We need to adopt Hamsakshiranyaya (close english phrase is Selective absorption) . Everybody have some good quality , we need to take just that one and progress in our path ![]()

3 Likes

5 Likes

What to do now?

The last few days have been extremely volatile. If you have watched the last interview I gave on ET NOW, I had mentioned that my sense is we will remain extremely volatile in the next 4-6 months before things get better. For those who might have missed it, here is the link. Margin pressure will ease because raw material prices are likely to stabilise. Inflation will also start looking better because last year’s high base rate will come into the picture and year-on-year growth in inflation will look lesser. Also, with the passage of time, the knee-jerk reaction of market participants will also likely reduce.

One interesting phenomenon to watch for is the FII / DII / retail investor flows. My sense is, and I could be completely wrong, that we will see a reversal in trend and see FII inflows and DII/retail outflows. FIIs will come looking for a safe haven and where there is some semblance of growth in an inflationary world. Retail investors, many of whom are first-timers, will be seeing their portfolios taking a beating and their fundamental assumption that making money in the market is easy will get challenged. Also, with normalisation post-Covid, people would return back to their professions and free time and mind space to dabble in trading will reduce which is more than likely to reduce their fund flows.

Another point which I tell often and probably is a great time to reiterate now is that market returns are non-linear. A 20% CAGR does not mean you will get a 20% return every year. Returns over shorter periods will be all over the place. Some years we will see negative returns and some years we will see very large returns. In general, if you are investing in equities, always keep in mind that a 10% correction is likely every year, 20% every 3 years and 30% every 7-8 years.

As investors with a 3-5 year view, I think it is a great time to remain disciplined. Those who sip into the portfolio stocks, keep doing it. One slight modification you may want to do is increase the frequency of deploying your capital. If you were buying once a month, do it 3-4 times a month now. Buy on the days when the markets are crashing. That way you are likely to benefit in two important ways:

-

you will get a better average price

-

you will feel happier that you have bought at a lower price (and this point is actually psychologically more important)

We are now going through a regime change. Years of easy liquidity policy is ending globally along with forces of deglobalisation and higher inflation. Any transition is painful, but fundamentally, I think India is placed in a much better position today than at probably anytime in the past.

I am hopeful for the future.

51 Likes

Sir,

What has been the historical correlation between inflation and real-estate prices? Are real-estate prices expected to go up with inflation or it is another way around?

Thanks

1 Like

True. In this respect, the recent repo rate & CRR hike is very much a good thing. Data shows historically our markets have done well under rising interest rates. For FIIs to invest in emerging markets, the first thing needed is currency stability. FII flows will very much reverse if RBI continues with tight money policy. And a lot of corporate deleveraging has happened in the last few years, so corporate profits will not be affected much by interest rate hikes. Stocks will move from speculative players to stronger hands.

6 Likes

US Housing

The Federal Reserve (US Fed) is done watching inflation run away and has made it a priority to cool down one of its biggest drivers: the housing market. With rising mortgage rates, Americans will not have the easy money to purchase real estate which is expected to cool down the real estate in the US.

- In December, the average 30-year fixed mortgage rate sat at 3.11%. That rate is up to 5.27%—its highest level since 2009.

- During much of the pandemic’s housing boom, historically low mortgages shielded homebuyers, to a degree, even as home prices shot up nearly 35% over the past two years.

