What about the paper stocks in this carnage? Anyone tracking the fundamentals there still?

This correction looks really scary. This do not look like a bull market correction. Though I do not know TA, this seems the end of our six year bull market. We may be heading for one-two year long bear market. I may be wrong. But watching market since 2001, this seems very likely.

1 Like

On first look, fundamentals seem to stay intact in the turmoil. Yesterday visited a paper distributor and as per him, prices are still rising and there is scarcity on the ground, which is a bullish sign.

On a side note, have seen many time the market fall after RBI rate hike. But this is the first time, saw the market fall because RBI did not hike the rates… ![]()

1 Like

I have seen two blood bath 2000 and 2008 … These can be brutal

Lets take favourite sector of 2008 which was infra and Real estate … Unitech was profiled by MOSL as one of big wealth creator in their wealth creation studies …

It fell from Rs 516 to Rs 28 in one year … and today it is @ Rs 2 .

Same happened with lot of infra companies , some of which have filed for bankruptcy . Typically in such bloodbath 70 % + of stocks in favourite sector disappear and never reach their old valuation , 20% ++ stocks linger and give below FD returns and < 10% of stocks do really well . Also often new leaders emerge in that sector …

Worst fall in Indian history is very difficult to say as Indian market history is not well documented . But couple of Big shocks were in 1970s ( emergency and nationalisation ) , 1990s ( when India had to pledge its gold with bank of england) . Today relatively we are better placed …

Current market has just started falling … it may take up till Mar / may 2018 to stablised . So if you have money to invest ( say X ) divide it by 100 … and invest that amount X/100 daily in market till May 2019 .

7 Likes

It looks to me like RBI has decided to leave the Rupee to find its own level. I sort of agree with that. Why give an easy exit to the FIIs? A rate hike would have propped the rupee and would have helped the FIIs exit better. What has happened I think is that the holding of rates signalled RBIs intention to not bother with the rupee but solely with inflation which according to them is within control. This obviously will spook the FIIs who will try to exit quickly before the Rupee falls further. A bulk of the selling today understandably has come from FIIs who have sold 3370 Cr. I don’t remember seeing such a high number for a day before (or for a week).

I think the biggest winner in all this is IT - Rupee falling further is good news for them. Rate hold is also a good news for them as it will help the interest in equities gravitate towards this sector so I think multiple things are working in favour of IT at this point.

Since I made the mistake of discussing macros, let me balance it with some micro.

In that vein, I really like the current valuation for Sasken. Last 10Y FCF is about 1000 Cr. They have a cash of about 500 Cr in the BS. At a market cap of 1350 Cr, it looks to be a safe bet. If you remove the cash, it is trading at a P/E of 9. It is trading at a P/B of about 2 and has zero debt. Management has given some lofty targets for 2022 but there is some ways to go although they do appear very honest and shareholder friendly (looking and dividend and buyback history). I think about 60-70% of revenue is from US/EU which should benefit from the rupee depreciation.

Risks are that it could fall further to 700-750 if the current meltdown continues but the valuation appears attractive to me and is probably one of the few quality IT stocks that’s available at cheap valuations. A reason for the cheapness could be that they are not a typical IT services company and haven’t shown blazing growth in the past. Another risk is that its a very illiquid stock - which is an advantage if you have the patience. Yet another risk is the technicals where it has broken 200 DMA on a closing basis today.

Disc: I had Sasken in the portfolio earlier and have added further today.

8 Likes

IT is a good space to be in. But then Sasken with so much cash is giving out only 20% as dividend. What the heck are they doing accumulating cash? I don’t know how to deal with such managements but I will stay away from managements who want to accumulate cash. Cash is best in the hands of the shareholder. My personal view only.

1 Like

its not like that… fact remains that harder and faster the correction equally sharp is the following rally…i’ll just give you a couple of examples from 2001 (since you are watching since 2001)… jan 2004 …5 months and 40% correction on index…may 2006… 40% correction… 2 months… (yup two months)2008 i dont need to tell you  …we also had 2 other 30% corrections in the recent past but not including it as the pace was cool and spread over a few months… all i would say is that if one is in good companies… one need not panic… if you had hedge…not harm is liquidating30% hedge here and adding… one should keep eyes and ears open and analyze all info sanely…if one does that then even a FD investor would find great value in markets today…e.g even in OMCs… yes… i mean it sir.

…we also had 2 other 30% corrections in the recent past but not including it as the pace was cool and spread over a few months… all i would say is that if one is in good companies… one need not panic… if you had hedge…not harm is liquidating30% hedge here and adding… one should keep eyes and ears open and analyze all info sanely…if one does that then even a FD investor would find great value in markets today…e.g even in OMCs… yes… i mean it sir.

1 Like

Monetary Policy Committee has a very specific mandate. Manage inflation and inflation expectations with interest rate. RBI has chosen to stick with that - a very courageous move. It was not the mandate of MPC to fulfill the wishes of certain market participants. Now that both inflation and inflation expectations are heading lower, it would be counter productive on part of RBI to hike rates just because market demands it.

