A random thought, picked up from Cal Newport – Gathering inputs is the easy part. It’s the long thinking, and rethinking, then thinking again that’s really needed if you want to produce industrial strength insights.

7 Likes

These are good books to get started:

-

What Works on Wall Street – James O’Shaughnessy

-

Quantitative Value – Wesley Gray, Tobias Carlisle

-

Quantitative Momentum – Wesley Gray, Jack Vogel

-

Dual Momentum Investing – GaryAntonacci

I will keep sharing links and ideas on quant investing on this thread and my blog so do keep an eye out for it.

8 Likes

Thanks

Will wait for your next update. Whenever you find time, please also help with few successful quant traders names.

I have written the following post in Market Meltdown, the Virus, and our Actionables - #67 by basumallick. I am adding it here for my own future reference of my own thoughts during the 2020 GCC (Great Corona Crash!!!).

This is a great thread started by @Donald. Let me put my two cents worth on this. Some of this I have already shared in the following posts:

- AA - Abhishek's Attic (place to store stuff to clear my head)! - #87 by basumallick

- AA - Abhishek's Attic (place to store stuff to clear my head)! - #90 by basumallick

Like in everything I am a strong proponent of understanding the context of a situation. For what we are going through, there is no precedent in history. Never in recorded history of mankind has entire countries and continents stopped working in one go. Let it sink in for some time. Never ever. Not in the 2 world wars nor in during the great plague or Spanish flu or during any other event did country after country shut down their business and basic way of living.

Pt 1 - There is no historical context.

We can compare with the last big fall which by the way was touted to be a once in a century event - the GFC or global financial crisis. A lot of things have changed since then. Interest rates, global liquidity, overbearance of central bankers on financial policy, newer geopolitical alignments are all different now.

To look at the current scenario, I think we are essentially faced with these questions:

- How bad can it get?

- How long can it last?

- What do we do if we are sitting on cash?

- What can we do if we are fully invested?

- What to buy?

Let’s take turns to think through each one.

1) How bad can it get?

I don’t know.

That is the simple answer. But I am personally expecting significant fall even from these levels. My reasoning is as follows:

US newsflow will continue to get worse over the next few weeks. US media, especially those which are popular globally are pro-Democratic and this being an election year, will fuel the frenzy further. India most likely will see increase in cases in the next 1-2 weeks which will fuel the fear of a longer duration lockdown.

The market shrugged off the RBI interventions. We need to see the market reaction next week to assess how the market is taking it, but when good news is swept under the carpet it is never a good sign.

I will be watching the 7500, 7000, 6500 levels on the Nifty closely in case we get to these levels.

On a fundamental basis,

Current Nifty EPS = 439 (standalone)

Possible FY21 Nifty EPS ~ 350-400 (expecting a 20-30% decline in earnings)

At a PE of 15 (standalone) we get a price range between 5250-6000.

At 6000 levels, markets would have corrected 50% from top. This is NOT impossible, even though it sounds improbable.

These levels are NOT sacrosanct. For all I know, markets could have already made a bottom last week.

2) How long can it last?

Again, I don’t know. But I am thinking on the following lines.

The way the economy is shaping up, the world is headed for a recession and India’s GDP is going to contract severely. Different estimates put it at a GDP growth of 2-3%, which is basically half of what was the base case scenario even 3 months back.

Today, sectors contributing to 25% of the GDP is working (telecom, banking, warehouses, pharma etc). 75% is sitting at home. Every month contributes 8.33% of the GDP. So, every month of a lockdown or restricted working impacts the GDP by 8.33%*75%=6.25%. Once the lockdown is released we will limp back to normalcy but the scars of this are unlikely to go away in a hurry.

I am personally preparing for a prolonged 2-year economic slump and consequent bear market or range-bound market. We could actually be oscillating between Nifty levels of 7000-10500 for the next 2 years. (I hope I am wrong!)

3) What do we do if we are sitting on cash?

Wait for markets to get some stability or valuations to become very lucrative. Good quality companies are still not mouth-wateringly cheap.

4) What can we do if we are fully invested?

The probability that markets go down from current levels is much higher than going up from here. So, I would sell ALL stocks which are non-core or where there is little or no fundamental conviction.

Raise some cash in the portfolio so that you can deploy at lower levels. This will also help you psychologically if the market falls further because i) you will know you have preserved some capital and ii) you will have some dry powder to deploy at lower levels.

This is NOT a buy on dips market. So, do not buy on dips ![]()

5) What to buy?

Now, this is the most tricky question. Again this is what I have been agonising over the last 2 weeks. My thoughts are on the following lines.

