Now that export restrictions have been removed, perhaps better export figures can be seen in light of increase in infections.

Published: 30th June 2022

Disc: invested

Now that export restrictions have been removed, perhaps better export figures can be seen in light of increase in infections.

Published: 30th June 2022

Disc: invested

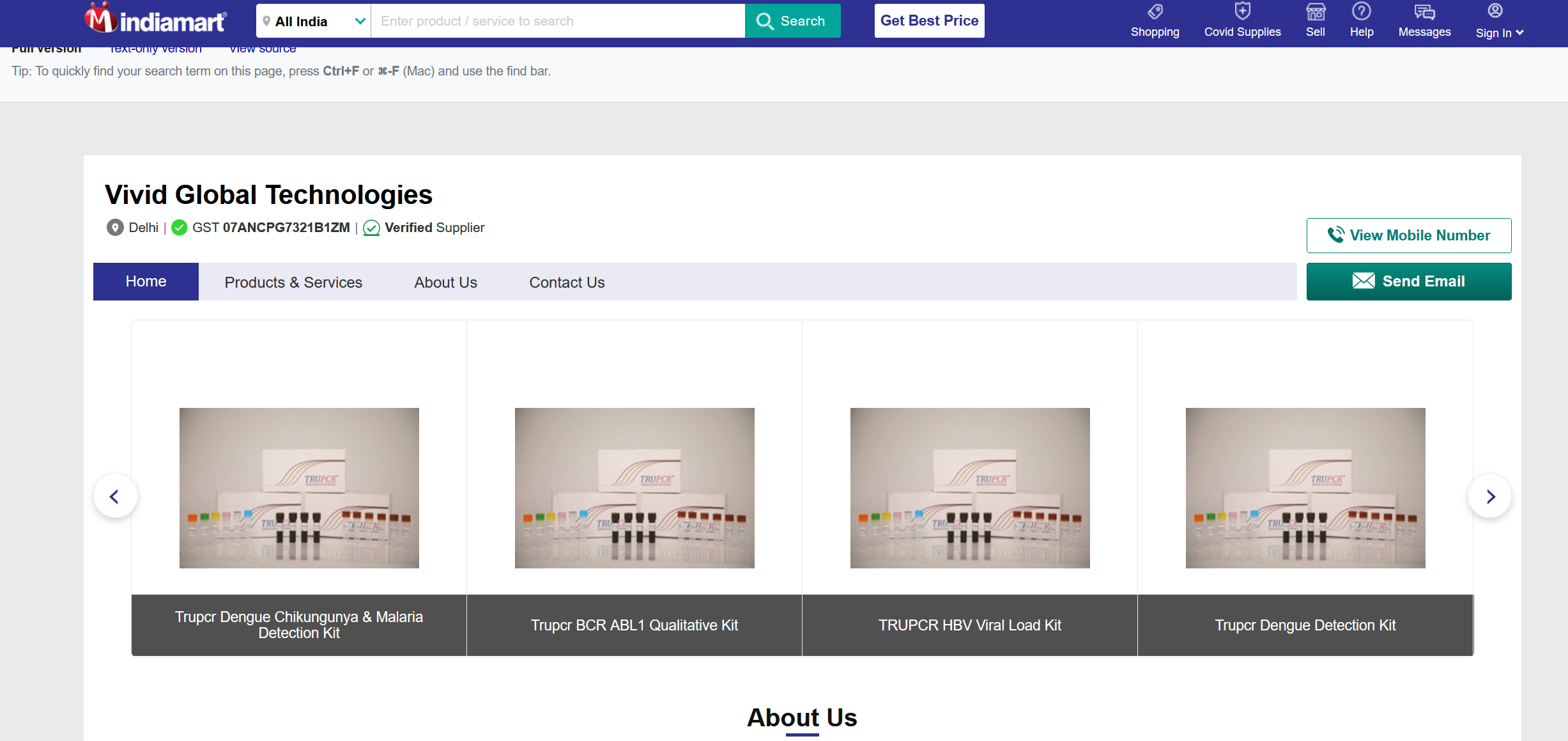

Was trying to look this up up on why the sales were routed through Vivid Global Technologies.