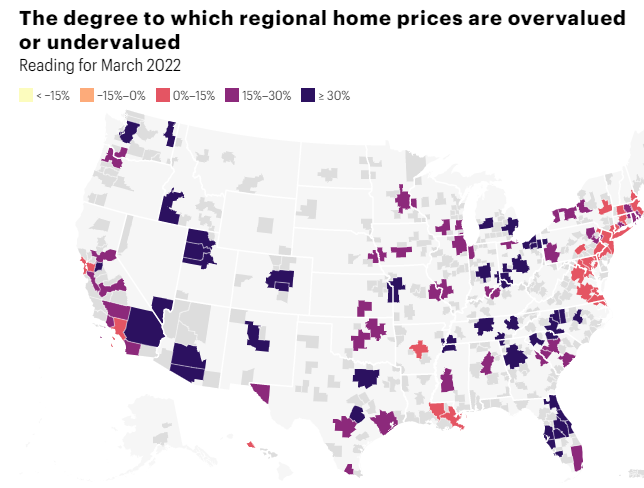

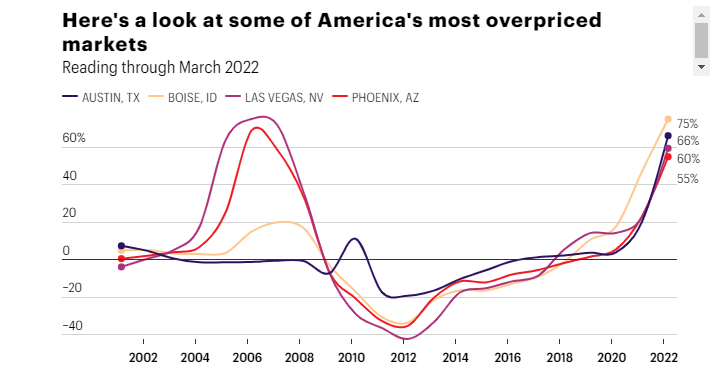

- An analysis provided by Moody’s Analytics finds that 96% of regional housing markets are overvalued, and 27% of markets are overvalued by more than 30%.

- The most overpriced markets are Boise (by 75%); Austin (66%); Ogden, Utah (63%); Las Vegas (60%); and Atlanta (60%).

- Case in point: The metros of New York City and San Francisco are overpriced by just 3% and 13%, respectively.

Why did the market rates of houses move up?

- Work-from-home made houses more important than ever

- Home prices continued to rise to create a Giffen effect on the population which created a FOMO effect on them, coaxing them to purchase a property

- Demand is concentrated in specific areas, especially the suburbs as the rates in metro cities like NYC and Detroit were already high.

- Inflation forced people to buy real assets like houses

- The migration to suburbs to find peace and better quality of life has become more real than before during the pandemic

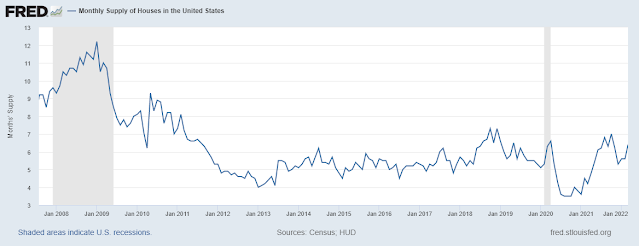

- The continuous increase in housing prices has also reduced the supply of houses in the market. Homeowners are unwilling to sell their houses even though the prices have started to cool down from March.

- The price of labour, housing materials and other expenses have also risen sharply in recent times

Monthly supply of houses in the US

30-Year Fixed-Rate Mortgage Average in the United States

As per JP Morgan, the nationwide nominal house price index is now 40% above its 2012 low-point and 4% above the peak reached in 2006.

Challenges faced by the industry

- Rising Prices of materials, labour

- Improper suburban settlement plans

- Improper tax distribution across government states

- Prices went on a bidding spree with only the upper class and upper-middle class being able to safely bid for a house in the market

- The skyrocketing prices have led to a fall in demand as people are simply not able to afford the house

- Homeowners are not interested in selling the house at current levels either, Supply is still shorter than demand thereby increasing the prices in the long run.

In summary: Although housing is a very local-driven market and aggregate data does not show the true picture, it definitely looks like the US housing market could be in for a period of consolidation and pause. Implications for businesses that are part of the US housing supply chain could see a definite fall in revenue growth and contraction in margins.

11 Likes

In general global supply chain disruptions are a key driver of inflation. A key word here is D-globalization: New Supply Chains Are Inefficient and Will Drive Up Inflation

Also QE goosed the stock market and that boosted demand for cars and second homes.

There is a lot of doom and gloom around with a recession talk, I am not sure if best to exit my positions and re enter when I feel macro indicators improving or stay invested even if it means weathering a multi year slowdown.

There are no easy answers to this. It has to be a stock specific and personal situation specific decision.

I think a falling market will take everything down irrespective. No point holding onto anything if a recession is expected.

Loss harvesting is probably the best plan if anyone wants to hold on.

Investing like Federer

Let me start with a story.

One day an elderly couple saw a young man, probably in his early thirties, playing tennis in one of the corner courts of their exclusive country club in Florida. This couple had spent their entire life engrossed in their business and had never really followed the sport. They had sold their business and chose a peaceful retired life. Now that they were retired and extremely wealthy, they thought that picking up tennis would be a good thing. The young man who was playing seemed to be doing it effortlessly. The lady decided to try her hand at the sport. The next day she approached the tennis director at the country club who promptly enrolled her on the tennis program. To her dismay, the lady found that the game was really difficult. She was not able to control the ball. It was either sailing wide of the court or hitting the bottom of the net. She went to complain to the tennis director saying that the game which she saw being played by the young man seemed so easy. The guy did not even seem to be making an effort. And here she was huffing and puffing and yet not able to make a single shot. The tennis director turned around and said, “Maam, yesterday the person you saw here was Roger Federer. He is perhaps the greatest tennis player in the history of the game”.

