Thank you for sharing the details. I tried to find the link to apply buyback online but unable to find so. Can you please share the link for Buyback?

It should be there in your broker portal, depending upon which broker you are using.

I got it.Thank you very much

Q1FY25 Concall Summary

Business Updates

- The decline in revenues is due to lower realizations and subdued API demand in export markets

- The greenfield project for intermediates and specialty chemicals at Gujarat will start from Q2 onwards

- The company incurred capex of Rs 52 crores during the quarter and total capex for full year will be Rs 200 crores funded through term loan and internal accruals

Participants

Dolat Capital

Axis Securities

Unifi Investment Management

Yogya Capital

DSP Small Cap

QnA

- The domestic volume was not impacted but in exports volumes got impacted negatively by 8% yoy and mainly the antibiotic category got impacted

- The export demand still seems slower and this should pickup from Q3 onwards and as far as FY25 is concerned H1 will see a negative rate variance while in H2 this variance will go away due to the lower base of last year and thus growth will be visible with new products from dermatology also coming in

- Specialty chemicals will see business doing well from H2 onwards and for full year can see a good growth of 50% in H2 on a yoy basis

- Since the export order book is more than 2.5 months there was an impact of price decline while in India the order book is around a month so price variance impact was not seen

- In many export markets the business happens on government tenders and there are many regime changes happening in global governments which could also lead to an impact on export volumes

- In the next 3-4 years the target is to achieve revenue run rate upwards of Rs 4000 crores with an annual EBITDA margins of 14-15%

- In terms of formulations working on 15 products across cardiology and oncology and these will be launched over the next 2-3 years

- Majority of the sales from oncology formulations will start from FY27 onwards

- When the API prices are lower the gross contribution margin should be higher and that is a function of lower prices and company has a target to achieve 35% gross contribution margins

- There are many challenges in the export business on availability of container and also cost of freight so export momentum should be lower in Q2 as well

- One reason why impact on margins is lower is lower contribution from exports which has come down from around 38% to 31% and generally the gross contribution margin in exports is higher

1 Like

Aarti Drugs had announced a temporary shutdown of a specific product line following a bromine gas leak incident at its manufacturing facility. The leak occurred during the transfer of bromine from a tanker to a storage tank.

As a precautionary measure, the Maharashtra Pollution Control Board (MPCB) ordered the company to cease production of the affected product upon completion of the existing batch. The shutdown commenced on July 18, 2024.

Today, August 7, 2024, Aarti Drugs received conditional approval from the MPCB to resume production. However, the company must obtain additional clearance from the Directorate of Industrial Safety and Health (DISH) before restarting operations.

