as well as stock performance? kindly elaborate. Also I find that its least communicative company.There are hardly any concalls. I asked questions through emails to Investor desk, but no response at all. Also the generic substitution has come in 2019 I think…but after that too stock performance was good even till sept of 2021…Stock performance deteriorated and stock was down by almost 30 % from its peak in last 4-5 months…What must be the reason for it? and also Marcellus exited this stock. Kindly share ur opinion on it?..Thanks

Well I have found MNC companies to have very less frequency of communication - Abbott India, Honeywell Automation and to some extent Nestle India. So I will have to agree with you on that.

Mankind’s Duphaston has been cited by Marcellus for their exit from Abbott India, but in my view I do not think it has a long term negative impact.

I mean in any capitalist system, a moat attack is the most natural expectation for a dominant company. If our investment thesis of Abbott India being a high ROCE, moated business is valid then it’s only a matter of time that it regains it’s market share.

For something as critical as infertility treatment, the brand value and goodwill will have some traction with end customers compared to say a generic paracetamol medicine.

Also Abbott has multiple blockbuster OTC medicines and will create more such brands in future by borrowing from its US parent’s portfolio.

However as there are so many moving parts of a business, difficult to predict anything with certainty beyond a few quarters.

I think the business is more impacted due to high raw material inflation. No idea on pricing fluctuations.

In my opinion, the impact on business was more due to postponement of deliveries and IVF, IUI where critical applications were there and due to covid, ppl have postponed their decisions about such voluntary as well as non-urgent treatments…Hopefully this is the reason i am expecting to be true.

The company has never degrown its topline and bottom line for the past 12 years. So is the case with last 14 quarters. But the only cause of concern is it has been growing its topline at an average 12% for past many years. Therefore, whether the company is worth the PE of 52 is the question i am trying to look answer at. May be its getting some sort of MNC premium.

In my view this stock unless does really well based on some growth triggers, will be stuck at this levels for years or may fall going forward on account of PE de-rating. At an average PE of 35, it will quote 13K. But then market always has some surprises

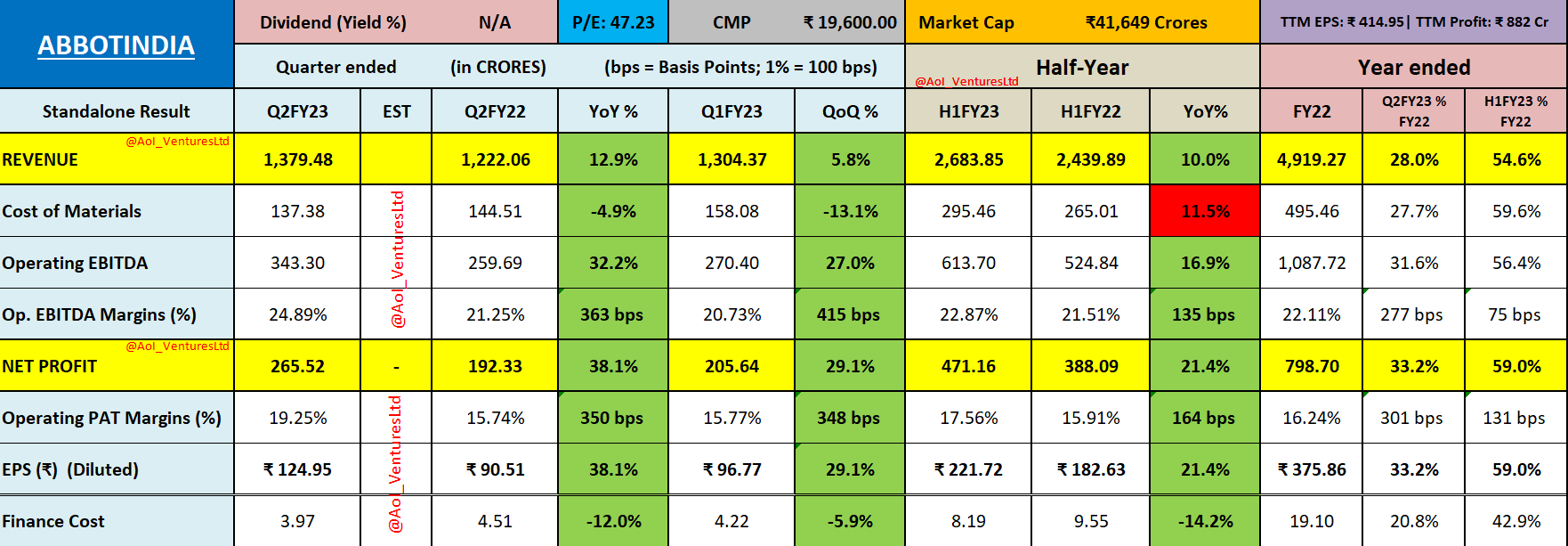

Finally, a real conference call (Link) from Abbott India (28-Sep-2022):

Notes (fine-tuned as per my understanding):

Branded generic space industry is a $20 billionàindustry growing at around 10% to 12% à3000 odd organizations. Only, 20% value with the multinationals and the rest with Indian companies. However, 43%, 44% of the market share is held by the top 10 companies. Abbott India Limited is the only multinational amongst the top 10 companies in the Indian pharmaceutical market. Abbott India is also growing faster than the Indian Pharma Market, IPM.

Approach to becoming category leaders: Category expansion, testing, different SKUs for product gaps.

Duphastone: Lost share but we have grown and continue to grow. Moved from being the only one to one amongst the 41 brands in a span of two years after being the only ones for 60 years. Broadly two segments to the entire Duphaston market- gynaecologists and IVF. Lost share in gynaecology, but not in IVF.

Growth strategy:

Lifecycle management, expansion of current big brands - top 10 brands are categories and investing further to expand the categories

Scale up the number two set of brands- the next 10

New Product Launch: Plan to launch 75 products In the next five years compared to 35 Products launched in the last 3 years. Where is that delta coming from? Not as much in lifecycle management, but on LOEs (loss of exclusivity) and other therapy areas. Out of the 75, at least 50% are going to be LOE.

Nurture a new category under women health (postmenopausal): Investing heavily to build the post-menopausal problem category with Femoston, a very big and very strong molecule globally. Expect post-menopausal problem category to become huge in the next 3~5 yrs.

Ramp up headcount in GI: Abbott is the leader in the gastrointestinal category and would like to retain this leadership.

~70% of our business comes from metros and class one towns. Spreading the business to class two, class three, and extra urban geographies.

Ensure product availability across channels.

Miscellaneous:

33% → In-house manufacturing

58% → total raw materials was imported

FY22 top line growth → 14.1%: 7.6% volume and the rest price.

Almost 26% of our business by value comes from NLEM products

60-odd brands in the portfolio. Top 10 brands → 70% of the business. Next,10 brands → 20% of the business, and the rest contribute the remaining.