All I can find right now is that they were the supplier for TruPCR kits listed on IndiaMart. This listing did not show the Covid kit but this screenshot is a cached version from Google. Somehow indiamart website is not loading for me right now.

I remember seeing that TruPCR was distributed by other companies on IndiaMart at some point. Some distributor had listed TruRapid before approval was received (if I am not mistaken).

This could be simply that the distribution is normally outsourced and the distributor took a percentage share in the business. I don’t see this as worrying at this point. LinkedIn page of Mr. Prateek Goel says that he founded Vivid Global Tech in 2013 and is currently the ‘Head of Commercial Operations, 3B BlackBio Biotech India Ltd’. So he is a related party with skin in the game, it appears.

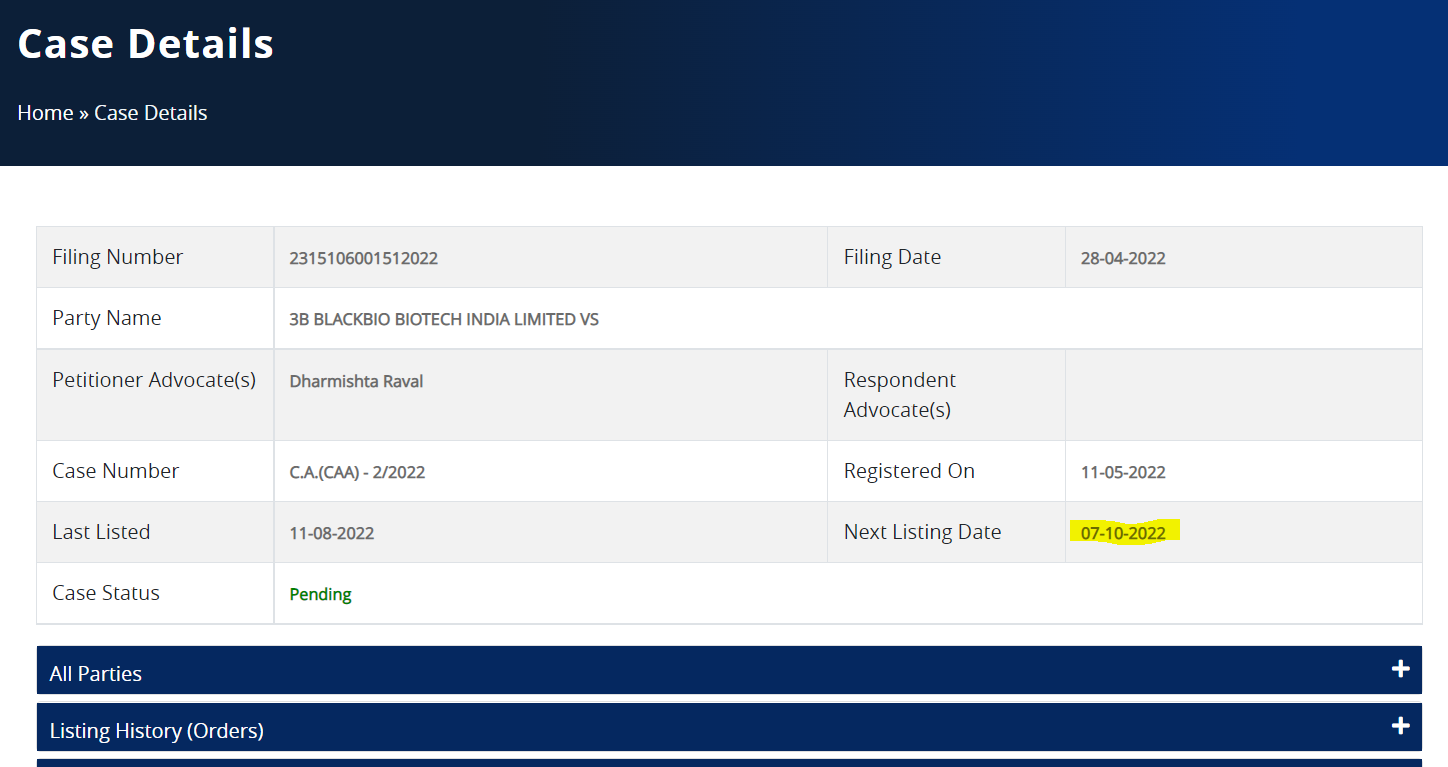

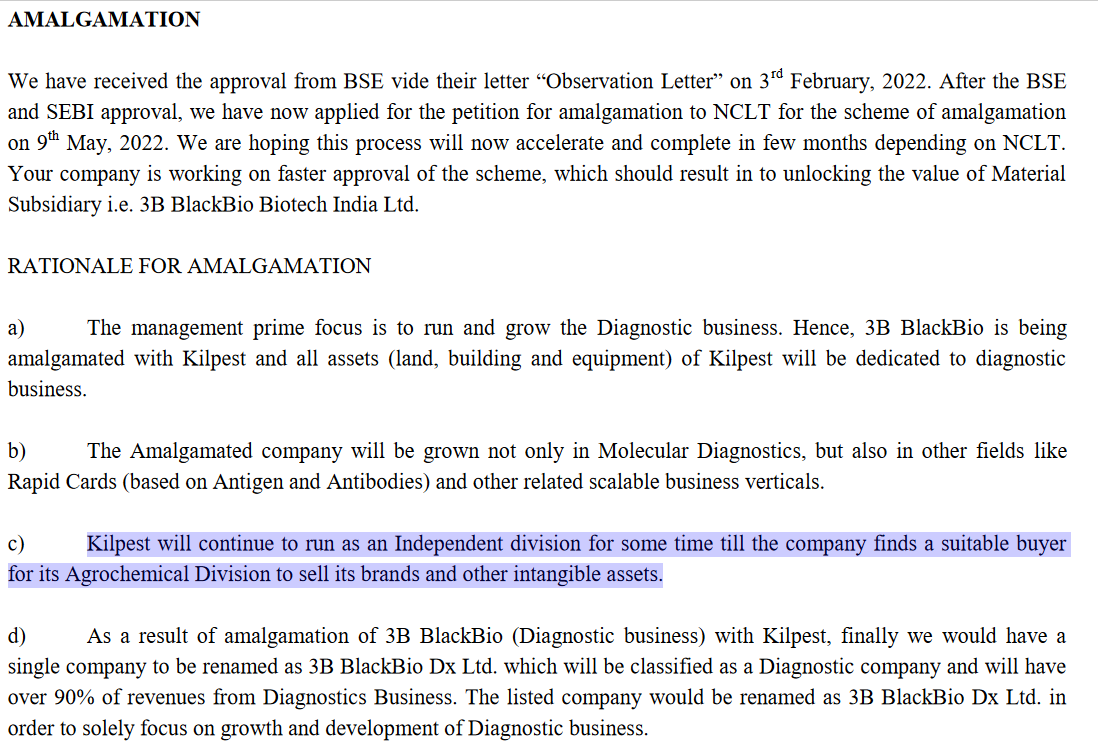

Seems the company was not adequately prepared and has been caught off-guard by the NCLT notification regarding amalgamation (did they engage a good consultant for the amalgamation?):

Is this information available in the public domain, e.g., via the NCLT website? If not, then from the recent stock price movement, can we infer that there is a leak of insider information? I would not like to have a big exposure to a company that leaks information. Therefore, I am interested in the answer to the above question.

Disclosure: Invested.

Looks like it’s there in the public domain…look for attachments under listing history.

https://nclt.gov.in/case-details?bench=aW5kb3Jl&filing_no=MjMxNTEwNjAwMTUxMjAyMg==

It’s very sloppy on Kilpest management part to have missed this, when this is something all shareholders were looking fwd to.

Disc.: invested

Thanks for sharing the order. Nearly 2 years since this small, straightforward merger started. It’s worth reading the order to understand how death by compliance happens via Indian regulators / courts. When an inefficient system meets an inefficient management, shareholders are bound to get screwed.

Kilpest India investor presentation is published and can be accessed through the link provided below.

