Details of yesterday’s transactions.d931d38e-c2b7-4d5f-997e-1e58024455a8(1).pdf (349.0 KB)

1 Like

Disclosure - Acacia Banyan Partners sold some

old news so one should be cautious and think that Why they are selling their businesses

Patents also give rise to litigation

All above are for 3M USA. How does it impact 3M India. I do not see any impact. Pls let us know how you see impact of 3M USA selling these businesses to 3M India?

5 Likes

Listing out some questions for ValuePickrs to ponder about:

- The company is continuously changing CEOs every few years. This can lead to sub-optimal growth as all CEOs may not think the same way. Why is that so? I hope Ramesh Ramadurai is a capital steward and stays with the company for at least five years.

Ajay Nanavati - Upto FY14 (Couldn’t find annual reports before FY10 - so don’t know when he started)

Amit Laroya - FY15 to FY17

Debarati Sen - FY17 to FY19

Ramesh Ramadurai - FY20 onwards

-

Why are the margins falling since past two quarters? During FY12-13-14, it was mainly due to two reasons. A => Rupee depreciation as the share of traded goods as part of inventories was at 45%. B => Poor operating leverage after huge capex during those years. C => Provisions for bad debts. First two reasons are not applicable now as traded goods are 30% of inventories now and rupee didn’t depreciate so badly in last two quarters and also no huge capex recently (I don’t think recent acquisition of 3M Electro should cause this). We should dig further on why margins are being impacted.

-

MNCs tend to hire a lot of workforce in India to cut their costs globally due to availability of cheap labour in India. Hence, all behemoth MNC IT companies are expanding crazily in India over the past few years. We need to be mindful if employees hired in India for global operations are being charged to PnL in Indian subsidiary or the parent company. Good thing is employee costs as percentage of sales is muted since years (in fact decreasing). Another comforting point is 3M is regarded as one of the most ethical companies, so gives confidence that no such practice is going on.

Thanks!

5 Likes

Thanks, but from where do you infer this for 3M India.

It is the global 3M company which is regarded as one of the most ethical company on the globe.

I’ve inferred it for 3M India through the parent-child relation.

1 Like

Thanks for your valueable observation. Find enclosed my understanding on issues mentioned in you message:

-

3M India managment is controlled by 3M Group and hence based on Corporate structure need, the move their employee within group. Since the work culture and ethos are same and strategy level decision are taken at group, I do not see change in employee as major issue. In case top management is replaced due to non-performance then it would be concern. However, most of times, we see CEO MD of India moved to other role in 3M group only. Hence, I think it is typical MNC rotation of management then kind of concern due to non-performance.

-

While point you raised for margin is valid, I generally look at company from ROCE over medium term to assess profitability. This is more relevant in case of Business like 3M which have blend of trading and manufacturing. Many time, with increased domestic prouction, the company may with lower prices in order to improve penetration and achieve scale of production. That may result in (EBITDA/Net) margin deterioration, but ROCE accretive. In case of 3M, what is interesting to note that depiste movement of margin, ROCE has increased from 21% in FY15 to 29% in FY19 (Source: Screener)

https://www.screener.in/company/3MINDIA/ -

Agree on employee cost part with you. However, personally, I never trust any certification from third parties, particualrly when the certificate issuing authority is also in business. While I have limited idea of Ethisphere.com and its activity, in Indian context, certificate issued by same agency to parent company, had disaster equity wealth destruction record.

https://www.ricoh.com/release/2016/0308_1.html

Hence, I belive in philosy of “Suno Sabki, Karo Manki” and Buyers be aware. We can not outsource evaluation of business and managment to third party.

Thanks once again to bring out valid observation which made this thread more useful.

11 Likes

Thanks for your comments Dhiraj bhai.

Related to employee expenses, I could find the below in related party transactions section in the annual report. I believe this is related to the outsourced work in Indian subsidiary.

I hope that the numbers reflected represent the true economic value of the work contributed and the auditors have done their job.

@lingalarahul7

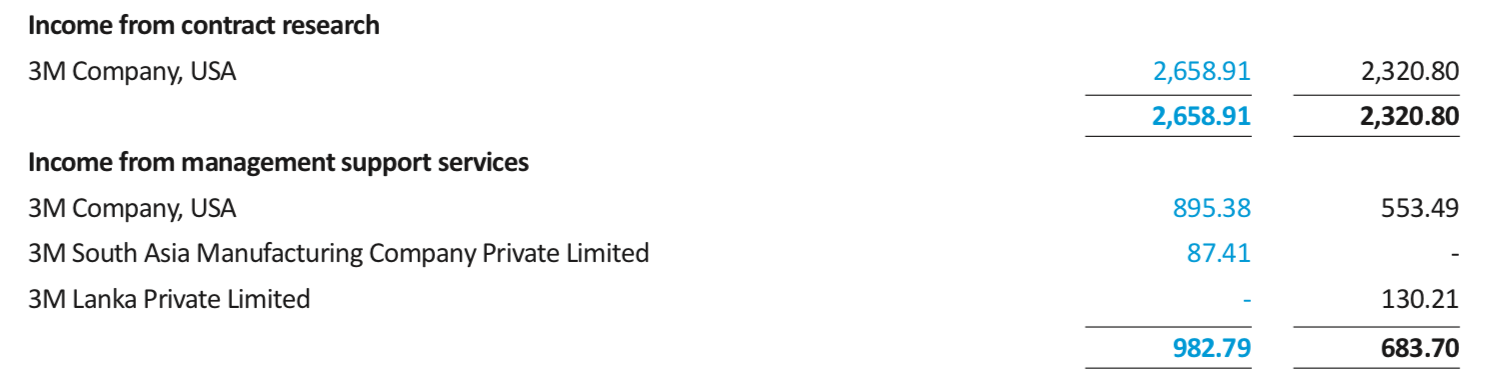

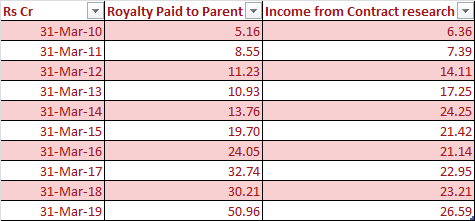

In the first post I did cover about related party transaction.

