Doesn’t apply for kits.

“Relaxation has been provided in certain limited cases, including for procurement of medical supplies for containment of coronavirus global pandemic till 31st December 2020,” the statement said.

Disc. Invested

Doesn’t apply for kits.

“Relaxation has been provided in certain limited cases, including for procurement of medical supplies for containment of coronavirus global pandemic till 31st December 2020,” the statement said.

Disc. Invested

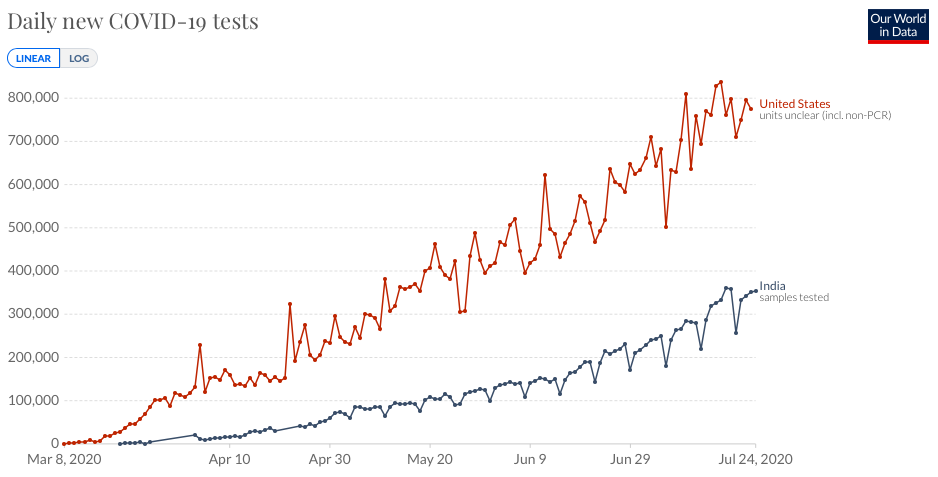

Latest testing data after previous update a month ago. Daily testing has more than doubled from the start of July from 2 lakh per day to over 4 lakh per day. For reference, US is doing ~8 lakh tests per day currently. July 24 and 25 have seen 4.2 lakh and 4.5 lakh tests respectively which is a big jump and close to the 5 lakh per day target for July set by the government.

July 24 - At 4.2 lakh, India's highest Covid tests in a day is good news, but positivity rate a concern

July 25 - India conducts over 4.4 lakh Covid-19 tests in single day | Latest News India - Hindustan Times