Not only IT, any sector that is export oriented (esp. USD denominated exports) will stand to gain. In the last nine months, INR has depreciated almost 16% against USD. So almost all high end exports (like pharma, IT, specialty chemicals) or exports where India has a country specific edge (like tea and spices) will stand to gain; where as, the benefit would not be as prominent in commodity exports like metals, textiles etc as the currency of our competing countries have depreciated too. Q3 FY19 results may be subdued as positions may be hedged; but Q4FY19 results will be above expectations. Another sector that stands to gain will be Indian producers who compete with imports in domestic market (like paper).

It may hurt some egos (mostly, BJP supporters who see strong currency as a sign of strength) to see the currency depreciated; but ultimately, Indian exports on the long run can remain competitive by either raising productivity or by depreciating currency. As such we don’t have high hopes of productivity improvement, so no other option left except to depreciate the currency.

5 Likes

Please start a thread on Sasken…may be some scuttlebut can be initiated. These companies who are in the background undiscoveref are too good to be true.

2 Likes

Hi Guys,

No doubt the market was overvalued and its still doesn’t look cheap. But this sudden fall is interesting. Not a single dead cat bounce either. Nifty has fallen 12.28% from the peak. (During demonetization it fell 11.73% from the then peak) . In the internet, i see people attributing to various things. 1. NBFC crisis. (But then even other stocks got hit) . 2. Panic selling by retail /margin calls ( But this is too small to make any impact 3. Macro (But its not that it turned bad suddenly) . So i dont think its because of these reasons. Could there be something else going on which we dont know?. I want to hear the views from the experts here. (Other than the overvaluation and macro)

1 Like

Market is valuation to the base and than run of sentiments…Sentiment is negative. Outflow outstrips inflow …imbalance is reflecting in stock market. Absolute value will still hold even if it dips it will bounce once reflected and endorsed by results. Fundamentally India is a yo yo market. If you are long term market player. …nibble in else wait for the right stock rigjt price. Every market fall is a cleansing act to remove dirt from the system with requlators upping their ante hope it give a more ambitious and clean market till the next rise of the titan

Have seen the Bloodbath of 1992,2000,2008 and now. The common factor is the excesses/scams created in the 8-10 year bull cycles.Excesses don’t just get washed away by sudden corrections only but take time. This is a 10 year old bull market and the way it has fallen my worry is that this might take us to much lower levels than anticipated by many. ILFS,now it seems is our Lehman moment. Coming elections and now Govt not interested in Governance but giving out doles for next 8-9 months is a problem.

7 Likes

I used to follow this couple of year ago this was always have been a good business to have but never proven out to be a good stock to hold. Most of their services were given to Nokia and customer concentration was there biggest risk and that is why it has never got the actual valuation it deserved. Though I haven’t followed then in last couple of years . Has that risk now been changed ? Also as a sector the IT & ITES is having a very little room to grow unless it is operating in some Niche area like Tata Elxsi.

Article on present market scenario by capitalmind

5 Likes

Sentiments…they don’t spare the most seasoned investors.

Completely agree that something is rotten in our financial system or in the global market. I will start buying when stalwarts show 50% correction or stabilise at any level. I have seen the fall of 2008 when my PF was down 75% from top but I also saw days when it used to double every six months whenever the recovery started. Only thing is to find out sustainability of earnings and buy at right price. NObody knows the bottom for sure.

4 Likes

Sorry, to clarify:

-

We’re discussing macros and how they impact institutional investors like large asset managers. They may or may not be relevant to value investors. Large market moves are largely not driven by value investors but traders, momentum riders and hedge funds, for whom macros are key - and many of those players make money as well, so whether macros matters to your investment strategy is relative - it is not the value investor’s strategy to follow macros closely. My point is limited to illustrating that market moves can be driven by interest rate changes as large institutional players, mostly foreign ones, react to these by reallocating their portfolios - the rates they refer to are the reserve currency rates.

-

My point on looking at US Fed rates is in so far as we are talking large institutional investors and macros - my personal belief is that market volatility is led by foreign capital inflows and outflows, and these players are so huge that they essentially set the tone for all emerging markets - and their decisions are based on US T bills and the Fed, as it is the primary reserve currency and safe haven. Indian G-secs, as you correctly pointed out, are set at a risk premium to OECD rates. I don’t think we can understand market moves completely when only referencing local policy actions as the primary drivers of those moves (especially tyhe currency) are foreign investors - the recent turmoil has been widespread across emerging markets and has its roots in changing policy stance in the US, and I don’t think its any different for India.