Excerpts:

I believe a rerating can happen only when they shift their focus into diagnostic care fully and convince the market to stop looking them as an Agri player (minimum contribution to the overall sales figures)

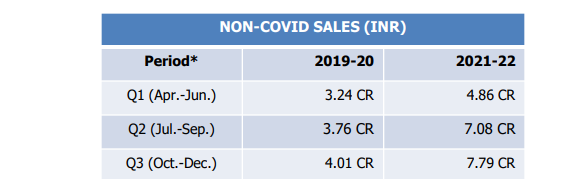

I feel the management is a bit cagey about sharing non Covid sales numbers.

I was trying to ascertain if there has been a sequential QoQ growth in non Covid sales and here is my estimate:

Q1FY23 investor presentation says the non covid sales were 9.42 cr. minus 1.78 cr. which is ~7.6 cr.

Now, Q4FY22 presentation says non covid sales for FY22 were 26.5 cr., which roughly translates to ~6.6 cr. per quarter (though the latter quarters likely had more non covid sales).

So, i am estimating a sequential QoQ growth in the range of 12% to 15%…which is okay i guess?

Requesting more experienced members to provide their commentary on Q1 results (@sahil_vi @kalidasa @vikas_sinha @Vineetjain111)

One big threat to molecular diagnostics is the up-and-coming CRISPR-based diagnostics technology.

While this new tech is not perfect yet but, in my view, it will displace qPCR in a few years.

You can read more about it in this Nature paper here: CRISPR-based diagnostics | Nature Biomedical Engineering

I have posted some content from the paper below –

Abstract

The accurate and timely diagnosis of disease is a prerequisite for efficient therapeutic intervention and epidemiological surveillance. Diagnostics based on the detection of nucleic acids are among the most sensitive and specific, yet most such assays require costly equipment and trained personnel. Recent developments in diagnostic technologies, in particular those leveraging clustered regularly interspaced short palindromic repeats (CRISPR), aim to enable accurate testing at home, at the point of care and in the field. In this Review, we provide a rundown of the rapidly expanding toolbox for CRISPR-based diagnostics, in particular the various assays, preamplification strategies and readouts, and highlight their main applications in the sensing of a wide range of molecular targets relevant to human health.

Main

The fast and accurate diagnosis of a disease is central to effective treatment and to the prevention of long-term sequelae1. Nucleic-acid-based biomarkers associated with disease are essential for diagnostics because DNA and RNA can be amplified from trace amounts, which enables their highly specific detection via the pairing of complementary nucleotides. In fact, nucleic-acid-based diagnostics have become the gold standard for various acute and chronic conditions, especially those caused by infectious diseases2. During infectious-disease outbreaks, as most recently experienced with the coronavirus disease 2019 (COVID-19) pandemic, fast and precise nucleic-acid-based testing is vital for effective disease control3,4. The detection of nucleic acid biomarkers is also critical for agriculture and food safety, for environmental monitoring and in the sensing of biological warfare agents.

Nucleic acid-based diagnostics relying on the quantitative polymerase chain reaction (qPCR) or on sequencing have been widely adopted, and are frequently used in clinical laboratories. The versatility, robustness and sensitivity of PCR have made this technology the most commonly used for the detection of DNA and RNA biomarkers. In fact, PCR is the gold-standard technique for most nucleic-acid-based diagnostics. However, the costs of reagents for PCR are high, and the technique requires sophisticated laboratory equipment and trained personnel. Although isothermal nucleic acid amplification circumvents the need for thermal cyclers, non-specific amplification can result in lower detection specificity6. The specificity can be improved through additional readouts, in particular by fluorescent probes, oligo strand-displacement probes or molecular beacons. However, there is a need for technologies that combine the ease of use and cost efficiency of isothermal amplification with the diagnostic accuracy of PCR. Ideally, such next-generation diagnostics should also have single-nucleotide specificity, which is integral to the detection of mutations conferring resistance against antibiotics or antiviral drugs.

Last year’s total non covid sales were 26.53 Cr. If we take the non covid sales of first 3 quarter, non covid sales in Q4 of FY22 will be 26.53 - (4.86+7.08+7.79) = 6.8 Cr which means a QoQ growth of 12% for this quarter.