This is a true incident.

Why am I telling you this story?

Just like studying about or watching Federer on TV will not help you play like him, similarly reading Buffett, Munger, Lynch and others will not make you invest like them.

The availability of information today, especially on social media, is so much that just by repeated exposure people tend to get a feeling of expertise. It is like if you see a cookery show about making an omelet everyday for six months, you will start getting a feeling that you are an expert at it. It may not even occur to you that you may not know how to even light the gas stove. Making a great omelet is really not easy. How hot should the oil be? How much do you beat the eggs? How much salt to add? How long should you fry one side? When do you flip sides? None of this can be learnt from watching omelet-making videos. You need to live through it, experiment with it and then slowly after a few times you will get a hang of it.

The same thing applies in investing as well. Repeated exposure to investment gyan and discussion provides an illusion of knowledge. Investing is a “lived” skill. The legendary trader Paul Tudor Jones once said, “This skill is not something that they teach in business school. I get very nervous about the retail investor, the average investor, because it’s really, really hard. If this was easy, if there was one formula, one way to do it, we’d all be zillionaires.”

Becoming a good investor takes dedication, patience, curiosity and tremendous hard work. It requires building up a network of investors and industry contacts who can help you do the scuttlebutt. Just sitting and reading in a room with no computer screen sounds idyllic but is not the reality. At least not for people when they start off. Maybe, it can be done after spending fifty years in the investment arena.

Here are some pointers for those who wish to learn to play at the top of the league.

- Practice everyday: This means you need to study a business or industry everyday. All knowledge is incremental, so if you keep doing it, it will compound.

- Learn the language of investing: You need to be able to read the financial statements.

- Inculcate the right mindset: The biggest determinant of returns over longer periods comes from investor psychology. Two people buying the same stock at the same time at the same price may end up with completely different results as one may be able to hold on through many ups and downs and the other may sell in panic or euphoria. The way to build the right psychology is to reflect on your past buy/sell decisions, the reasons why you took them and what would you do differently if the same situation arose again. Maintaining a decision journal in the initial years might also be very useful.

In summary, we need to understand that the game of investing requires a lot of hard work and dedicated effort. When the masters play, they make it look easy. But it isn’t. It is actually a very difficult game. And that is why the success rate is very low. To get the odds in your favour, approach it like an elite athlete.

71 Likes

In this day and age of a lot of social media circus, this article articulates the true essence of investing. Well written.

Over past year, I had a first hand meeting with a lot of gen X wannabe investors, and nearly most of them wanted to take the 2 minutes Maggi route. Few of them wanted to do the hard yards of reading, observing and thinking.

The usual recourse was to do quick learn courses online for a few days or weeks and plough right into the markets like a gladiator.

The markets had been kind over past many months and so these types of investing/trading worked. But once the trend turned, the true brutal nature of Mr Market was revealed and a lot of newbie/wannabe guys suffered.

Investing is a long test match like game where the first few attributes needed are temperament and a thirst to keep learning. Learning has to be from books/ experienced guys/ mistakes (preferably of others) / observation of how markets and stocks behave and above all learnings from history. History keeps repeating itself in terms of market and investor psychology, only the cover and contours change. The basics at the DNA level always remain the same.

What most investors need to know is that they need to be patient while learning and keep the passion going. And preferably try to forge alliance with friends/acquaintances/ others who have made it big in the field. There is no replacement for an experienced observant investor who has seen a few cycles and learnt the right things.

Many a times simple home truths fail to penetrate thick resilient skulls. I have been observing changing market fancies for various sectors/stocks. And the key message has always been to avoid stocks that were once market darlings but now have lost that fancy. But people are so enamoured with past winners that they keep looking at rear view mirrors, but fail to see the happenings right in front of them, and miss sitters. Such a simple concept, but I find that very few implement it.

61 Likes

Sit tight, fasten your seat belts and enjoy the bumpy ride

Edited excerpts of communication sent to subscribers on 12-Jun-22

As I have mentioned in all my previous videos and emails in the last few months, the next few months are likely to remain extremely volatile. Markets will fall sharply and when people get really scared and you start hearing doomsday all around you, it will surprise everyone and turn around and rally for a few days.