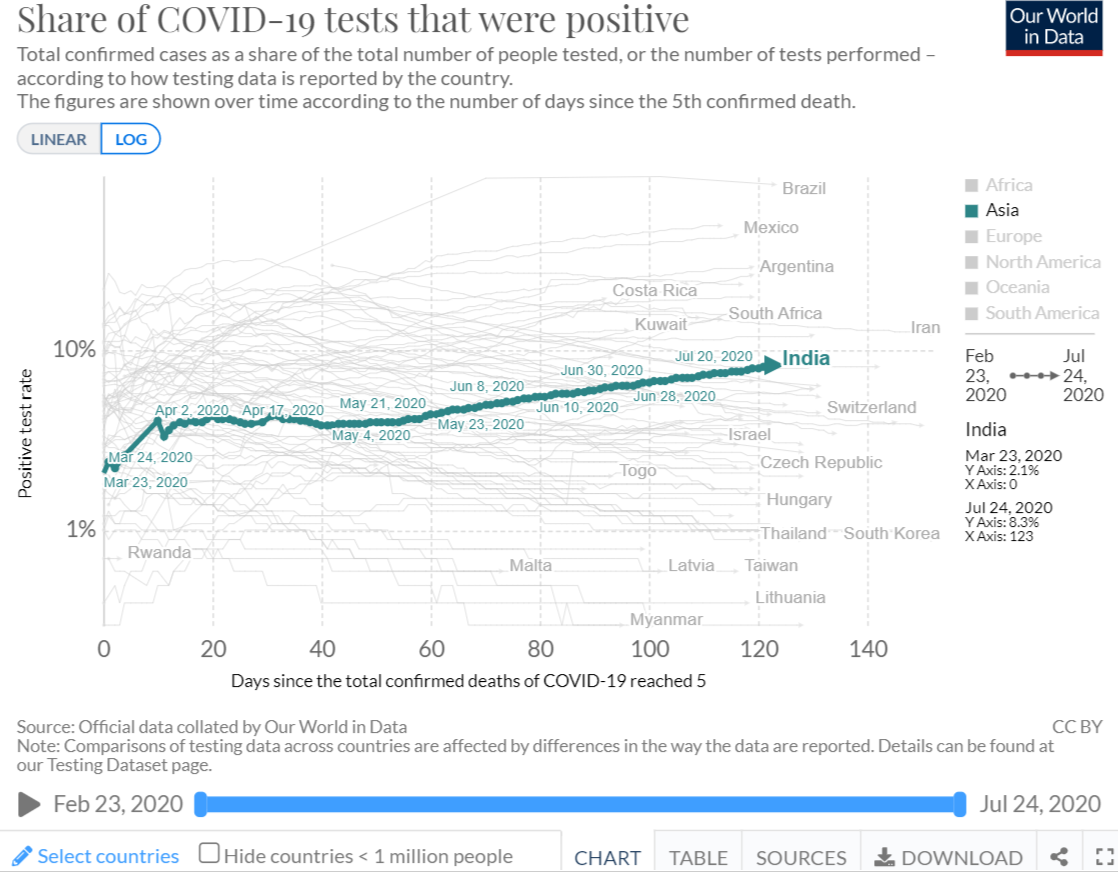

Positive rate suggests we are a long way from peaking:

According to statistics released by the health ministry Saturday, India’s daily positivity rate is now at 11.61 per cent. India’s seven-day positivity rate has been over 10 per cent since 11 July. According to the World Health Organization, a [positivity rate over 10 per cent] reveals that the testing capacity is limited to only those in the high-risk category, i.e., people most likely to have contracted the infection. A country should have a test positivity below 5 per cent for over two weeks before relaxing public health measures.

Update: Roadmap for conducting 10 lakh tests per day. Key bottleneck is procuring more testing machines.

New Tenders for Kits will be floated soon

Seven Canyons World Innovators Fund bought a 2.3% stake in Kilpest today @360/share. Sellers were Varun Daga and Own Infracon both of whom partially sold down their stakes.

$130 mn, US based small cap fund. This is their first deal in India.

One doubt. I have seen similar market transactions happening in one another stock. Is it legal for an insider to fix such transactions (e.g., timing, date, price) with other parties in advance?

Maybe this helps (all suppliers to govt. and related entites)

Even in international tenders, if the lowest bidder (L1) is a Class-I local supplier, the full contract quantity will be awarded to Ll. In case, the L1 bid is not placed by a Class-I local supplier, only half of the order quantity shall be placed with the L1 bidder. Then, if the lowest bidder among the Class-I local supplier matches the Ll price or falls within its range, the balance 50% of the contract will be awarded to the domestic firm.

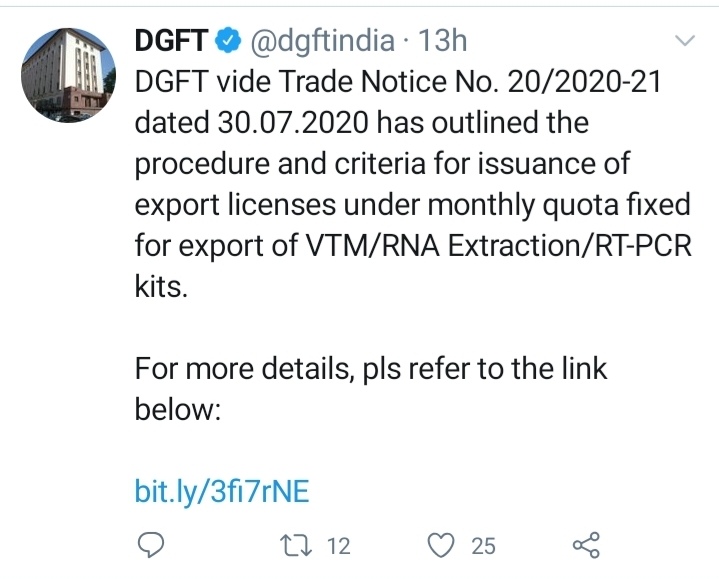

Export ban on diagnostic kits has been lifted with some restrictions.

This is a huge positive news for kilpest. They have got USFDA (EUA) approval, partnered with genophyll in US and also partnered with HS Biolabs in UK for some time now.

Q1 result today which is expected to be blockbuster.

Disc: Invested from much lower levels.