If my base case of a prolonged bear market holds, then I need to look for companies which have:

i) strong free cash flows

ii) Zero or very low debt

iii) Real assets

iv) Moderate absolute growth

v) Good dividend yield

These are additional parameters to the normal ones of good management, high ROCE, reasonable valuations etc.

Pockets of opportunity would most likely be from the following:

i) Consumer discretionary

ii) FMCG

iii) Pharma (both domestic focused and export oriented) and ancillary (API)

iv) Agriculture and Food

v) Speciality Chemicals

vi) Utilities (electricity, gas)

vii) Strong banks & NBFCs

Longer-term opportunities need to be bottom-up.

Over the next 2-years, we need to be more cognizant of the overall market context than before should deploy a part of the portfolio in “value trades” rather than only long term buy and hold stories.

The beauty of the next 6 months would be the bleak short term outlook and the great longer-term opportunity. I would be on the lookout to find a balance between the two. It would be a great time to bring the word “multibaggers” back from the dead once again!!!

25 Likes

Jim Simons

Ed Thorp

James O’Shaughnessy

Cliff Assnes

Ed Seykota (part technical part quant)

Richard Dennis

William Eckhardt

Jerry Parker

Gary Antonacci

Perry Kaufman

Kevin Davey

Nick Radge

Ernie Chan

Andrea Unger

3 Likes

Supply chain optimisation likely to incorporate redundancy and failover → Will this lead to dollar collapse? Why would china and japan keep the treasuries in that case.

What are your views about war or at least a skirmish west vs china? Its 20 years US has not gone to war?

Thank you for the detailed analysis

I am a bit confused

You are saying "one should sell non core stocks to get some cash that can be deployed at lower levels but then you are also saying don’t buy on dips "-so when does one deploy that cash since there’s no way to know where the bottom?

Can you help clarify the dichotomy between the two statements ?

I see that you have steered clear of IT sector on “what to buy” -dont you think the rupee depreciation will help the IT behemoths maintain (if not grow) their earnings ? Besides they do offer dividend comfort since their profit margins are huge and can still sustain dividends even if they have short term earnings impact (I am referring specifically to the large cap IT stocks like TCS, Infosys, HCL Tech)

Thanks

When you buy is very clearly (atleast to me) mentioned in the answer to qs 3.

I dislike IT sector because all are me-too businesses which are perenially cannibalising each other’s margins. Just buying because rupee may depreciate is not a good enough reason for me.

2 Likes

I did not get your connection between supply chain optimisation and dollar. Please elaborate.

No clue. Not interested to have a clue as I consider it a known-unknown and waste of time to theorise about. If it happens, it happens. Why bother about it now. There are better ways of global domination than to go to war.

1 Like

As you have put it localisation is a strong case because of huge unemployment in US localisation may be the answer to address the problem of unemployment. China wants to keep its currency competitive to keep its exports viable. In case of localisation they have no incentive to keep the treasures and hence sell them.

I have not talked anywhere about localisation. I have talked about supply chain optimization with higher slack, redundancies and failover built-in.

As per localisation, US is not cost-competitive in most businesses and it is unlikely to change anytime soon. Some manufacturing can get back to US but wherever it is labour intensive US will be at a disadvantage.

1 Like

Wait for markets to get some stability or valuations to become very lucrative. Good quality companies are still not mouth-wateringly cheap.

4) What can we do if we are fully invested?

The probability that markets go down from current levels is much higher than going up from here. So, I would sell ALL stocks which are non-core or where there is little or no fundamental conviction.

Raise some cash in the portfolio so that you can deploy at lower levels. This will also help you psychologically if the market falls further because i) you will know you have preserved some capital and ii) you will have some dry powder to deploy at lower levels.

This is NOT a buy on dips market. So, do not buy on dips

Q3 says to wait till there is stability and valuations will become attractive

Q4 says to raise cash but don’t buy on dips

But valuations will become attractive only if markets dip

Hope this explains my question

I agree that this is a good time to keep cash ready and deploy it if markets dip. However, in my humble opinion, it is better to deploy at every drop ( say 10 percent drop in nifty) since no one knows where the bottom is.

I am surmising that you expect a bigger drop and are telling investors(especially who have limited cash) to wait for that drop instead of buying in dips

IT sector is not a growth sector anymore. Indian IT cos catering to international market (dominated by 4 TCS, Infy, HCL Tech, Techm) are not inventing anything, they are not on the cutting edge, they are service industries and are already massive, to expect a growth of 10% y-o-y is a little much with absence of triggers. Cutting edge is in the Silicon Valley.