It looks like their non covid sales are stuck between 7 to 8 Cr mark which does not inspire confidence in my view.

The number of labs having PCR cycler machines has increased multifold during the Covid times. These labs are potential customers for 3BB. Furthermore, the company is looking to expand its foothold in European markets as well as the middle east. The company has more than Rs 100cr cash for inorganic growth. If things go well, this can lead to exponential growth in revenue over the next few years and can lead to major re-rating.

Tech-disruption risk, due to the newer technologies such as CRISPR diagnostics and Optimal Genome Mapping, is high over the next few years, particularly given huge investments recently in these fields. Several people have expressed similar views in this thread. However, the increased prevalence of PCR machines (due to Covid) will slow down the disruption away from PCR tests.

The NGS tech is less prone to disruption as it works together with the newer technologies. 3BB’s foray into NGS needs to be tracked closely.

The company should invest into the newer techs to ensure continued growth in the long term. As of now, the company is still to reach scale, which will be the focus for the next few years. Scale while maintaining quality will hopefully allow the company to transition into the newer techs in the future.

There is some update in regard to NCLT approval. The Next Listing Date which was earlier 18th Aug has been changed to a new date of 7th Oct’ 2022. So, things got delayed by almost one and half month, but its progressing at least is the good thing.

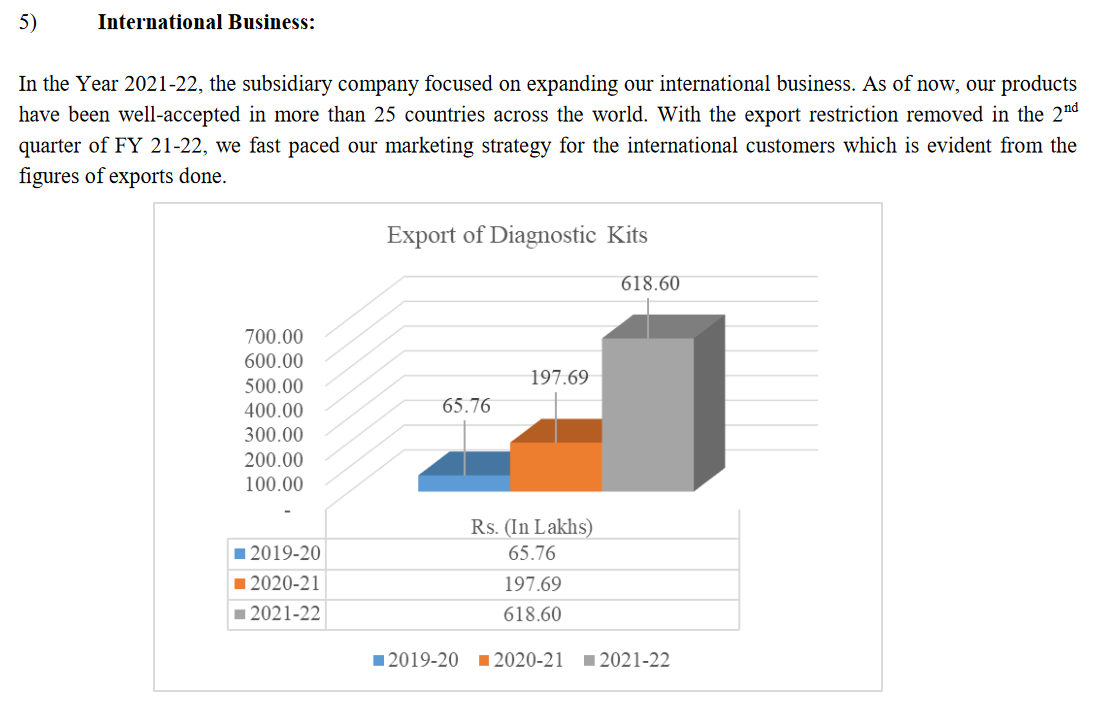

Good development on the export front.

