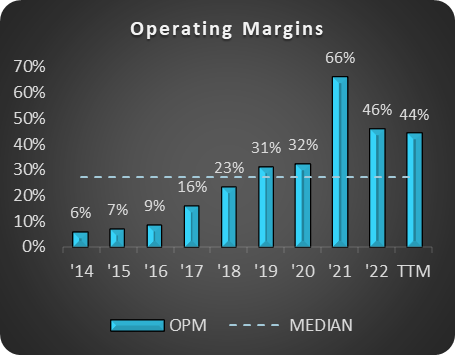

The only question that comes to my mind is about the OPM. What are the steady state margins here? Are the new found levels sustainable?

If one looks at pre-COVID levels the company was between 6% to 30% which was a massive improvement and the share price was rewarded commensurate to this move. Now it is operating in the 40s with the most recent quarter jumping to over 53%, a whole new orbit. A side question to understand this better would be to know why did the margins improve so much?

The spoilsport here could be that margins revert to pre-covid levels of 30s. That will start taking the valuations up and I wonder if the topline growth could be enough to sustain the price.

Their non Covid kit margins were always above 50%. as Covid kits were sold like commodity in later stages due to volume play, it is not comparable.

In starting years consolidated margins were lower due to lower contribution of 3bb… but as company is converting into biotech, it gonna sustain atleast in short term unless there is stiff competition in future.

The margin will always remain higher going forward as you can read from all the management commentary that they are targeting more and more export which has better margin compare to domestic market. So i feel margin is easily substainable.

Further freight cost can easily be saved for european customers and made in UK products can easily be sourced from their subsidiary company.

Both name and investment amount are not available in public domain. Both of these parameters (name/business/products and investment amount) are vital to judge the quality of the acquisition and it’s impact on future earnings. Any information on these two will be appreciated.

I hope funding through “internal accruals” doesn’t means huge erosion in cash and cash equivalents.

Decent set. Covid is now almost completely flushed out from the results. Trading at close to 7 times EV/EBITDA and growing fast. It’s extremely cheap IMO.

