Expectations Investing by Michael Mauboussin is a very good read. I had covered it as part of a presentation I made a few years back.

5 Likes

Thanks for sharing the slide. Is it available anywhere to peruse? Would love to go through the presentation.

I had done a webinar for the Indian Investing Conclave which covers a broad range of topics.

The free webinar playback is available at Indian Investing Conclave

In case the link does not work, you can use Indian Investing Conclave and scroll down to episode 10.

The presentation deck used is the one below.

Indian Investing Conclave.pdf (1.1 MB)

22 Likes

To summarize, you need to focus on understanding the business and its various levers well enough to figure out it is screaming at you to buy or sell. If you need excel for it, you don’t know the business well enough.

This statement of yours is somewhat misleading…I request you to pls clarify. If you dont use DCF, then how do you value a company?

I am asking cause I use DCF all the time…and till date haven’t seen anything better.

And since you manage money for others I am all the more curious to know that if you dont use DCF then what do you use?

Rgds

RR

2 Likes

There are many ways to understand whether a stock is overvalued or undervalued without using any calculation at all.

DCF is practically useless as a tool because the percentage of times it can get to the right result is miniscule. A follower of DCF will miss most of the best performing stocks at all times. You just need to go back in time and do a DCF for HDFC Bank, Asian Paints, Pidilite, Nestle etc say twenty years back.

Whereas DCF is mostly an academic tool for students, the DCF mindset is important. Using the process to walk through the story and your set of assumptions are important. That leads to a better understanding of the business.

One of the biggest drawbacks of DCF is that it does not consider the transaction value of an asset. And that is the reason why DCF cannot value an asset that does not have a cash flow. Does it mean say the “Mona Lisa” has no value because it has no cashflow? Monal Lisa has what is termed as transaction value. Someone is willing to pay something for it (for whatever reason).

Every asset value can be broken up into two parts—i) intrinsic value, which is derived from its tentative future cash flows and ii) transaction value, which is derived from what value someone else will pay for it in a transaction.

And this is one of the main reasons DCF falters, other than of course the fact that assumptions about the long term future nearly always tend to be wrong.

I don’t value companies based on DCF. I try to understand the strength and longevity of the business and try to see what range of earnings are possible in the next 1-2 years, in a probabilistic range. And see what a buyer might be willing to pay post that period.

Another way I look is to see in simple terms how many years will it take for the business to return the capital to the owner if it was completely bought out.

So, I don’t do anything fancy. Simple back of the envelope stuff and it works perfectly for me. I know that I don’t know the value so don’t get into heated debates on valuation with anyone and waste my time ![]()

25 Likes

Excellent post Sir.

To balance this out, I believe Mr Mohnish Pabrai has included sale value of the stock in his DCF calculation in the book ‘The Dhandho Investor’, i.e. he has included every year cash flow plus the inflow arising from the sale of the stock after n number of years (here n may vary depending on how long you wish to forecast)

One of Mr Buffett’s reasons for criticizing cryptocurrencies, I believe, is because they don’t produce cash flow (as he explains here). I personally agree with his logic. In fact, I would say even Mona Lisa painting has cash flow- as it is displayed in a museum and is one of the key attractions for tourists. Tourists paying for tickets is essentially cash flow, right?

1 Like

DCF versus not is a never-ending debate. My current belief is that just as there are many ways to bell the cat and make money in the market, there are many approaches to doing a reasonable valuation. All of them flawed (DCF may be theoretically perfect, but even that is debatable), and some useful elements in many of them.

It probably boils down to which one works for you and your personality. At the end of the day, you need to be comfortable with the approach, and it needs to support your conviction. For some people, a DCF does that; for others it may be other methods.

I’ve personally evolved(?) from a DCF builder, to someone who does not use it much today. However, I can see the value of DCF modeling for someone whose mental makeup can derive support from doing this exercise.

In the end, Mr. Market is going to humble you sooner or later, whatever approach you use. But if you are truly open and humble, Mr. Market also rewards you well.

So bring out your DCFs, your XYZs or whatever tools suit you best. Just don’t forget to keep an open mind, and remain humble.

Best of luck to all!

3 Likes

Many thanks for your response. Really appreciate you took the effort of typing out your mind.

Cheers

Rajesh

3 Likes

Every year the market gives a patient investor an opportunity to buy.

The issue is it is very difficult psychologically to buy when the market is collapsing around you.

That is why a systematic strategy works well. It takes the psychological element out of the game.