Disc.: invested

Some points I noted from FY22 AR

Export story is building up in a good way

Agrochem business will be hived off eventually (post amalgamation)

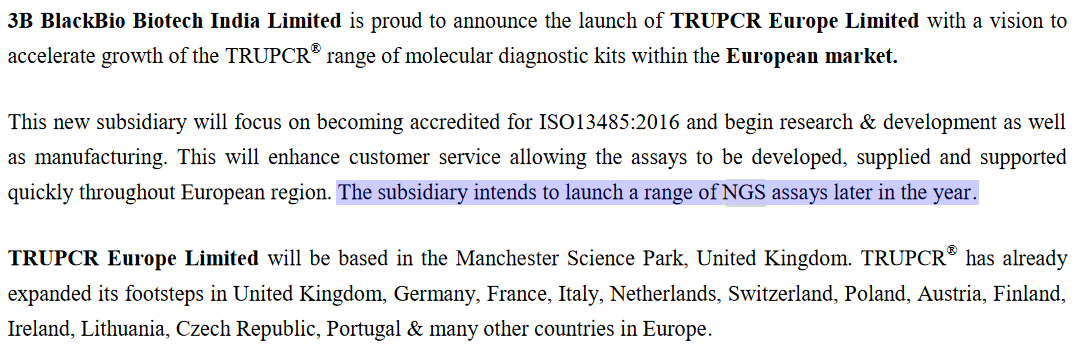

NGS based assays will be launched later this year

Disc: invested

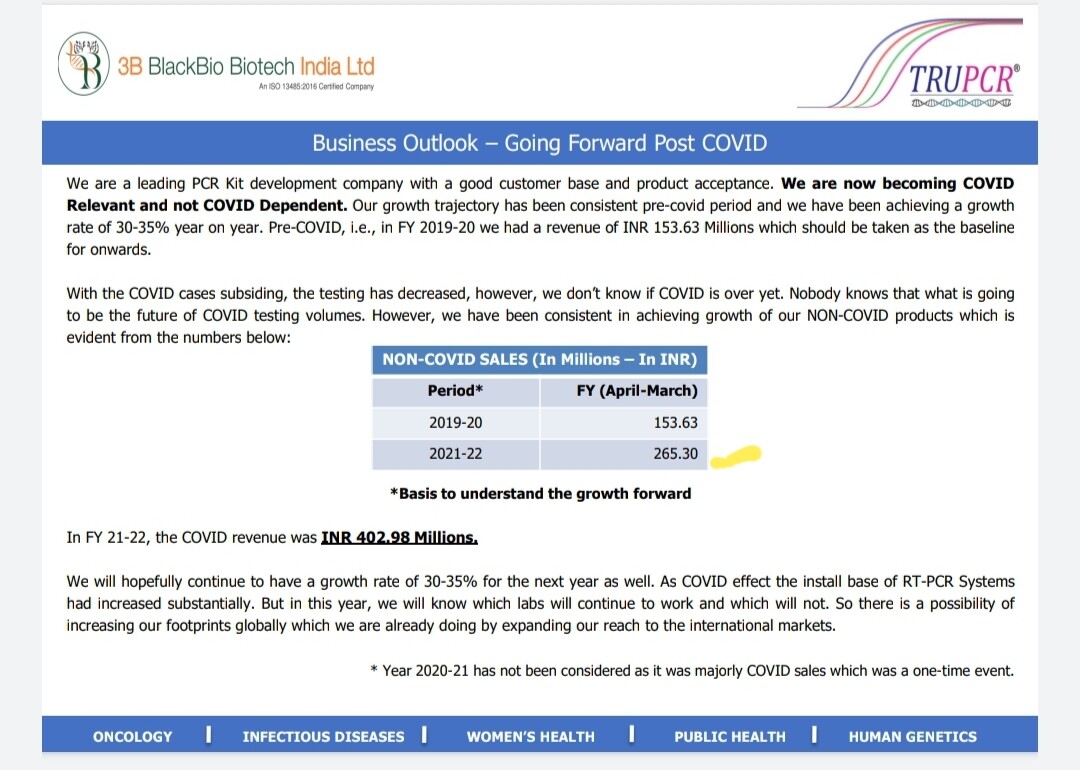

Kilpest investor presentation. There is not much new information provided compared to the previous reports. The only notable information is the increase in exports sales of 61.86M in FY21-22 compared to 19.77M in FY20-21. The non-covid revenue has also gone up by 30% which is a good sign. Again, listing in NSE and reclassification into diagnostic industry can be the only triggers for a rerating of this stock. But we don’t see any clarity from the management on these.