4 Likes

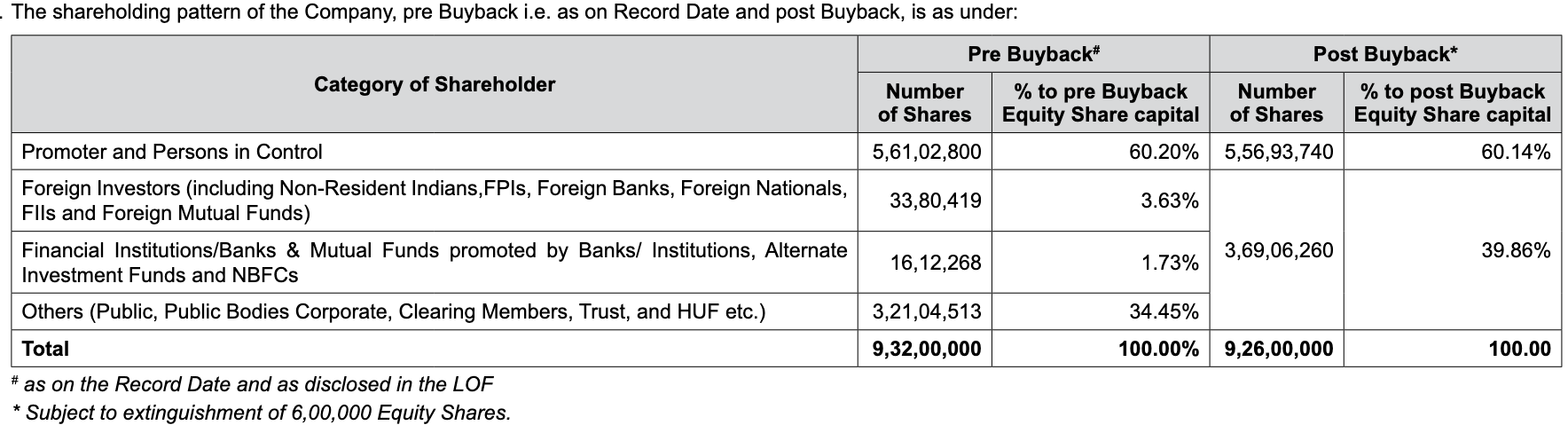

Why Aarti Drugs buy back 2024 was not in my best interest as a long term share holder?

The price of the stock is now 460. The buyback price of 900 was almost double the price. If the management did the buyback now it would have had added more value for the long term shareholders including the promoters.

So why would a company buyback shares at a premium? Does the management value their shares at 900 when they are offering a buyback? Secondly if they think 900 is reasonable price why are they not buying at 460? It does not make good sense to long term shareholders except that they can offer they own share at a higher inflated price. Buying back cheaper does not hurt the company .

The 2021 buyback the promoters reduced by 1% but the small share holders increased 0.1%. So it looks like it were the promoters who benefited from the buyback.

Note:

Older buybacks was also on premium

• FY 2023-24 6,65,000 Equity shares at 900 per share.

• FY 2022-23 6,65,000 Equity shares at 900 per share.

• During the F.Y 2020-21, the company bought back 6,00,000 Equity Shares at a price of Rs 1000/- per share. Post Buyback Public Announcement 21.05.2021

• During the F.Y. 2017-18, the Company has bought back 2,75,000 Equity Shares at a price of Rs.875/- per share.

• During the F.Y. 2016-17, the Company has bought back 3,60,000 Equity Shares at a price of Rs.750/- per share.

