After doing a lot of stock screening over the past few years, i have come to the conclusion that one of the most effective ways to find good companies is to use this super simple method on screener.in. Of course not all companies that pop up will be good but it narrows down the universe considerably and in my opinion eliminates a lot of noise (over 93% of the listed universe is eliminated!). In coming to this conclusion i used the following two simple conditions

Does the ensuing screen list the big wealth creators of the last 5 to 10 years? ( page, eicher, symphony etc )

Does the ensuing screen eliminate the wealth destroyers of the last 5 to 10 years? ( unitech, tata steel,suzlon etc)

If the answer to both is a resounding yes, then it should logically follow that the other members of the list are in good company with at least higher chances of winning in the long run. The mental model i am using here is Occams razor. The most likely explanation is the one that makes the fewest assumptions. What assumption could be fewer than “cash from operations / assets >20%”?

I do not agree on point number 2…coz if u see so many wealth destroyers today were once wealth creators…eg is SAIL, SAIL was a part of nifty once in time , now not a part…so if you follow at the point approach to find such things through screens then it may be wrong also as nobody can see the futures…investment runs on thesis & probabilities…

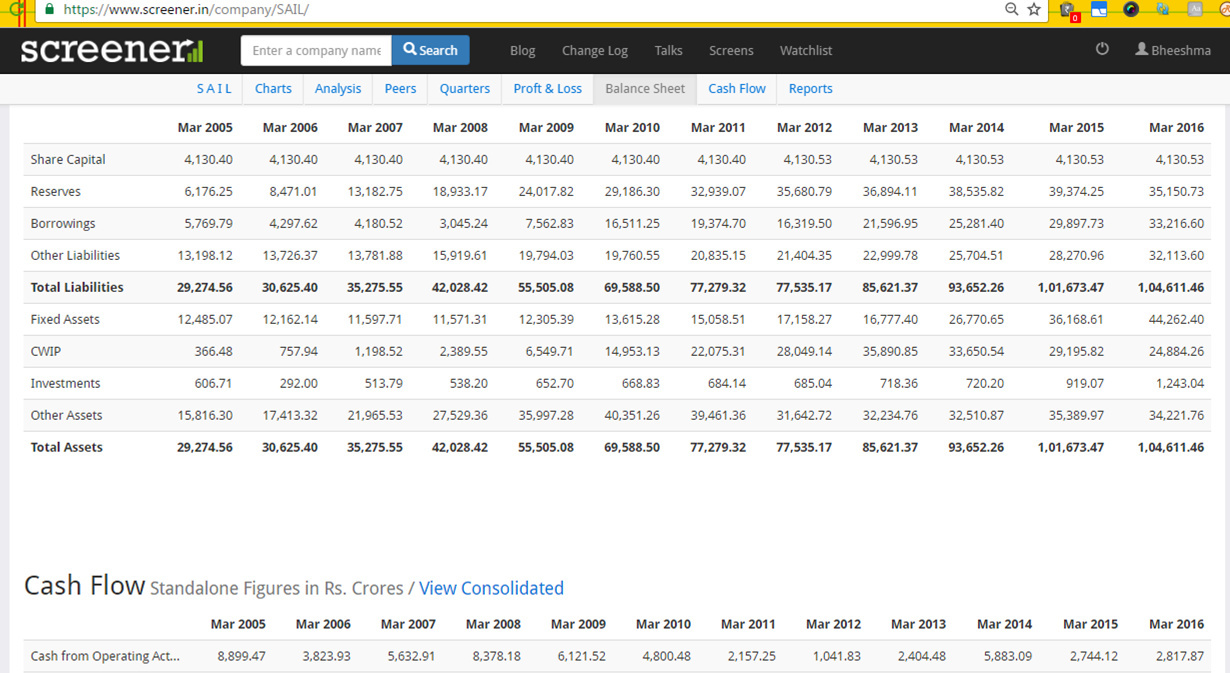

the last time this Screener would have picked sail up as potential candidate would have been in 2005. Since then cash from operations has never been more than 20% of its assets. Check it out.