TRUPCR to supply Vela Diagnotics’ NGS workflow solutions

In my view, Vela’s NGS workflow solutions (which is more like the hardware) will complement the NGS-based assays that TRUPCR plans to launch later this year

Disc.: invested

How big is the opportunity and TAM size here?

(I’m not able to get it from the attached link)

I don’t known/couldn’t esimate. Thanks

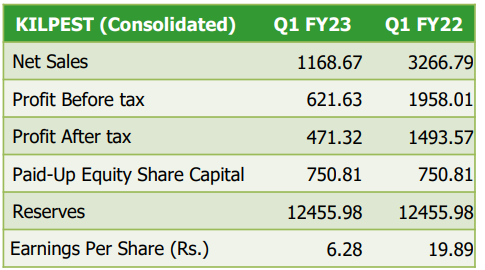

Really solid results in my view. Q2FY23 results prove that there is a lot more to Kilpest than Covid test kits. Continued numbers like these should place the company in the next orbit soon.

Disc.: biased and invested to the teeth

The company has posted a Stellar quarter and half yearly number post covid and grown their core business at 100 percent rate. Here are few highlights of their performance :

“This subsidiary was launched with a vision to accelerate the growth of TRUPCR® range of molecular diagnostic kits within the European market. We would like to mention that the UK subsidiary has successfully faced the BSI Audit for getting the ISO 13485:2016 accreditation. With the subsidiary hopefully getting the certification soon, they will start commercial production in UK itself. This will have following benefits:

A. the “Made in UK” products will have better acceptability especially in Europe and other regions;

B. with products readily available at UK office, the lead time to supply the customer orders will be reduced and the customers will be more confident in “TRUPCR” brand which will eventually lead to increase in revenue.

Although the technical team is in place now, we are working to continuously to increase the sales and marketing team. In the past few months, the UK subsidiary has participated in 3 International Molecular Diagnostic Conferences. With these conferences, the visibility of TRUPCR Europe has increased and we are getting enquiries for providing distributorships and OEM solutions through which we will expand our footprints across Europe. With enhanced visibility and full marketing team in place, the real benefits of the subsidiary will start coming in the next financial year.”

“We have been looking for options to acquire a company in similar business area to get inorganic growth in FY22 and onwards. However, we have not been able to find a suitable company. As due to COVID, most of the lifesciences and molecular diagnostic companies are seeking very high valuations. M&A valuations globally have gone high due to demand from molecular diagnostic companies which are flushed with cash. We will only go for the acquisition if it makes financial sense and meets our internal IRR criteria. We would also be looking at share buyback in FY22/23 post merger, if we are unable to secure a desired acquisition candidate. Our aim is to create maximum value for our shareholders.”

“Rapid Kit manufacturing plant is ready for trial runs & we are optimizing the products in R&D which have market potential, other than COVID Testing Kits. We will start with Dengue NS1, Dengue IGM/IGG to cater to the current season and keep on adding products as and when they are ready from the R&D. We will also be launching some novel products in FY 2022-23 which are under R&D Stage.”

A. Who is growing at 30% CAGR and operating margin of 45 % from last several years

B. High penetration by continuously attending international Molecular Diagnostic Conferences to spread awareness of TRUPCR brand

C. EV of 101 cr and operating cash flow of 27 cr a year

D. High products in pipe line , investment in foreign subsidiary (made in UK), amalgamation been the next triggers

E. High focus on export to get better margin (made in India and sell overseas)

F. Continues focus on signing of long term contract to have stable revenue

G. Varun daga of Girik capital is holding 12 % stake in the company

Kindly note the note was made post the result announcement. Market cap was at 250 cr approx