10 Likes

For investment / trades in shorter timeframes (1-3 months), buying stocks at new highs is better while for longer term (3-5 yrs), buying quality stocks at market dips/lows is better. Even for longer term, it is better to never try and catch lows but wait till the shorter term trend turns [Eg: Index > 10 day SMA> 20 day SMA]. Fall is generally more swift than the recovery…

There is no one absolute truth in markets! Everything is contextual  This is what I have learnt…

This is what I have learnt…

4 Likes

The Four Pillars of Future Business ~ Megatrends in the Making

“The only function of economic forecasting is to make astrology look respectable” said John Kenneth Galbraith. And he was right. One of the reasons economic forecasting, as well as financial market forecasting, is fraught with such a high degree of risk is because it operates in a complex adaptive system. One small change in one small component somewhere and there could be a large impact in a completely different system in an entirely different place and time.

However, looking at the future does require some amount of understanding of the present, trend-following characteristics and understanding of potential disruptions. With this in mind, I have tried to analyse the major pillars of future business change. Below are the four pillars of my mental framework for the future of businesses:

- China + 1

- Climate Change

- Digital & Tech

- Health & Wellness

A) China + 1:

With the battle lines drawn between China and the Western world, there is a definite possibility of a Cold War 2.0 ensuing in the next few years. Some experts say it is already underway. Global corporations will be forced to de-risk their sourcing and move away from their dependence on China as their sole supplier. Global supply chains may have to reorganise to reduce and remove the domination of a single point of failure.

However, China + 1 is not just reducing dependence on China. It is a complete overhaul of the decades of policy of super-efficient supply chain systems. The just-in-time delivery model is also likely to take a back seat as companies build inventory and build in some slack in their supply lines to take care of unforeseen events.

With increasing automation and the use of technology, manufacturing is also shifting back to developed economies as labour costs start mattering less and less in the overall scheme of things. In addition, we also see a rise of nationalistic fervour across the world and politicians will be more likely to promote companies that create jobs in their countries even at the cost of maximum efficiency.

B) Climate Change:

The 2030 Paris agreement and other such agreements will force countries to regulate agents of climate change and take corrective actions. We have already seen China act on this by banning chemical factories and other highly polluting plants. This is likely to become more of a trend. As more and more developed and slowly developing nations understand the true cost of climate change (increased weather disruptions and natural disasters), they will be forced to take action.

Governments and corporations will have to focus on better sanitation, clean water and clean air. We are already seeing the beginning of this. Increasingly difficult emission norms for automobiles and their resultant switch to cleaner fuel and EVs; large water treatment and desalination plants; efforts towards rainwater harvesting; solar and wind energy adoption and many more such initiatives are picking up across the world.

We are also seeing a thrust towards biodegradable products, banning of plastic use, recycling of products including the right to repair (something new for the developed world which we have been doing forever!!) .

C) Digital & Tech:

What can I say about this that has not been talked about already by everyone? Technology has become ubiquitous in our lives. Online classes for students, mobile games, the rise of esports, 101 apps for every conceivable activity are now a part of our lives.

Next is the Metaverse. You may be able to travel to Alaska without ever leaving your sofa, or do your online shopping by walking through the virtual store and pick products, just with a VR set.

Companies will increasingly be dependent on tech to not only move ahead of their competition but just to survive! The better a company is at using tech, the more competitive it will be.

D) Health & Wellness:

Sitting indoors due to a pandemic, people across the world seemed to have realised the value of health and wellness. People and governments across the world have fallen short in managing the pandemic and the scars of this will take a very long period to heal. So, there is likely to be increased focus on healthcare spending across the board - governments, corporates and households.

The entire spectrum of health and wellness - diagnostics, online consultations, e-pharmacies, online health records, medical insurance, preventive health care will fall in this ambit. Mental health has emerged as a subject that people have openly started discussing and it is likely that a lot more focus will be in this area as well. Companies in these areas would definitely have a tailwind for the next few decades.

Companies will get both positively and negatively impacted by one or more of the four pillars. Business strategy will require thought and investments in these four pillars. As investors, we need to evaluate how one or more of these four pillars affect the business that we own and how they are addressing these issues as corporates.

This article first appeared in The Economic Times

31 Likes

DOUBT IS GOOD.

“Doubt goes with me everywhere - to the arena, to the practice range, it’s there when I awake and when I sleep. Doubt is my enemy because it unnerves me, makes me overthink, but it’s also, in some weird way, my friend because it helps me become a sharper shooter.” ~ Abhinav Bindra.

The future is uncertain

Investing is based on what will happen in the future. The future is inherently uncertain and probabilistic. It can never be known with certainty. The most that people can do is to forecast based on their knowledge and pattern recognition abilities. Their knowledge, in turn, is based on their past experiences. Someone who has lost a lot of money in the stock market in the past is likely to see investing with a very different tinted lens from someone who has amassed a lot of wealth from it.