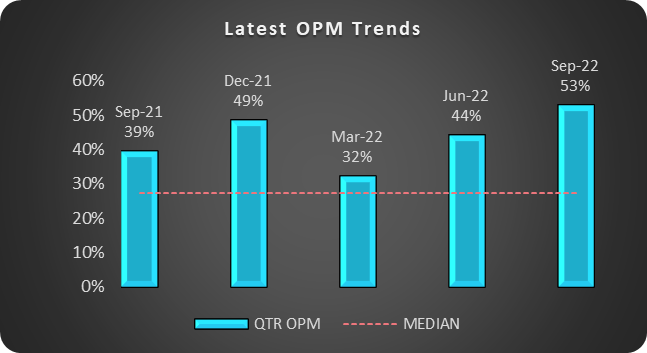

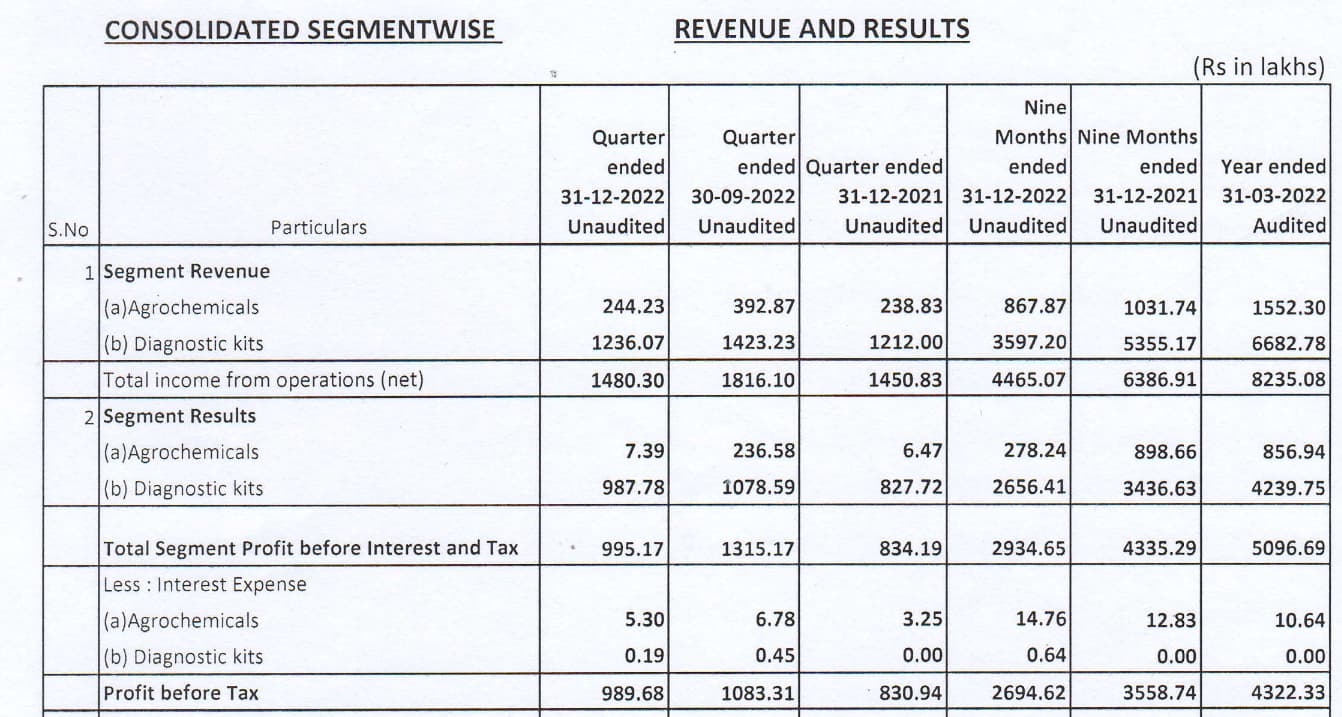

It seems Agrochem side of the business is dragging down the overall margin (vs Q2FY23).

If you look at Diagnostic business in isolation: the PBIT margins have gone up compared to the last quarter (Q2FY23): 987/1236 vs 1078/1423 (let me know if I am missing something)

No point reading much into minor margin fluctuations IMO. The mix is changing and exports are slowly picking up. They moved to a new site as well recently, so there could be operating expenses changes. Plus ofcourse the agro business will fluctuate.