Markets, as is life, move in cycles. Sometimes, the times are good for us and sometimes they are challenging. The interesting part is people often forget this reality. In good times, they forget that bad times are ahead. And in bad times, they forget that good times are ahead. In Chinese, there is a concept of Yin and Yang. It talks about a system being composed of complimentary but interconnected or interdependent forces. Bull and bear markets are similar.

What To Expect From The Market

There is a possibility of a sharp down move in the next month or so, probably led by global cues. However, it is a possibility only and not a certainty. You would have noticed that both in Hitpicks and Quant, we have a large part of the portfolio in cash. The reason is that these are short-term oriented and I would want to be a bit more certain of the overall market trend before committing fully.

In the long-term service, we have about 15% in cash. I am not inclined to sell more and go to cash aggressively even though the possibility of a sharp downswing cannot be ruled out. One reason for that is, as the name suggests, it is based on the long term, and most of the stocks do look good from a two-three year perspective and if I just ignore the immediate next one-two months of concern. So, the objective for me is to look out over a 1-3 year horizon in the long term service and calmly accumulate stocks which can give me a decent return over the next 2-3 years.

For those who are in our PMS service, you would have seen that we are deploying your capital in a slow, steady and systematic manner. We will continue to do so.

The Medium-to-Long Term Outlook

I am actually fairly positive. Maybe unusually so. I see a fair deal of optimism in the management of companies during concalls. As long as we don’t see another bout of Covid flare-up or a nuclear war or some such black swan event, the Indian economy actually seems to be on a very strong wicket compared to what is happening in the world around us.

Inflation is a concern, but 75% of Indian inflation is related to food and I expect it to come down with the monsoons. Inflation also will start cooling down once the base effect of last year kicks in. The rate hikes which everyone talks about are a non-event for me. We are just correcting the Covid era rate cuts. It is unlikely to have a great deal of effect on corporate growth. Bank credit to commercial enterprises is steadily going up signifying underlying recovery in the business.

The China + 1 theme is playing out very strongly on the ground in multiple sectors like chemicals, textiles, engineering and electronics. Over the next few years we are likely to see a silent out move of MNCs from China and into other sourcing markets like India, Vietnam, Indonesia, Malaysia etc. Covid and the Ukraine-Russia war coming back-to-back has necessitated a major strategic shift in single country sourcing. While this is going to be long term inflationary in nature, countries like India, with abundant manpower and natural resources can benefit.

A lot of sectors are looking good and some cyclical sectors are at the cusp of recovery - autos, real estate, infrastructure, engineering and capital goods, agrichem to name a few. My promise of some changes in the Long Term stocks still remains unfulfilled. I have multiple good stock ideas but am waiting and twiddling my thumbs because I think we will get a better entry point ![]()

As I mentioned in my previous mail, those who are doing SIP can continue to do so. Just spread it out a little bit more if possible. And if you are a bit active in the markets, try and buy a little on days when the world seems to be ending ![]()

My sense is that we are headed for a very good 2-3 year period once we cross this volatile period in the next couple of months. So, sit tight, fasten your seat belts and enjoy the bumpy ride ![]()

Footnote:

- Also, last week I shared some views on the LIC IPO on ET NOW 9pm news. You can watch it here:

32 Likes

My feeling is that this time ,this correction would go upto minimum December . And at the end of this correction, we will find so many good companies available at very low prices . May be at such low prices that current good ideas would look expensive in context of better companies available at much cheaper prices.

If I was at your place, I would rather wait for next 4-5 months to stater shortlisting my purchase list . And i would rather dont do any SIP as SIP has to be done in uncertain times. Not in the times when we can see clear clouds. Better to wait for some more time, we can buy more quantity with the same amount.

4 Likes

Watched your complete thread today. It was really awesome and also got inspired by your overall journey and the hard work you put into it.

some questions :

-

Before covid, you were posting the Quant method results of your portfolio on monthly basis and the CAGR for each month. But it was stopped after some months. I am very curious about how it fared till now, if you are continuing…Specially the initial CAGR was way too awesome around 130% and all…so after 2 years, whats the status now?