-

Not saying risk premiums are fixed, but refuting the point that they contract because the risk free rate goes up - this is analytically incorrect - market risk premium is defined as a fixed spread above the risk free rate. The spread can change, but this is because the perception of risk changes, not because the risk free rate changes - if I need 5% above the risk free rate to invest in security x as a hurdle, then 5% doesn’t decrease if the risk free rate goes up. It can change if I think security x has become riskier or safer. It is clear that if the safer asset becomes more rewarding, I’ll demand at least the same level of premium as before for an unchanged, riskier asset. Please note this is not data analysis, but just drawing theoretical conclusions from portfolio theory. You can differentiate the equation for the DCF cost of equity by the risk free rate Rf, and noting that Rm is an increasing function of Rf, f(Rf), and see the derivative wrt Rf to be 1 + beta*(f’(Rf) - 1). f’(Rf) => 1 by definition (in simplest terms f(Rf) = Rf + S, where S is the positive markup that is derived from the inherent volatility in the asset). So the derivative is positive as a whole, implying increasing coe i.e. increasing discount rate and lower PV of cash flows, and lower equity valuations.

-

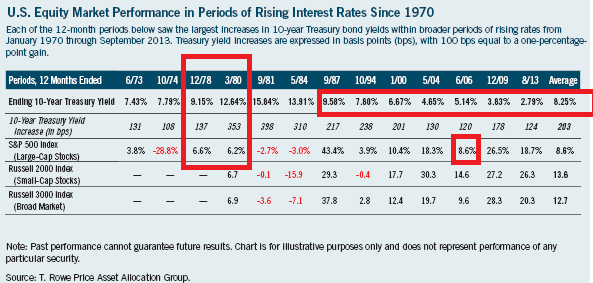

CAPM is theory of course, and does not hold in practice in many instances. Thanks for sharing the article, it is an interesting read, but the article is a little disingenuous with its data - the only place in the data there where equity returns rise is in the years 1978-1980 - and these rises are much below the standard long term return on US indices (about 7%) so cannot draw the conclusion that they increased from the baseline. The only other year is 2006, and the return here is again just about at the long term annual trend. On the contrary, decreasing rates have high correlation to higher than average equity returns.

- Another major conceptual issues with the analysis in that article imo - Monetary policy today is v different from how it was in the 1970s and 1980s which were a v chaotic period. Today forward communication and managing expectations is the key task of monetary policy, so rate hikes which are well communicated and within the inflation target range of the central bank should not worry markets - it is the unexpected change in long term yield expectations that causes volatility and erosion in other asset classes - modern central banks spend a lot of effort in keeping the long term yield expectations unchanged through clear policy communication - I do not reallocate my long term portfolios if my long term risk free return remains unchanged - this concept did not exist in the 1970s and was developed later. If one looks at the data for the last ten years again the thesis is not supported - actually there is no recent data for equity performance in a period of rapid rate hikes simply because it is yet to happen - the point is not a permanent increase in rates, but that long term expectations of the risk free rate undergo flux, leading to reallocations of long term strategies. The second piece of data provided, that equity moves up when yields are < 4 is also not fully representative of the fact that 10Y US treasuries have only been below this level since the advent of the modern monetary system in the late 2000s i.e. the era of quantitative easing and massive monetary stimulus - which as we all know propped up markets world over. So imo cannot read any correlation in this relationship as the market has been factoring in continuing loose liquidity in the face of gradual, well communicated rate hikes - liquidity makes the rate hike a moot point, allocation is easy when you continuously get inflows.

6 Likes

Agreed @phreakv6, looks like RBI is between the devil and deep sea in this case, and has decided financial stability is more important - keeping money markets liquid and getting OMOs done in Oct seems to be top priority. Unfortunately, it also looks like there is significant political pressure to keep optics on rates to prevent a blowup in the money markets and also manage the NPA issue. This does not bode well for inflation - @devaki.tripathy, with oil at $80+ a barrel, higher inflation is on the cards imo whether we like it or not, and several commodity sectors + foreign capital leveraged cos are going to go back into the red - exacerbating the NPA crisis. Imo RBI has kicked the can down the road, and will face a harder choice in a few months if the pressure on the rupee and oil doesn’t abate, as the financial sector issues will only deepen - and if inflation starts picking up rapidly then, it will be v difficult to manage with just monetary policy alone.

1 Like

While I agree with you, I believe this is the time to identify tomorrow’s leaders who can ride this downward cycle and rebound

@vaedermacher

Thanks for the long explanationwity data

If investing in stocks is a business, every business has its loss days when you got to restart

I deleted my posts as people keen on winning the argument than trying to see if there is merit in the post will keep finding fault in your analysis and you wonder what’s in it for you, you don’t want to be a prophet seeker, you want to be a profit seeker

People generally are aware to things they have first hand experience. Like if you are ever hit by lighting and survive, you will be careful when there is lighting. The rest of us won’t care. If you have been pickpocketed, youll always be careful with your wallet in a public place. In the book buffetology, the author says interest rate increases is one of the times Warren picks stocks at bargains but unless you have gone through this once or twice it’s easy to not notice it.

1 Like