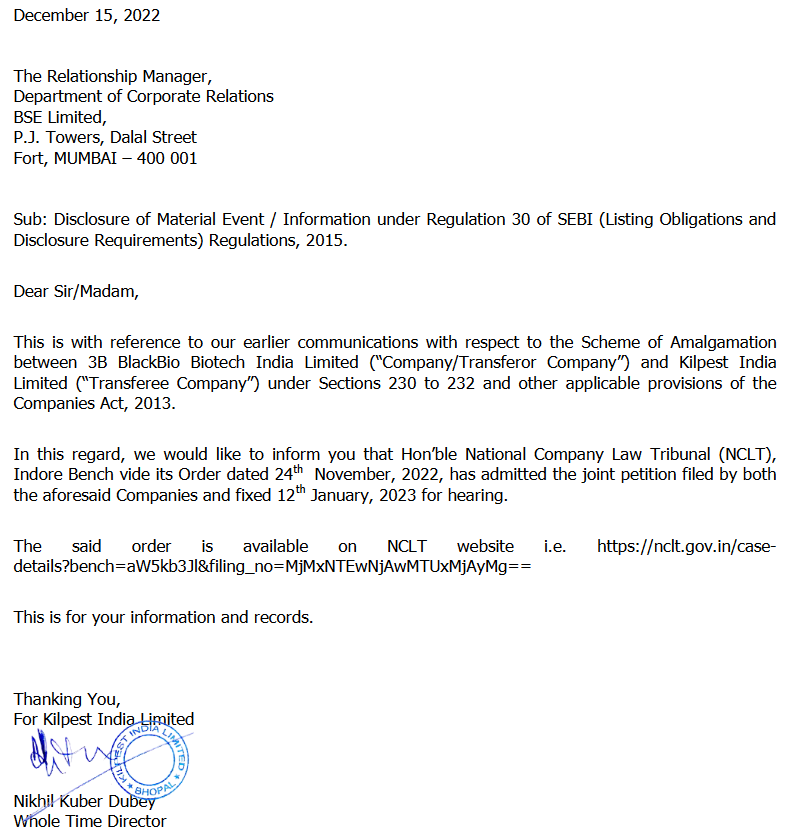

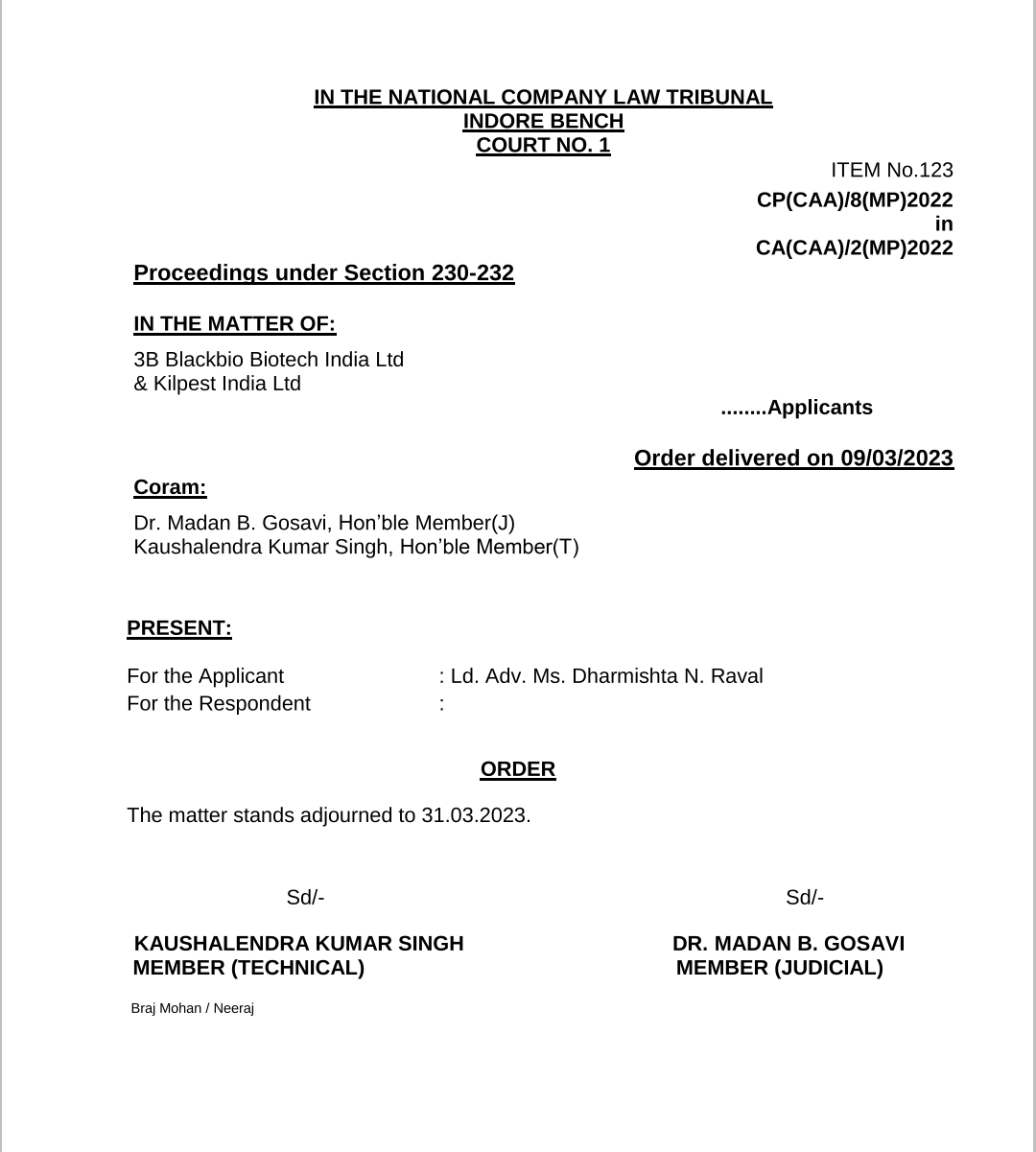

I think it’s been roughly 2 years since kilpest announced Amalgamation with 3B BlackBio Biotech and its 2nd time NCLT adjourning the session, now delayed to March end. Anyone know what is happening here? I am aware our contry’s systems are notoriously slow in these matters, But Kilpest case seem to be much worse.