-

You had mentioned that passive Index investing is also a sort of Quant method…But it was just a passing reference. If you could kindly throw some more light on this aspect. How you view Index Investing, compared to individual stock picking…other than usual aspects…

Thanks in advance

5 Likes

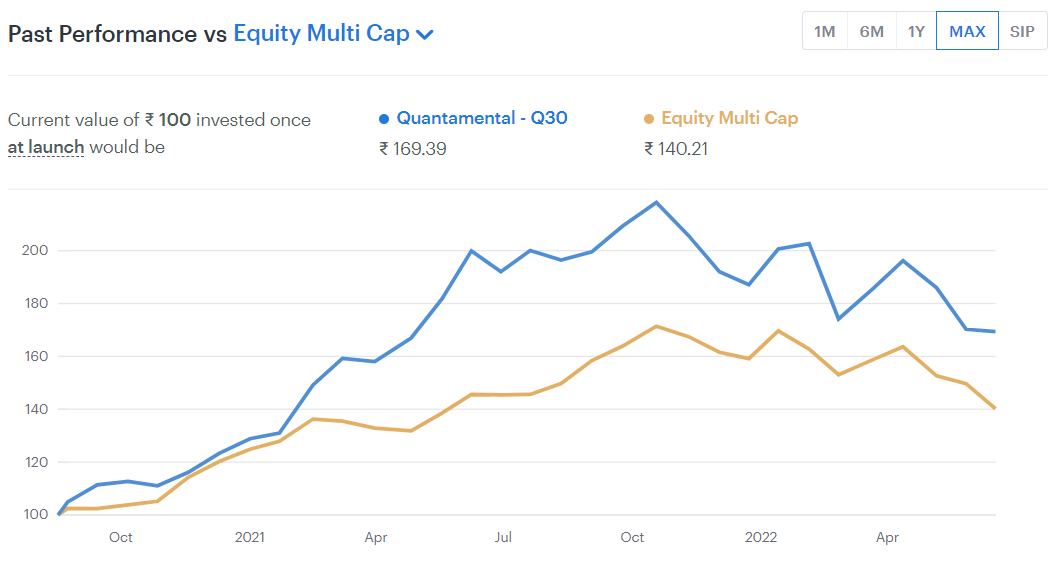

@Mudit.Kushalvardhan Thanks for the nudge.

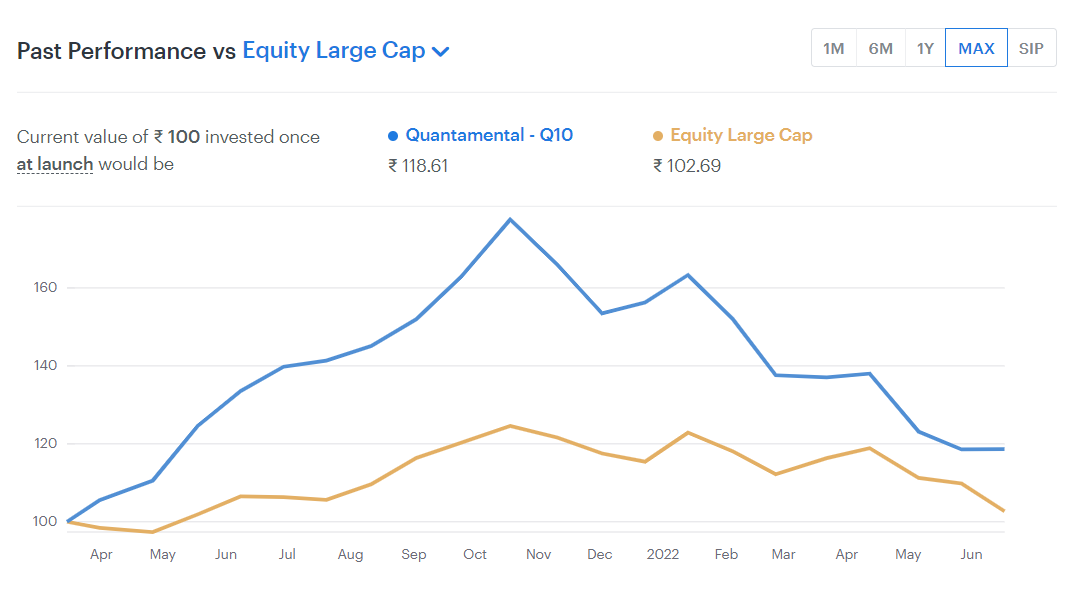

Actually, the reason I stopped posting the results was that I started two smallcases using the same (similar) momentum strategies that I had earlier mentioned and since smallcase worked as a thrid-party independent & authentic source of return calculation, I got lazy in tracking it myself on excel.