Sure, they are cheap and safe right now. One could invest and get safe returns. But, with the market giving such good corrections one ought to aim for more.

This is evident by seeing Wipro, Infy, Techm, HclTech reaching for lowest of PEs in a decade. Market pays high valuations (PE) for visibility future growth.

Just my 2c.

Thanks for sharing your perspective

People have been commenting that IT services growth is going to stall because of linear model and not developing products -both tcs and infy develop banking products and bfsi is their biggest business -

Further if you see sales growth of TCS over the last 5, 10 years, it has continued to grow despite all this

Yes, cutting edge is in silicon valley but most of these companies outsource a lot of their non core work to service companies which is a steady source of revenue and which becomes a moat (for service companies) because of high switching cost

Abhishek -while you may be right that IT companies are cannibalising each other’s margins, a company like TCS cannot have the growth it’s had as well as ROCE around 50 percent if it was a commodity business

Rupee depreciation is just one of the things I mentioned -ofcourse i still expect growth in the next few years largely on digital initiatives

One should not ignore the high switching cost (moat) which allows them to get repeat business.

Disc: Invested in TCS

Hi Jami /Abhishek ,

IT sector in india is mostly into me too segments & are purely based on cheap labour .

But i was loking at LTTS & KPIT (not birlasoft).

Especially KPIT is working on cutting edge technology like self driving , mechatronics & ADAS (automotive software). I worked in Intel & presently in qualcomm & automotive is the next big sector , every electronics company is looking for .

Please let me know whats your opinion on KPIT?

1 Like

Abhishek great point. I am trying to come up with a worst case scenario math for bajaj finance due to the corona effect. Ofcourse, this is only a guess

Assume

no loan origination for 6 months.

credit cost spike of 200 bps.

Then

Interest cost = ALM mismatch would be 28k CR (pg 24 q3FY20 inv presentation), assuming 8% interest for 80% of it. Thats 1800Cr.

Credit cost = 2% of 145k Cr. 2900cr.

Book value drops by 2900+1800 = 4700Cr.

Current book value 30k Cr - 4.7kCr = ~25Cr.

5 times book = 125k Cr. (Assuming RoA is around 4 and leverage 6. 24 RoE. deserves atleast 5 times book)

FV around 2000-2100.

Any holes in my assumption / math?

The problem is with a scenario like what we are in, it is very difficult to model the worst-case scenario, because we do not have any historical context of what can go wrong. Lot of questions remain unanswered. Will NPAs shoot up if a large part of the loans cannot be serviced? Will people be willing to spend as much after they come out of these testing times like what they were doing earlier? How long will this last, 3m, 6m or 12 m?

So, in these scenarios doing a lot of excel analysis does not help. Usually a high-growth company like BAF is valued on PE and not as much on P/B. And the valuation part is more art than science.

2 Likes

We have had these scenarios earlier.

Flu: Spanish flu during WW1, various flus during middle of 20th century viz. Hong Kong Flu, Swine flu , H1N1 during 21st century. These hit some places very hard and we can extrapolate people’s behaviour from that.

Also Demonitisation was a time when incomes shrank and people weren’t sure about the future, that was even a Black Swan (which this isn’t).

Also, since the flu ravaged China 2 months earlier, Chinese behaviour should be 2 month prior to Rest of World, we have a sure model to see.

2 Likes

The Q30 portfolio was down in March by 13.3% after being stopped out in 2 progressive steps.

Quarterly 31st Dec to 31st March Q30 is -18.24%

5 Likes

Notes from Bias-Information-Noise paper by Michael Mauboussin

-

Anticipating revisions in market expectations is the key to generating long-term excess returns as an investor. This process requires you to understand current expectations and why they are likely to change. A company’s fundamental results are the primary catalyst in expectations revisions. These include drivers such as sales growth, operating profit margins, and return on invested capital. Successful long-term investors see where expectations are headed based on their forecasts for fundamental results.

-

Ample research shows that most experts do not make great forecasts. This might appear to be a problem if you are in the business of making predictions. But it turns out that the ability to explain what happened after the fact, often in a way that flatters your faulty prediction, is an incredibly effective coping mechanism. Barbara Mellers, a professor of psychology at the University of Pennsylvania, says, “We find prediction really hard, but we find explanation fairly easy.” We tell stories to ourselves and others to paper over our poor predictions.

-

The difference between superforecasters and regular forecasters is “due more to noise than bias or lack of information.” The researchers conclude that “reducing noise is roughly twice as effective as reducing bias or increasing information."

-

Another area where noise can creep in is position sizing. Effective investing has two components. The first is finding edge, where a security is mispriced and hence offers the prospect of excess returns. The second is position sizing, or how much money to invest in the idea.