Disclosure: holding

3 Likes

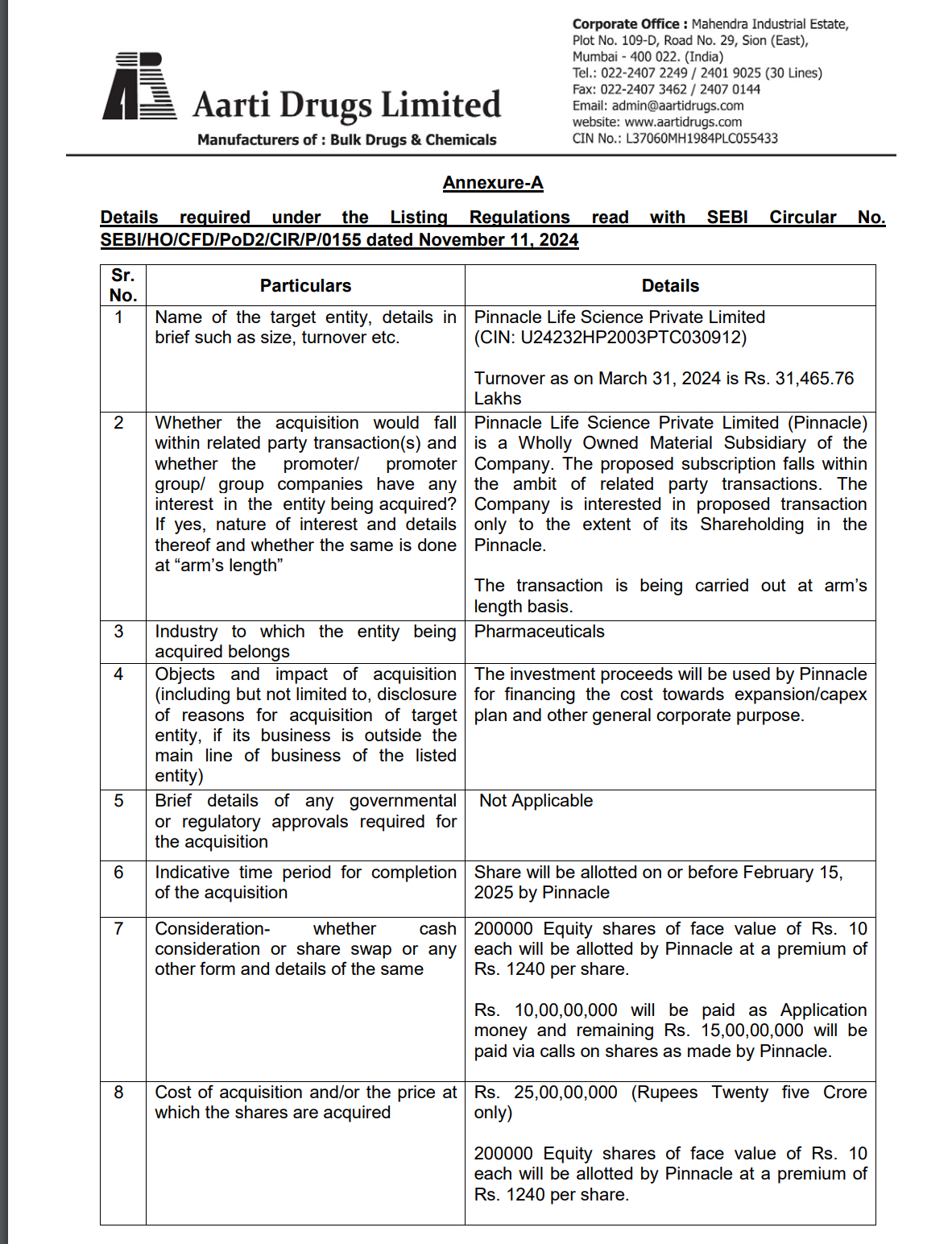

Approved the investment in equity shares of Pinnacle Life Science Private Limited, wholly owned subsidiary of the Company, upto an aggregate value of INR 25 Cr by way of subscription to the Rights Issue.

The investment proceeds will be used by Pinnacle for financing the cost towards expansion/capex plan and other general corporate purpose.

Aarti Drugs | Management Interview

- Management is said to have targeting mid-teen revenue growth in FY26’

- Post weak set of Q3 numbers, he expects a 2-3% price decline in FY26

Aarti Drugs (concall rough notes)

-

Salicylic Acid : Dumping continues Anti-dumping filing by Apr’26

-

Messaging remains consistent. Execution delayed but direction intact.

-

Oncology Commercialization Timeline (New Clarity)

First product to be launched in Q4 FY26

First product to be launched in Q4 FY26 -

Salicylic Derivatives (New Detail)—- Silicates block coming in 1–2 quarters - Volume Growth :FY27 expected: 12–15% — Gross Margin Target (API): ~36%

-

Guidance around Utilisation

Plant Q3 FY26 FY27 Target

——————————————————

Sika 30% 80–90%

Salicylic ~300 T 800–1000 T -

Greenfield projects put together… created a drag of roughly 8–8.5 Cr at EBITDA level and 14–15 Cr at PBT level. Mainly from Sika and Salicylic acid - low utilisation etc

-

Strong signal that Q3 was the bottom. Losses start reducing from Q4 itself. Suggests Q3 disruptions won’t repeat in Q4. Likely QoQ revenue growth. EBITDA margin should improve from 9.3% → ~10.5–11% range

2 Likes