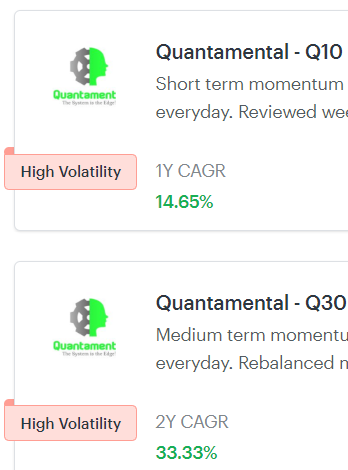

The Q10 strategy (large and mid-cap only) has had a decent performance considering that the market has been in a correction phase.

Q30 (which is all caps) has been around longer and also held up reasonably well.

Momentum strategies, by their very nature, will outperform extremely well when the market is in an uptrend. It will not perform well in a consolidating or whipsaw kind of market. In these markets, value or mean reversion systems will outperform. unfortunately, I am still stuck with not being able to figure out a reasonably good mean reversion system ![]()

6 Likes

How is an index constructed? Let us walk through an example of constructing an index for ourselves. Let me call it “The Great Indian Index (TGII)”!!

What are the key decision factors here?

- How many stocks will be there?

- What stocks to include?

- How will the allocations be for each stock?

- How long will we hold them? i.e. what are the exit criteria? Is it going to be a fixed duration or will there be a trigger event?

Now, assume we have done a lot of research and decided that we want TGII to have 40 stocks - midway between 30 in Sensex and 50 in Nifty ![]() That takes care of pt 1.

That takes care of pt 1.

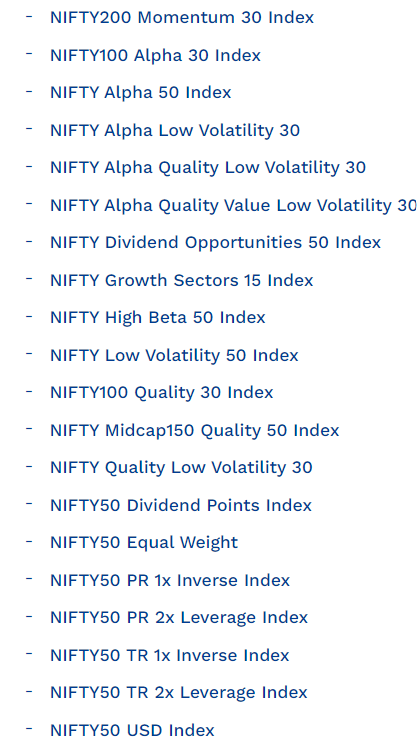

For pt 2, the easiest is to pick the largest 40 by market cap. That’s what Nifty 50 does. You can add layers of complexity / sophistication on stock selection for the index. https://niftyindices.com/indices/equity/strategy-indices is a fantastic resource where NSE publishes a number of indices and gives a detailed discussion on how each is constructed. below are just some of the indices in it. Another important aspect that is to be kept in mind is stock trading liquidity. You want only those stocks in your index that has a minimum threshold of daily volume.

Now the easiest way to solve for allocations, pt 3, is to start equiweighted. That is, each stock will have 2.5% allocation. Other ways of allocation are, you can overweight on momentum (simple last 6 or 12 months performance) or value (lowest PE or PB or EV/EBIDTA etc) or quality (high ROCE). So, you can say I will have allocations from 2% to 5% based on my filter criteria of value, momentum, quality etc.

The last pt is when to rebalance. Easiest is to say, we will rebalance every quarter or 6 months or one year. That is fixed frequency/duration rebalancing. Nearly all indices do this. One reason they find technical based or fundamental based rebalancing (like stock based individual portfolios can) difficult to implement is in bear markets you may not find 40 stocks to fill your index. And an index cannot hold cash ![]()

That’s it. That is all there is to an index. I have tried to write it in simple terms here but every index is constructed on similar lines.

15 Likes

Hi sir,

Don’t you think Q-10 & Q-30 should be compared with Nift200 Momentum 30 Index or some other similar type of Momentum Index, considering it works on some what same principal.

The idea of a benchmark is one in which an average investor can alternatively invest in. The strategy indexes are mostly not implemented. And Nifty 50 is by far the easiest alternative that an average investor can invest in through an ETF / index fund.

1 Like

Can you guide how much percentage of one’s portfolio should be in Index Funds and how much should be in direct stocks? What must be the criteria for this?

1 Like

@Mudit.Kushalvardhan There is no rule. Though, people tend to invest a higher percentage in stocks than in Index funds.