Dear @pradip.

Someone’s gut feeling. No Sir, I have tried last year to say many times this is not the valuations to buy small and micro caps. I learnt that not many pay heed, because, most don’t want to hear the truth, they just want to hear positive words of hope, and words that stocks will work out for them irrespective of at what price they are bought. The truth is uncomfortable, so lets bury our head in the sand is the general approach.

So, what I have been trying to learn from last nearly two years is the “fact” of how stock markets work and not my “wish” of how stock markets should work. I am sure I do not know what it is exactly, but that is my quest. I have no interest in prophecy but it is in me trying to become more and more rational.

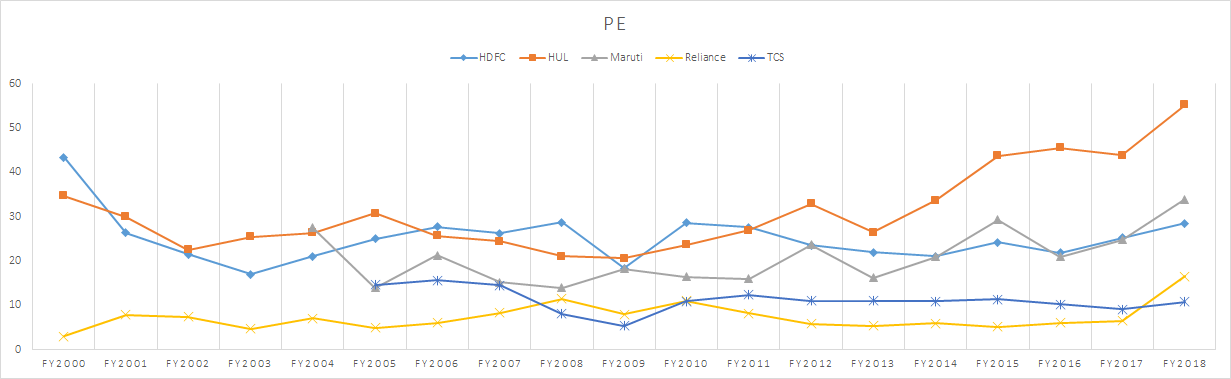

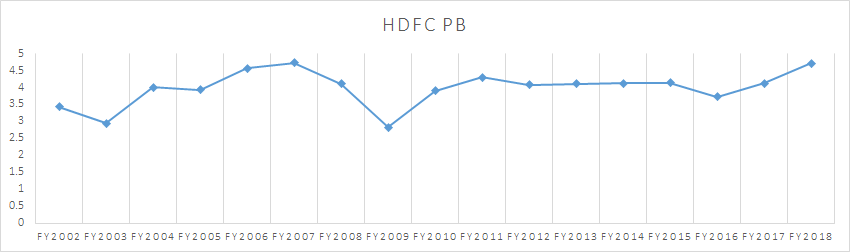

I am looking at data points and then trying to come to a conclusion on a. where we are and b. where are we likely to go if we know where we are.

Thanks to @deevee for having posted much of the sensible data so I do not need to mention it.

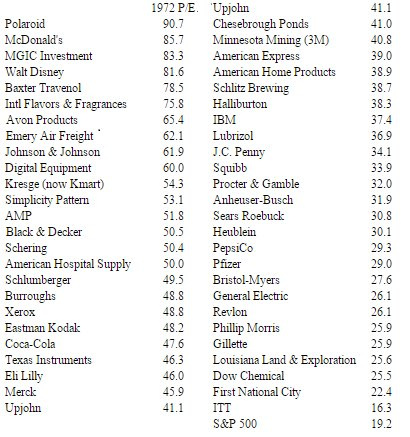

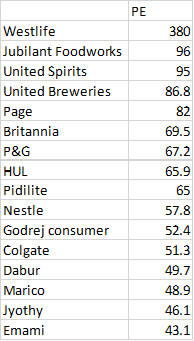

To add to it, I will attach an an excel by the brilliant Anil Kumar Tulsiram. He has done tremendous work. It has a world of knowledge in one excel, but one could use it to simply compare the earning ratios to 2007 to 2018. The file is dated April 2018 so some stock prices have changed. Have a look at Dec 2007 PE and Latest PE.

EDIT: Please treat the attached excel with a pinch of salt. Mod has pointed out that some data has probably not been entered properly and is standalone instead of consolidated. Kindly update before you use the excel.

If you want the full file please go to https://t.co/qjAnpP7Z1z

Also, Lets try a sensible thinking approach which does not need excel. Colgate Palmolive is the example. Apply this logic to most stocks. Net Profit: 673.37 Cr. Market Cap: 33,900 Crore. So, you pay 33000 Crore today, to buy a profit of 673 Crore. If you put 33,000 Crore in the bank FD, you will get 2310 Crore as interest in 12 months. Does it make sense to buy at such market caps? But it seems that it does to a whole bunch of people

Anyhow, there is no point in explaining further to those who will chose to pay any price for a good stock so to them, I wish them good luck. They will need it.