However, during FY19, there has been significant jump in Royalty payment as compared with Income from Contract research. While not sure, but party it may be due to addition of royalty payment from 3M Electro which was not merged in 3M India till FY18. Having said that, I would still closely evaluate this are development.

Find enclosed Yearwise Contract research income and Royalty payment for 3M India in Rs Cr.

3 Likes

One more thing is the volume of shares traded each day for this stock is very less at about 1000 to 2000 shares. This implies only 2.5 to 5 crores worth shares are traded each day for a 25000 crore company. This can possibly explain (along with other factors) the high PE of the stock.

Another company facing a similar situation is Honeywell Automation.

I initially thought the problem was with the price of the stock but MRF Ltd with a similar market cap and more than double the share price trades about 30 to 40 crores worth shares daily.

Another reason could be high promoter holding at 75%. But Siemens Ltd which also has a 75% holding with market cap of 60000 crores exchanges shares worth 50 crores daily.

May be it is a combination of both i.e. high share price and high promoter holding leading to such low value of shares exchanged each day.

Request people to share their thoughts on the same.

3 Likes

MRF is a very visible consumer company , visible on Kohli’s bat, large advertisement hoardings and Television ads, brands like 3M which are of very different nature and from a Print/Print related item industry are not in your face type visible which leads to much lower trading volumes, same is applicable to Honeywell automation.

In my opinion, it is a combination of all the parameters

- High promoter holding.

- High Stock price.

- Lack of information apart from AR & AGMs. Also, no analyst coverage. (main point IMHO)

- B2B, less visibility brand (as @amanbindra mentioned)

- Fear of de-listing.

3 Likes

Actual results link

3M is apparently affected the most due to US-China trade war which will naturally prompt it to diversify their production base. Hopefully some of it will come to India.

Sluggish performance at the parent level may lead to increase in their focus towards emerging economies.

Looking forward to see if they’ll come up with new business lines at parent level in the current restructuring, whose benefits may be reaped by Indian subsidiary as well in the long run.

Discl: Tracking position

5 Likes

This company is the beneficiary of corona virus issue. IMF has hit the panic button, all central bank coordinating to combat the economic impact and the spread is only increasing with face mask demand surging like rocket. No face mask is available in amazon and whatever is available is selling expensive.

IMF, govt and others are ordering to stock up all the necessary medical equipment to fight the spread.

Disc - Invested

1 Like

When stock is trading at 83 TTM PE, I believe most of positive are already factored in. Also, when one look at first level of analysis, more Corona Virus impact economy, more 3M would suffer as nearly 60-70% sales of 3M in India is from Industrial activity. I doubt improvement in mask sale would made up from negative in industrial slow down. This is my understanding.

The recent increase in share price, in my understanding, has more to do which recent geo-political factors development. World has been getting constant shock of concentration of supply chain in one country. In last 3-4 years, events has shown fragility of concentrated supply chain, to the major Outsourcer, That may have resulted in thought process to diversify supply locations. While I am not sure which region would emerge as beneficiary, I see definite trend in relocation of capacity. Since the capacity would be to service Western world demand, it would require stable technology/capital goods suppliers. I see 3M/Honeywell/Siemens/ABB (along with any other reputed Capital goods player which support manufacturing) as being a major beneficiary in this trend. I see current development as same as Speciliaty chemical in 2014 when China stopped supply which created first level of shock in supply chain and then first level beneficiary where Indian Speciality chemical company and second level was GMM Pfaudler like Capital goods suppliers… This is very very crude subjective assessment and too much simplistic explanation without any data to support and also appear as my wishlist (after investing in Honeywell and 3M at very high valuation, rather than actual assessment). I may be completely wrong in assessment of situation (like in Shemaroo and Care Rating in past) and may reverse my view after two-three years.

While I hold 3M and it is among my Top 6 holdings, in my opinion, increased sale of Mask etc are more of one time and not material to make difference. However, investor sentiment is altogether different and I am may be completely wrong in assessing that.

Discl: Among my Top 6 holding, no recent investment decision in last 3 months, Not sebi registered analyst, Not a recommendation, Investor shall consult his/her own advisor before making investment.

21 Likes

Due to the ongoing COVID-19 situation, we have been buying a lot of 3M products at office.

3M hand rubs and masks are the ones which were available and the most expensive. Though as noted by @dd1474, increased sales of masks and sanitizers are one off, I feel making 3M products available in market when others are sold out shows their agility and of course there may be a slight uptick in sales of sanitary products post COVID too as we become more aware as society.

4 Likes

If you see their Q3 2020 performance,it was pretty bad compared to last qtr and even Q319. Any idea why it was so and the future prospects leaving aside one time growth in sales currently