When you are investing there are so many questions that crop up. Is the market overvalued now? Should I wait for some time before investing? Is this company that I am investing in going to give me good returns? Is the price going to crash after I buy? It is already up so much, should I chase the price? It is down from previous highs, should I buy now? How will the US taper affect the Indian markets? Why are there no brokerage reports on this company? Is it a fraud? Do I know enough about the company? The industry has a major tailwind, so should all the stocks in this sector do well?

The questions go on and on…

And unfortunately, there are no definitive answers.

When I started investing, I used to feel that this doubt that I always have must be because I am not very knowledgeable. The more I know the less doubt I will get. But in reality, it turned out exactly the opposite. The more I learn and practice, the more doubts I get. And the root cause is simple - the future is unknowable.

Doubt is good

All the great investors I have been lucky to interact with are very doubtful about their picks. Rarely have I seen someone to be very sure. Even after holding a stock for many years, there are some niggling doubts that persist. Should I hold on? Should I add to my position? Should I sell and book profits? Should I sell partially?

Doubt comes mainly from three sources - macro concerns, stock-specific issues and our own past track record of investments, usually recent ones. And no amount of studying or interacting with management or channel checks can help you in removing your doubt. I have seen so many cases where even the management deludes themselves, perhaps unknowingly, about the future prospects of the business. It just goes to reiterate the basic point that the future is unknowable.

I have seen investor friends sitting on the sidelines with cash since 2017 citing the fact that the markets were overvalued or large macro investors taking large cash calls because a certain index level has been surpassed. Market timing in the face of an uncertain future adds a layer of complexity to the process (and is mostly wrong!!).

Using a Quant mindset to develop an end-to-end process

Then what is the way out? One simple way is to have a well-defined process. I have been a process-driven investor for most of the twenty odd years I have been at it. But my process was limited to a checklist, although it was quite extensive. That is what I got from reading a lot from the processes of great value investors. Then I chanced upon quantitative systems and investing. From there I picked up the notion that the process needs to be all-encompassing. It has to start from the universe selection. This simply means which stocks I will research and keep tabs on. Buffett calls it the circle of competence. Quants call it universe selection :-) It is the same thing.

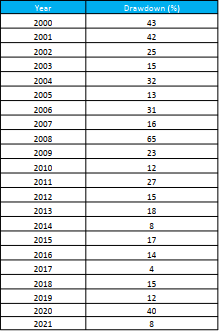

The next is what stock to buy. 99% of the focus on investors are in this. Here you should be clear what time frame you are looking for investing, what is your risk appetite, how much drawdown can you withstand etc. Your fundamental or technical checklist fits in this step.

The next step is the most ignored or least thought through. It is about position management. You need a process for adding more or reducing your positions. This should not be a knee jerk reaction but a result of a thought-through process.

The next step is the sell decision. Again, having a well thought-through process is very important.

The last step, which is something I have never seen talked about by anyone, is should you retain the stock in your watchlist. There are pros and cons to it and it is also dependent on why you bought and subsequently sold the stock.

Doubt is good. It helps you focus on your process. In investing, you will never get it right all the time. You need to get probability on your side. And that’s where having a well-defined process helps.

This article first appeared on CNBCTV18.

24 Likes

please elaborate on the sell decision in the quant method.

Firstly, if you have followed / read the thread from the beginning you will realise that there is no “the quant method”. Quant is a way of defining your factors for investment in a numerical manner.

So, just as you have hundreds of ways of defining your numerical system to get in (buy), you will have an equal number of ways of getting out (selling).

For example, if you are using a quant method to buy high dividend yield stocks, your sell decision may be dependent on either one stock or the entire portfolio goes below your defined dividend yield threshold. Another common method for selling is time-based. You decide as a strategy to hold the stocks for a certain period (say 1 year) and then reshuffle after that period.

5 Likes

Sir,

I have a philosophical viewpoint. Prima facie, biases and emotions are an endless loop- somewhat like 10 heads of Ravana, making thoughts go haywire Emotions play a big part in ruining investment returns. Quant system eliminates emotions and human biases. Thats the first major- major benefit.

Obviously the logic behind quant strategy, back testing , quant factors etc do have their share of importance in boosting returns for which expert advisors like you are the best guide.

Let me know what’s your thought on this.

2 Likes

You are spot on. Behavioral challenges are the most difficult to overcome as an investor, no matter how experienced. But having a rules based system helps in bypassing most (not all) of your biases.

The reason I say most is because some of your deep seated biases will most likely deep through into your system design … For example, because of my long term investment mindset, I can’t seem to work on very short term strategies.

I know so many experienced investors make a mess of market timing that it amazes me as to why more people don’t use a simple rules based system where they will be right more times than wrong and over a lifetime of making investment decisions that’s a fantastic edge to have.

