Hi everyone!

After recently joining the forum, and soaking info from all sides - I rebalanced my portfolio and would like your insights on it. As a young 22 beaming with passion for deep diving into equity research & technical patterns, my psych rubs on my portfolio with small cap/ midcap dominance and once in a while I dabble in large caps like TVS Motors if the charts get me excited enough ( getting rarer lately ).

I pick shares using a bottom up approach, first ensuring strong fundamentals with revenue growth visibility & margin expansion with capex/expansion plans. Then I time my entry based on technical aspects such as VCP breakout with volumes/ Stage analysis/ EMA 200 support levels. I try to avoid very high PE shares, and below 30-40 levels is my sweet spot which helps me sleep better at night.

Since most of them are small/ mid caps, I prefer to take a small loss and exit before it snowballs into larger ones, and let the winners ride. If the same share forms a better base later on, I re enter. This approach has its own merits and flaws, but seems to have worked for me after a lot of trial and error.

I’d be happy to try other approaches with merit, so feel free to add.

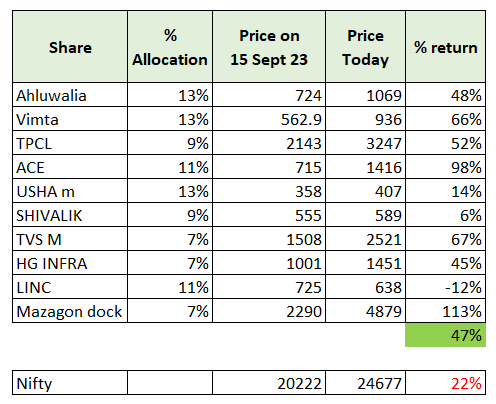

Portfolio : Currently having positions in 10 companies - with a medium-long term outlook. I am trailing most of them with EMA 50 stoploss, and will be actively tracking AGM notes and Quarterly results to see if the mgmt walks the talk, and scale up on further conviction.

Ahluwalia - 13%

Vimta - 13%

TCPL - 9%

ACE - 11%

Usha Martin - 13%

Shivalik Bimetals - 9%

TVS Motors - 7%

HG INFRA - 7%

LINC - 11%

Mazagaon Dock - 7%

Rationale for picks:

-

Ahluwalia and HG Infra both had 20%+ revenue guidance with healthy order books, and neutral margin outlook. I am a bit divided in this position, since I read that Infra segment usually faces a slowdown before elections, hence closely watching for exit if support breaks. I genuinely believe this sector is poised for good times, with growing infra & urbanization developments in India.

-

ACE is a proxy to the Infra play. Mgmt seemed very excited about demand outlook despite Monsoon season, with very strong commitments on margin expansion and topline doubling in 3 years. Seemed like a no brainer, eager to see capex and volume variables for this quarter.

-

Vimta - This is an early May position and honestly I wasn’t very sure about it but the share was at a well tested support with decent fundamentals. Little did I know it would grow itself to become the largest position in my portfolio. Q1 had bullish mgmt comments with plans to double capacity, and 2% margins expansion with revenue target of 500 cr for 2026 ( currently 315 cr ), which further rocketed the share to ATH - trailing this one as I am not sure if there’s much fuel left.

-

TVS Motors and Shivalik Bimetals are auto sector plays. TVS might be the only large cap I own right now, it gave a solid base breakout, and fundamentals seemed on right track with 2 wheeler demand rising with rural recovery and expanding margin guidance. It was a tracking position initially, which for scaled up recently when the share seemed to be taking support above 20 EMA.

Shivalik - smart meters - high capex - auto sector tailwinds - EMA 200 - connect the dots. -

LINC was a Pentonic play purely, with recent breakout from downward trend - will need to track this more actively every quarter to see if mgmt plans execute well.

-

Usha Martin - I liked the part about increasing margins from premium products and 15-18% revenue growth, the price chart was like a ant climbing a mountain - always like such treks with EMA 20 support.

-

TCPL Packaging - was very unsure about it since mgmt had pessimistic tones on fmcg volume growth, but the charts very giving a fresh breakout. Held onto a trailing position and voila! I still fail to get my head around how it went to where it is today.

-

Mazagon Dock - Latest entry at cup and handle breakout after a long upmove previously. I missed the initial rally in shipbuilding sector despite tracking it for 1 year. Call it a revenge trade haha but it seems to be playing out well - will trail it as long as it keeps me in trade. Mgmt seems positive about fresh orders potential - will need to track how it plays out though.

That’s all folks! I know it isn’t perfect - and I am just a beginner. I recently exited Mayur Uniquoters as it took out my stop loss, and there are many more mistakes that I did. However, keeping a tracking entry initially helped me to limit my losses and ensure my winners more than cover for the losses.

I am not very hopeful with current valuations, but earnings growth is there - so keeping a trailing stoploss to see where it leads. Feel free to add your own insights/ suggestions on any positions you are interested in - would be happy to learn from your experiences!

Thank you!