-

The investment industry spends a lot of time on edge and little time on sizing, and it is likely that sizing decisions are noisy for many portfolio managers. Research shows that investment managers leave returns on the table by failing to follow the position sizes suggested by their own processes.

-

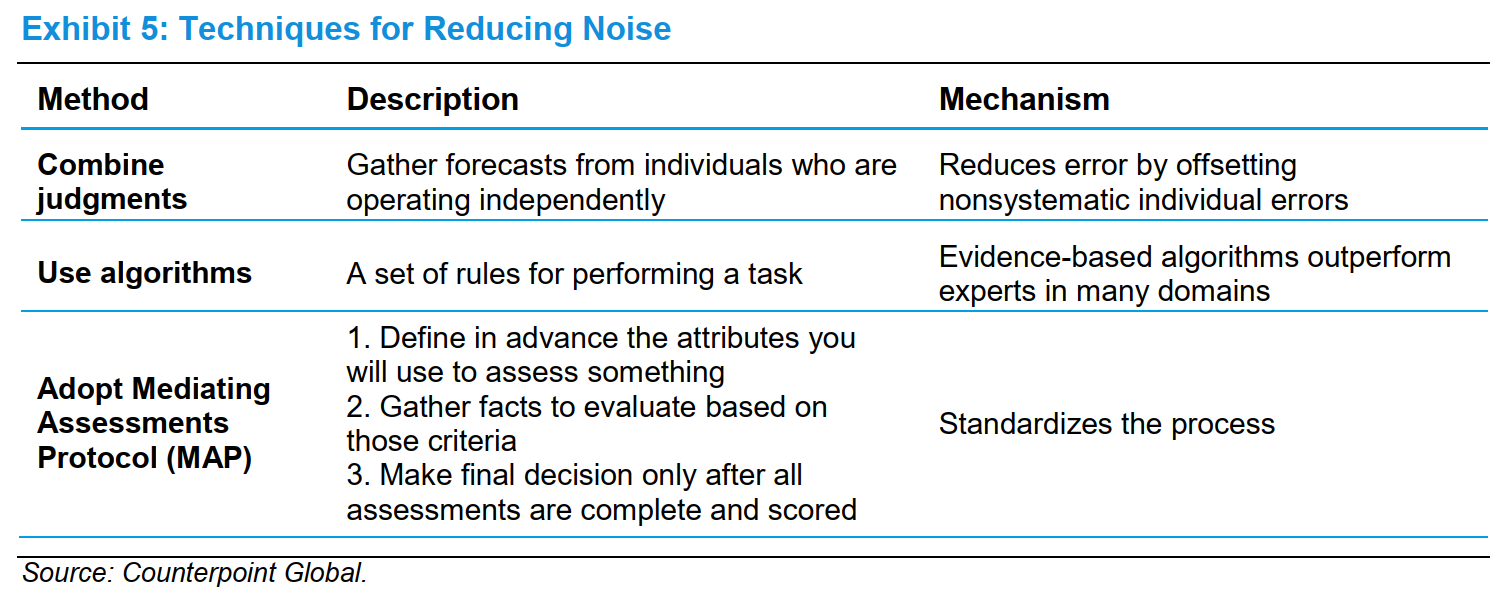

The three primary ways to reduce noise are combining judgments, using algorithms, and adopting the “Mediating Assessments Protocol.”

-

Because noise is nonsystematic, the first way to reduce it is to combine forecasts. This is the core idea behind the wisdom of crowds. While each individual may be off the mark in a random way, combining the forecasts reduces the error and increases accuracy.

-

A second means to reduce noise is to use an algorithm, which is simply a set of rules or procedures that allow you to achieve a goal. For example, a cake recipe is an algorithm. If you follow the procedures for how to combine the ingredients and bake the batter, you will end up with a tasty cake.

Reducing Bias:

-

The first is to incorporate base rates into a forecast, which addresses overconfidence. It is common for forecasts to be too optimistic, whether it’s the cost and time to remodel a home, how long it will take to complete a task, or the growth rate of a company. Introducing base rates often tempers and grounds an estimate.

-

A second method to remove bias is to create formal mechanisms to open the mind to alternative possibilities. One technique to do this is a premortem.

-

One crucial point is that forecasts should use numerical probabilities instead of words, which can be interpreted to represent a wide range of probabilities. Numbers allow for an ability to score forecasts precisely and to avoid ex post justifications.

source: https://www.morganstanley.com/im/publication/insights/articles/bin-there-done-that_us.pdf

7 Likes