I know that i am fantasizing ( hindsight bias notwithstanding) but you could have picked symphony up in 2008…

and with a little bit of financial understanding ( removing investments and cash in your calculations) you could also have been long eicher motors in 2009… just saying

Here is my side of story, if I ponder over what you are saying is “Cash

Flow from Operations”> 20% of total assets

It’s a popular ratio for budgeting process as it gives some estimation of

when cash will be available. It’s similar to Return on Assets, then we are

talking about efficiency. The mute question for now would be can we ignore

profitability, financial leverage etc?

Let’s take a reverse direction, is it possible for a company which has

reported net loss with a positive cash flow operations? Of course yes,

initial years due to high capital expenditure depreciation and interest

could be high. Question is would a high capex and high leverage translates

to future earnings engine? May be yes or no. As a matter fact while I was

digging 125 performers of last decade there were very few who were

leveraged.

Straight direction now- profit on books and negative cash flow from

operations. A prolonged cash conversion cycle may create a negative cash

flow but not necessarily a dud company.

Fair, let’s use Cash flow from Ops to total assets as successful ratio for

potential ratio. Then why is this working? When does it work?

In my opinion it may work for companies a. with a high inventory base and

efficient cash conversion cycle. b. lower tangible asset base company c.

company with little obligations or liabilities. High margins, pricing power

I couldn’t correlate directly to cash/assets ratio.

Ok, what happens to plastic and textiles industries. Lets check some

performers from there:

Mayur uniquoters- even with stellar 112 bagger Cash/assets is 10-12%.

Earnings has jumped 43 times in last ten years. Why such imbalance then?

Cash conversion cycle is 90 days, its not low but that’s the more or less

norm of that industry. Check their working capital to sales ratio, it will

just fly.

Indo count- another 55-60 bagger. even in best of years cash/total

assets is 16%. Whopping 115 days of cash conversion cycle days.

Why did Symphony work? 1 month cash conversion, low financial leverage all

adding to a modest total assets.

In short, you would miss those companies who where there is a loss but cash

from ops is positive. Depending on situation they can be bad or good. And

that may include a big chunk of inventory based companies as well.

Companies taking out big dividends also will struggle with this number.

yes you would miss those. you are right about that. what i do for textile companies is use operating profit/assets ( net of cash and investments). Using that you would have gotten into uniquoters in 2010 and into indo in 2015. Over time i guess one develops a judgement about which one to use where looking at working cap cycles. However as a sanity check on the health of the company i find it very useful and in many cases it does a great job of finding good businesses

Thanks for the starting interesting post. You initially started with wealth creator and destroyer over the period of 5 to 10 years. but your search criteria is only meant for one financial year. Don’t we get wrong result. There are companies which cook their numbers to show different result on one or two years. But the same cannot be done for 5 to 10 years period. Is there anyway to apply your logic for period of 5 years.

This is meant to be a filter to quickly identify promising companies based on the current year results. However you can do this for each year going back as far as you want. In an overwhelming majority of the cases you will find that companies with significant upside started demonstrating super cash flows relative to their assets much much before the share prices moved up significantly. You can try this out with your favorite companies and post the results here!

Just export the company data into excel and you can easily calculate the “cash from ops/total assets” for any company going back as far as you want. Sometimes companies have a negative profit but show positive cash flows. That doesn’t mean its a bad company - for e.g Tata Steel. You will need to dig in to find why that is so. However, please keep in mind that the lifeblood of a company is the cash that flows through it. Great companies usually have assets that generate a lot of it

@bheeshma

I tried to follow your advice for GM Breweries. Please correct me whether my formula is correct to get 5 years period of CFO/TA GMBreweries.xlsx (35.7 KB)

Yup thats correct. GMB also has a lot of cash and investments so you may want to exclude that from the total assets but its cool if you dont after all they arent giving it back to the shareholders

@bheeshma sir, I am working on screening good companies from microcap sector. It would be really helpful if you can correct any parameters/data or add any suggestion to better refine the search process.

Market Capitalization <1000 AND

Sales growth 3Years >0 AND

Average return on equity 3Years >15% and

Debt 3Years back > Debt AND

Debt to equity <1.5 AND

Profit growth 3Years >0 AND

Cash from operations last year >0 AND

Current ratio >2 AND

Interest Coverage >4

Some great companies have payables far more than receivables. Negative working cap in these cases is a low cost source of funding. So i would try and run this without the current ratio and see what comes up.