RT PCR V/S RAPID ANTIGEN TEST

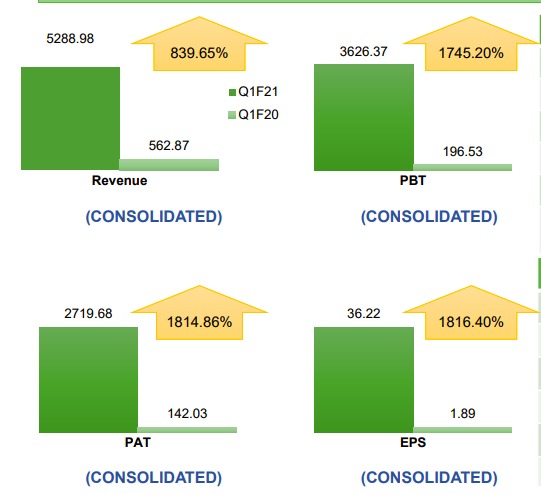

Absolutely Stunning result came from Kilpest:

839% revenue growth 5.62 cr to 52.9 cr (YoY)

1815% PAT growth 1.42 cr to 27.2 cr

EPS acheived 36.22 vs 1.89 (YoY)

Profit made in a single qtr almost equal to the total revenue in last whole year.

Q2 will be much more exciting with export ban lift, USFDA approval and much more testing being done using RT-PCR.

Disc: Invested from much lower levels and forms largest part of my PF. This is not a recommendation.

Stellar result from Kilpest which has completely blown past expectations. The margins are much higher than I was anticipating - didn’t factor in operating leverage kicking in so massively.

Measured but very strong commentary for Q2 (16 lakh kits sold in July itself) and anticipating 25k-50k / day utilisation from regular orders - any further tender wins and exports would be on top of this. I am quite impressed at the matter of fact tone of the presentation despite the unprecedented results.

On a related note, India stepped up testing to 6.5 lakh tests yesterday exceeding ramping expectations as well.

Disc. Invested

Investor Presentation Q1FY21

TTM EPS now is Rs.42.17 that brings back its PE to 9 (march low level)

Brilliant performance. This could be a 10 bagger stock this year. Already gained 7.5 times since march lows.

Hello everyone,

I did some number crunching based on the past announcements, Q1FY21 results, latest investor presentation.

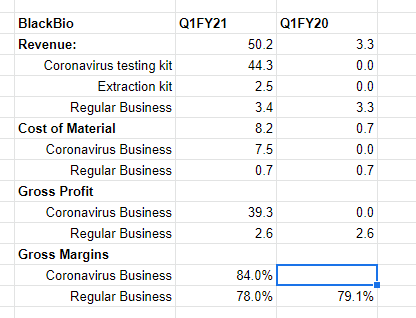

BlackBio’s Q1FY21 revenue was 50.2cr.

Till July the company had sold 8.86L kits at an avg realisation of Rs. 500, therefore contributing 44.3cr just from coronavirus testing kits.

The company had procured an order for extraction kits whose entire value was 5cr. Therefore, if we assume that half of this was also supplied in Q1, then the numbers from old regular business was 3.4cr.

Therefore, if I remove 20% cost of material from the regular business then it seems like their coronavirus business has more than 80% gross margins .

Till end of July, they have sold around 24.98L of testing kits with an average realisation of Rs. 421, which means that in July alone, they did a revenue of 61cr.

Let’s make some future projections.

India has crossed the 5L per day tests performed mark and has plans to take this up to 10L mark.

Kilpest mentioned in it’s presentation that-

Which means that if Kilpest is manufacturing 25K-50K tests per day then it is only catering to 5-10% of the overall demand which is not significant. Even at 10L tests per day performed in India, the max contribution by Kilpest will be 10% of market share given the current production capacity.

Realisation has been falling while demand has been rising. Assuming that realisation stays around Rs. 350 levels and given the range of daily production of 25K-50K, they can manufacture and sell 7.5L-15L tests monthly. That gives them a range of 25cr-50cr monthly turnover and 110cr-160cr quarterly revenues in Q2FY21 (60cr already done in July’21).

Given that they have a really high margin and assuming a bear case 30-40% EBITDA margin, we can expect an EBITDA of 33cr-64cr. This is after assuming a drastic fall in margins.

Negatives:

It is still perplexing that how they are able to have such a high asset turn.

Even though revenues rose 10x, employee cost went up from 50L in Q4FY20 to 1.45cr in Q1FY21. Other expenses went up from 72L to 4.4cr during the same period. This is a very bad sign. How are they able to control cost at such a level? We can expect this to go up going ahead.

