I read Ruchir Sharma’s book “The Rise and Fall of Nations” (as a light read). I continue to remain bottoms up stock picker. One of the main criteria for stock picking is that a country should have good economic fundamentals with stability in business climate, currency, policy, debt etc. Only in this background, I think stock picking can work (try picking stocks in Greece or Russia!). With this context, following are some things I found interesting -

Commodity Prices

The historical pattern for commodity prices is as follows - there tend to be a boom for a decade, then fall for next two decades. Are we looking at low commodity prices for a long time?

Working Age Population

There seems to be very strong correlation between rate of growth/decline of working age population and economic growth. A 1 percentage point decline in growth of labor force will shave about 1 percentage point off economic growth. The two contrasting cases in point are China and Japan. One of the reasons China grew so fast over so many years was increase in its working labor force (15-65 years) and decent woman participation. The one child policy now has caused this rate of rise of working population to decline and this might hit China’s growth rate. Japan’s growth slowed down considerably after its labor force growth became stagnant or declining. Many countries attracted woman to workforce, increased retirement age and have managed to improve the growth rate. India also shall do well for coming years (but will there be jobs?)

Bad Times, Good Leader

Bad times make people turn to good, reformist leader. Once this leader reforms and results start showing up, bad policy decisions start creeping in i.e. when times are good, countries turn to left and when times are bad, they turn to the right.

Ruchir’s statistics show that, when a reformist leader takes over, the country’s stock market tend to beat the emerging world average by about 30% in first three and half years. Then markets start moving sideways. As leaders get into second term, results turn out to be average.

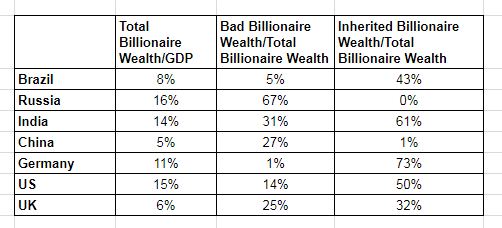

Good Billionaires, Bad Billionaires

It is natural & healthy for a growing economy to generate wealth and to have emergence of billionaires along with it. It is important that more billionaires are emerging into innovative and productive industries (IT, Automotive, Pharma, electronics manufacturing etc.) than those in the rent seeking industries (Real estate, oil, gas etc.) which are dependent on family ties and political connections.

Creative destruction drives strong growth in capitalist society and bad billionaires have everything to gain from status quo.

Following table is an interesting one →

Rate of Investment

The statistics tell that for fifty-six highly successful postwar economies in which growth exceeded 6 percent for a decade or more, average rate of investment was about 25% of GDP during the boom period. Anything less than 20% and more than 35% are a bad sign. When investment usually goes above 25%, money flows into unproductive industries like real estate, state sponsored companies etc. It is also important to look at the quality of investment spending i.e. whether the money is going into roads, ports, factories or whether it is going into subsidies etc.

Inflation, Deflation and Why CPI is not the Whole Story

Many emerging economies face inflation due to supply side limitation and many times this hyperinflation leads to change in governments, riots, unrest etc. Low inflation is usually good sign as it signal strengthening of supply side infrastructure. Deflation is not so straight forward as it can be due to productivity improvement (good) or due to decrease in demand (bad).

But CPI is not the whole story, it is important to track asset prices (stocks, housing) as well. Every major economic shock in recent decades has been preceded by an asset bubble e.g. Japan 1999 (Stock & Housing bubble), US 2001 (Tech stock boom), US 2008 (Housing bubble). Generally, bigger & faster the run up in asset prices, more the likelihood of the crash.

The Kiss of Debt

Just for this chapter, I would say that this book has been worth a read. The name was invented by Robert Zielinski, a bank analyst who had seen the impending Asian financial crisis. He wrote a brief paper that stated that many financial crises in the emerging world had been preceded by five consecutive years of debt growing at 20%+. Instead of writing it as a report, he wrote a play named “The Kiss of Debt”.

If the five year increase in private credit share of GDP is more 40%+, the economy is likely to face a slowdown/crisis. Conversely, if the private credit grows much slower than GDP for five years running, it creates conditions for economy to recover strongly as banks would have rebuilt stores of deposits and will be comfortable lending again.

According to McKinsey report, out of $75 trillion increase in debt since 2007, $21 trillion+ has been racked up by China. China remains a ticking debt bomb and very likely next crisis is likely to originate out of China. In 2013, the five year increase in private debt reached a record 80 percentage point of GDP.

In recent decades, recessions can arise out of debt fueled property booms just because of explosion mortgage finance business. In 140 year period in 17 advanced economies, mortgage lending has increased by factor of 8 while bank lending for other purposes has increased by factor of 3. (Affordable Housing will end in bubble?)

Another important learning is perils of “collateralized lending” compared to “cash flow based”/“repaying ability” based lending. The former lending works as long as borrowers short on income can keep getting new loans to cover their old loans - based on rising price of property or other assets.

Typically, when a bank is disbursing more money in loans than it holds in deposits and relying on outside funding to fill the gap, it signals a trouble.

Regards,

Rupesh