9 Likes

@basumallick I keep reading this thread for some time and it is really knowledgeable, thanks for sharing great wisdom.

Rule-based investment - Should an Investor follow the basic guideline which should act as a boundary. For me, if I say I will invest in only Nifty 500 Stocks that is a guideline but if we go overboard and start building rules for all along system become very rigid with no risk-taking edge. Minimize the universe of choice for a decision so you concentrate on your precious bring a time for finding good decision in your accepted universe.

A programable system helps to automate strategy one want to apply - program too can have logical bise based on the creator but we could minimize the flickering mind relate to change of decision and you don’t need to keep hooked up in the system all the time to watch and make call buy and sell.

If I understand correctly there is no shortcut for the old school approach of deep research for stocks or strategy before one could apply it in the real system. Appreciate your input if I missing something.

1 Like

Please go through the Quant thread for a better understanding of what a quant system comprises of. It is not just about universe selection. Universe selection is just one step. All steps of investing / trading can be quantified and systemised. The fundamental research of non-quantifiable nature like management quality and business quality are substituted by using some numerical proxy.

This is a complete misunderstanding. The paradigm of a quant system is that it actually can replace fundamental research completely. Whether as an investor one can follow such a system is up to to an individual, but if you have a well tested robust quant system, then fundamental research is superfluous.

Hello Abhishek sir, I am not sure whether we can use this place to ask questions but I will try my luck.

I was looking for resources on understanding the importance of independent thinking in investing. If you have come across some good material then please recommend.

I have started to notice that recently I have been getting bias towards ideas which people I respect own. Discussing ideas can be helpful and it helps in idea generation but when would one become aware that they have started to become bias?

I know being free of biases is not possible for a human but looking for suggestions to reduce to till a certain extend.

1 Like

I guess, I can reply as I feel I can share a thing or two that pertain to your questions.

Independent thinking is not an uncommon practice for us, we all have our tastes, which some times are so unique. So it is not hard for us to cultivate our own thinking even in investing, particularly when there are abundant investment avenues available to explore.

Regarding biases, there is knowledge and then there is truth, different things.

Seeking knowledge is a lifelong endeavor. We keep on learning new things. One is good at FA, one could start learning TA. Understood what happened in the company, in the last FY from the AR, there are other ARs to look into.

Truth is not an endeavor, it is a state of mind. One that can be attained in one moment, or one that takes a great deal of practice, a lifetime for some, yet not attained, because of denial. Unless we are truthful to ourselves, we cannot get rid of biases. To get inspired, to gain vicarious experience is necessary but we should get rid of biases.

To give a live example, I got a trading idea from VP yesterday and I checked some charts, understood a thing or two, bought a few shares today morning, wanted to take a position but didn’t because I couldn’t, I did not have the conviction. I thought of preparing a note, did not do it, so couldn’t take the bet. Had I prepared such a note, had I made such an effort to make the idea my own, I would have happily taken the bet, I would have thanked the person who I took the idea from. Would I feel sad if this becomes a 25% profitable trade in a month, no. Am I at peace for letting it go because I did not feel convinced, yes I am. That is the beauty of truth, no dilution, just purity.

These behavioral, character traits, also play a role in not just an investor’s journey but they score high with managements too. Why does the street believe some management? Why does it give premium to some businesses, apart from the business related reasons, there is this aspect of untainted image that one has built over the course of decades. I know some may say, not everything is not black or white, but until proven otherwise, I would say yes there could be such thing as integrity in Indian companies, which demands a premium.

Becoming free of biases is entirely possible, for some it takes years of practice, for some it could be attained by a revelation. I am surprised when members who understand a business so well, say they are biased because they are invested. One could be hopeful, one could be optimistic, or one could even be certain, but one cannot be biased. Like Keynes said - when facts change I change my mind.

I cannot name any material or book, but from what little I know, I can say that there are instances in history where one particular incident, one particular moment changed a man’s life and made him the person as we know him today. Such men have attained a state of being which made them choose a path and not discard that path in rain or shine. Buddha, Ashoka, Gandhi come to mind right way. One cannot wish and wait for such an incident, such a revelation, such a life changing incident to happen in his life but one could definitely start at any point and practice till he reaches his desired state.

Sometimes people are focused on learning new things, that they forget they already know so much but are failing to just implement, practice. Like Munger said - take a small thing and be serious about it.

Knowledge is unlimited, one cannot possibly learn everything because human life in every sense and meaning is limited, but truth is like a feather, one that could be blown away without lifting a finger, but until one gets rid of the denial, unless one accepts, admits, that feather remains as a huge mountain, bothering, pulling back, becoming a headwind.

Hope I did not digress or pollute the thread.

21 Likes