FY21 AR Observations (adding delta, focusing on qualitative aspects):

MD’s Message: Nine of our top 10 brands lead their individual markets; Launched a team to specifically focus on coverage in the Tier 2 markets; Increase our efforts towards vertically integrating our portfolio; Making constant improvements in formulations and packaging to enhance patient adherence

Operating strategy (paraphrased):

- Retain our market leadership while delivering best-in-class products to our customers, strong returns for our shareholders, and generating consistent value for all our stakeholders.

- Nudge the patients (HEALTH CLINICS CONDUCTED-9800+; ~58 Lakh PATIENTS REACHED THROUGH MAKING INDIA THYROID AWARE INITIATIVE; ~30 Lakh PATIENTS ENGAGED THROUGH D STROG), Coach the healthcare professionals (~20,300 MEDICAL STAFF TRAINED AS A PART OF KNOWLEDGE DISSEMINATION WORKSHOPS)

OPERATIONAL EFFICIENCIES AT THE PLANT:

TABLETS MANUFACTURING

• 50% increase in coating installed capacity in 2 shifts from 675 mio tabs to 1,012 mio tabs. Increase in installed capacity will help site to produce all Brufen SKU’s in-house as well as scope for internalization of new coated product

• 75% reduction (from 16 hours to 4 hours) in coating solution preparation time with user friendly method

• 20% reduction in machine hours (from 12 hours to 8 hours) and 11% reduction in labor hours (from 36 hours to 32 hours)

• Standard Yield improved from 98% in 2020 to 98.3% in 2021 resulting in cost saving

LIQUID MANUFACTURING

• Enhancement in liquid installed capacity from 9,745 KL to 12,700 KL (30%) without any capex

• Reduction in conversion cost in liquid by 10% (Actual 2019 v/s 2020) resulting in reduction of cost per unit

• Over 54% volume growth in liquid which is the highest ever since inception of plant (44.4 million bottles)

Opportunity Size: India’s domestic Pharmaceuticals Market (IPM) is estimated at INR 153,534 Crore in 2021 with growth of 4.4% v/s 2020. Acute therapies dominate IPM with 64% of total sales, however the chronic segment shows faster growth. There are estimated to be over 8,000 pharmaceutical companies, however the market is dominated by a core of around 300 manufacturers whose products generate the majority of sales in most therapy areas. Domestic manufacturers claim around three-quarters of the market in value terms

Risk: Increase in the list of drugs covered by the National List of Essential Medicines (NLEM), restrictions on trade margin mark-ups and amendments in pricing regulations will create price pressure on the industry.

I could not think anymore that can impact this business severely. You are welcome to add more.

My opinion:

-

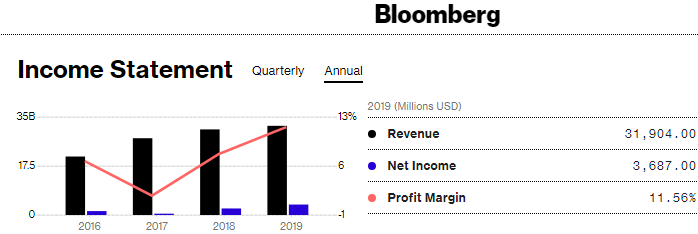

P&L statement shows ~16% growth in PAT w.r.t FY20, but it’s practically ‘same as FY20’, reversing the impact of increase in inventory under ‘Changes in inventories of finished goods, stock-in-trade and work-in-progress’ and decrease in Other Expenses (decent COVID time savings under the heads - Advertising, publicity and sales promotion and Travelling and business meetings. However, ‘Professional fees and other services’ flared up for reasons unknown to me…?). However, I consider this as one off considering the challenges COVID posed for the economy.

-

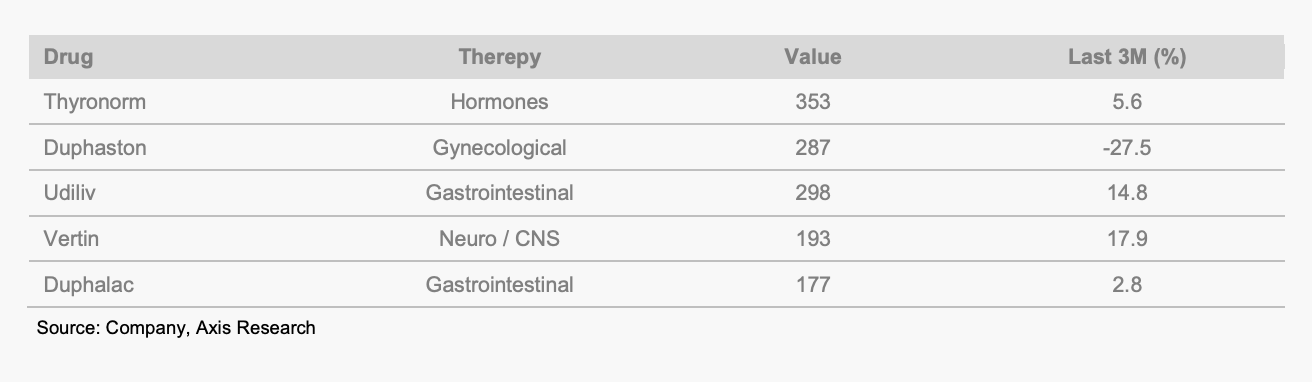

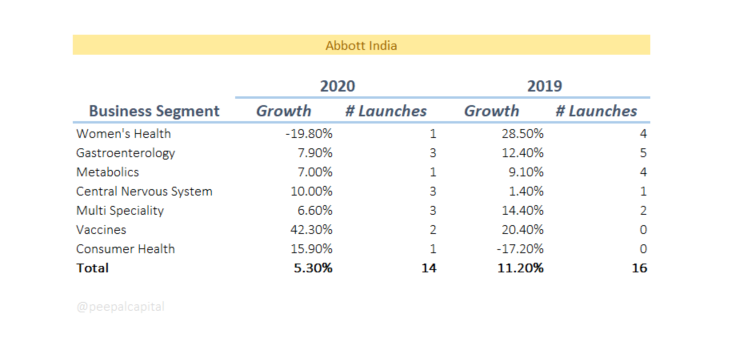

Business Characteristics: Sells branded products, which command trust among the health care professional, across multiple chronic therapies with almost NIL R&D. Well financed – No Debt, 68% B/S as Cash and equivalent, Asset Light (single digit % of Total Assets in PPE), Negligible Capex on YoY basis which makes it a Free Cash Flow Machine.

Overall: It’s a structural and domestic oriented multi-year growth story considering India’s demographics and portfolio of the products, which are necessary and need repeat buy. Due to the same and a limited supply of free float, valuations are rich even though shareholder’s communication is minimal.

Disclosure: Invested and expecting to beat FD returns at least. Please do not use the above as an investment advice due to below reasons: * I might be wrong in my understanding of the business, if history really rhymes.*** You may not know if I change my mind.**** Resources around you will help to build the conviction, which is a must have for anyone investing in equity directly.

Your thoughts are welcome. Also, do suggest any other domestic and listed competitor that I must study for better understanding.

If someone can throw some light ?

If someone can throw some light ?