In any case, I personally feel that the company has capitalized well on this opportunity. They acted fast, increased their capacity, and bagged orders. The numbers are extraordinary even though it’s a one-off. They have been fairly transparent with their announcements which is a good sign.

Regards,

Ayush.

Disc: Invested.

Let’s calculate net cost of production per covid RT PCR kit

(means ,how much cost kilpest have for production of 1 kit)

=In Q1 2021,Kilpest has sold 886000 test kits.@avg Rs 500

REVENUE(q1 2021)

= RT PCR covid rev @ 44 cr

=Other PCR revenue@6 cr

=Toral 3B black bio rev@50 cr

EXPENSE (q1 2021)

Consolidated expense @16 cr

Standlone exp is around @ 3 cr

So 3B blackbio expense @ 13 cr

In march quarter,3B blackbio have

4.5 cr revenue and

1 cr expense

for noncovid PCR testing

In q1 2021,3B blackbio has non covid revenue @6cr ,so expense will be around 1.5 to 2 cr(rough estimate)

So ,3B blackbio expense for covid test rt pcr will be around 13 cr-2cr=11 cr for 886000 test kits

So ,per kit expense will be around

Rs 125

How long this Covid will stay ??

Kilpest now is like HEG or graphite electrode story.

Seems they would do well for 2 more quarters.

Any expansion of capacity for the current demand?

This windfall will help them in building business and also new regions/customers, getting recognition.

As such it has long-term 5 year avg valuation of PE 20.

Business was growing steady anyway past 5 years at 35% CAGR.

Management has shown good capability and quality/honesty.

3BB caters to many kinds of testing, much more than corona only.

Corona testing can last for a year or more, world-wide, even after vaccination has shown good progress/coverage.

Any ILI/SARI (influenza-like illness/severe acute respiratory infection) will now get tested for covid as a precaution. This might become even a permanent heath protocol.

Disc: invested

3B black bio business was already growing at 35% CAGR pre covid. Its not a commodity like graphite electrode and having margin of more than 60%.

Though corona testing is not going to stop suddenly, but if we assume sudden drop in testing, They have earned enough cash which would help in accelerate growth in other kit business through R&D, marketing and established relationships

They have also left good image of product quality on new customers which will further boost brand value & growth for other kits due to proven track record.

World has accepted RT PCR technology as gold standard due to corona so there is little doubt of growth hinderance in future.

The biggest positive for me in kilpest is promoters seems honest and timely disclose everything so corporate governance is a big plus.

Their agri business is also turning around.

Management is already declared demerger of 3B blackbio which will unlock massive value. Other companies in this segment is trading at around 10 times of revenue which indicates how much value is left to grab.

For vaccine, even if it would be available in next 3 months, then too it will take long time to reach everyone and “keep testing” is only solution to stop fast virus spread as lockdown can not be done for long time. After that they can explore the export market in countries which is not vaccinated as whole world can not be vaccinated at once. So more or less 2 year story of covid kits would still left to fully play out.

Negatives: If testing stops, stock may consolidate here for 3 to 5 years which depends on their formal business growth.

Disc: invested

Hi All,

Could you please help in understanding that how demerger of 3B Blackbio will help to unlock value or re-rate diagnostic business considering the fact that primary focus of management even now is on diagnostic business (specifically Covid related business)? Please elaborate.

The company is perceived by many, particularly novice, investors as an agrochemical business even though more than 90% of the profit comes from the diagnostic business and this percentage is likely to keep growing. The growth rate of the diagnostic business is more than 50%, not 35% which is the growth rate of the consolidated business. The margins of the diagnostic business is nearly 50%, which is much higher than the agrochemicals or the consolidated business.

Many of us are lucky to have access to sophisticated screeners to get the real financial picture of the diagnostic business. Demerger of the diagnostic business into a separate listed entity will make the value of the diagnostic business very clear to the investors, and thus will lead to re-rating.

It is unlikely to be the case with Kilpest, but in general there is also possibility of accounting tricks/errors such as of moving costs to the standalone business and profits to the subsidiaries. In the case of an unrelated company named Brightcom Group (BCG), the standalone business has zero profits and all profits come from overseas subsidiaries that are impossible for investors to audit. In case of Kilpest, demerger will ensure there is no possibility of such accounting tricks.

Disclosure: Invested

My take on this current situation and future of the company: