You are making an assumption that you will be able to invest all the proceeds at prices which are as depressed as now, which may not be true. If you assume that you will be able to invest proceeds only at 8%(which is more realistic) your returns will drop to 13-14%, which is what one would expect from a single company credit risk opportunity. So market is not pricing it a highly depressed level.

But reinvestment risk is true for every opportunity. Do you know any other with a 13%-14% opportunity AA+ bond and remember its post tax as long as div is below 10 lakh

1 Like

It is interest so it is not tax free.

There are credit risk funds having YTM of about 10%. Risk in funds is much lower as it is diversified across companies. Also you can hold funds for long term>3 years and lower your tax outgo significantly if in higher tax bracket.

Essel group has already defaulted on interest payments.

So key point is are returns really very high for risk one is taking? Can we invest in diversified equity MF and get similar returns without re-investment risks? No easy answers here.

Don’t like at rating and buy as next jump cod be to D straight away.The credibility of rating agencies is questionable after ILFS and DHFL. DHFL secured NCD holders were not paid interest last year and rating agencies/debenture trustee had no clue and could not keep our trust.Therefore even secured debentures have lost their relevance. If you are confident of their balance sheet, then only invest

Don’t look at the rating AA+ and buy

just one correction…its dividend not interest as it is a preference share not a bond / loan and zee pays DDT on it (you can check the BS its part of equity structure and DDT payment)…regarding credit risk obviously i agree with you that everyone will have to take a call as per his understanding and risk appetite

Great pointers.

Xirr… already factored that reinvestment risk makes ur realised IRR lesser. Rightly, it will yield 13-14% unless market again gives some opportunity

Proceed is dividend, not interest.

Re.credit risk, as biased as I may sound, latest credit report has no mention on financials or fundamentals. It only downgraded the paper due to management shuffle.

So again, the bet is that 400 Cr default will NOT happen in interest of common equity stake of large investors.

Of course there r cos which hav defaulted on even 2 or 12 cr… Given that after such year long unfolding of events, essel group has somehow managed to prevent equity value’s ‘complete’ erosion, unlike other groups, it is a bet on management’s intent n co’s ability… both are probable on a positive side

2 Likes

Zee is a great brand in the world of entertainment, mainly in TV channels as well as Zee5 , their OTT channel. But change of ownership throws up its own set of challenges on accounting side. It is found that so called “due diligence” done before buyout/takeover/merger is generally quite weak/ineffective. This means after the ownership change, few quarters of financial under performance can be expected. (For eg. Acquisition of United Spirits by Diageo)

I would prefer to wait to see balance sheet clean up getting over before venturing to buy. I believe in the long term story of Zee and feel they will do well under new owners in the long run.

Disc : Not invested. under watchlist.

2 Likes

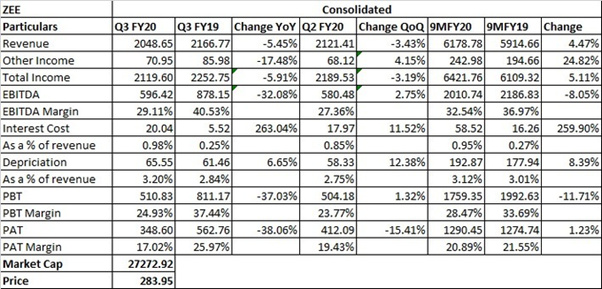

ZEE Q3 Results!

Q3 FY20 CC:

- Going forward I, Punit Goenka will remain the sole representative of the promoter family on the board of the company. Mr. Chandra will not be putting up his name for re-election in the next fiscal and will assume the position of Chairman Emeritus. To further strengthen the board, new independent board members, with expertise in the field of either media or technology, will be inducted. This exercise is expected to be completed by the month of February. All these appointments will have to be ratified by the shareholders and will come up for their consideration at the forthcoming AGM.

- Surplus Cash will be invested in high quality/liquid instruments.

- Lastly, on receivables from Dish TV and Siti Cable, we have performed a detailed analysis of recoverability. Based on the assessment, the company has determined that the entire balance is good and collectible. As per the plan agreed with Siti Cable and Dish TV, the arears will be cleared over 12 and 24 months, respectively. Consequent to the delay in payment, the company has taken an expected credit loss charge of Rs. 376mn during the quarter. The Company will closely monitor the collection pattern from the said customers.

- Now moving on to cash generation for the next year. Over the last couple of years, the company has been in an investment phase, acquiring content, primarily movies for expanding TV business and scaling up ZEE5 content library. While for ZEE5, movies are already one of the biggest propositions for the consumer, we have just launched 3 movie channels in regional markets to monetize the content that we have acquired. FY20 will be the last year of disproportionate increase in inventory and I expect that from next fiscal onwards, the number of inventory days will start reducing. In FY21, we expect that over 50% of PAT should get converted to cash, significantly improving the cash conversion ratio.

- Third quarter is normally a strong growth period for us, however, the tough macro-economic environment led to a decline in ad revenues. Most of our advertisers are going through a slow-growth period and that has led to a cut in advertising spends. I believe that the worst phase is behind us and we will start seeing an uptick in growth from the next quarter. The proposed changes to the tariff order by TRAI are being challenged in the court and we are awaiting the final verdict. However, I am confident that our strong portfolio of channels across markets will enable us to navigate any regulatory changes in the most efficient manner.

- Now coming to ZEE5. In the month of December, it recorded a peak DAU of 11.4mn. ZEE5 released 26 original show and movies during the quarter and continues to be the biggest producer of digital original content in India. We are well on track to achieve the target of producing over 70 original content pieces this fiscal. ZEE5 launched a refreshed version of Progressive Web App in December which enables a fast, engaging and immersive user experience. We are also in the process of inking deals with smart TVs for placement of hotkey on their remotes which will make ZEE5 content accessible to the users at the click of a button.

- Programming cost for the year will still grow by 10-12%. Programming cost is subjective as it depends if they have any productions lined up in the quarter.

- What we have said is that this is the worst quarter. There will be definitely an improvement from fourth quarter itself. Just want to put this quarter decline in perspective and that will give you an answer that why we are saying this is the worst quarter. There are three things which are actually driving this sharp decline - one is that we took off two of the most important channels from DD FreeDish, so that itself is contributing almost like 450 basis points of decline and that gets into the base from 1Q of FY21. So that degrowth which we are facing on account of FTA strategy will not be there. Secondly if you look at last quarter’s numbers, the base was extremely high. We grew around 23% in the last quarter on the back of 30% growth in a year before. So that was the reason, as I mentioned that we were sensing very strong market in the last year same quarter, we had done lot of events and we were tactically investing in lot of properties. So that also resulted in significantly better revenue growth last quarter. So, the base was extremely high and that has impacted to an extent. Last reason is that overall we are seeing weak economic environment. So that’s where most of our consumer companies have seen a sharp slowdown. Now in this slowdown, generally the consumer companies tend to hold back on new product launches or new innovations, which typically accounts for up to 50% of their spends. Cut back in the innovations has actually led to a significant drop in industry revenue itself and which is reflected in our numbers also. So, going forward we think that the base itself will be much better and secondly the worst is behind us. We are seeing some stabilization in ad revenues in last couple of months and we think that we are quite hopeful of recovery to normal growth trajectory in the coming fiscal.

4 Likes

[MCA orders inspection of Zee Entertainment’s books] https://www.moneycontrol.com/news/business/companies/mca-orders-inspection-of-zee-entertainments-books-4903391.html

1 Like

ZEEL is basically production house and no better way to judge it than the quality of art it produces

Sharing some things which they have done right in last couple of years which went missed among promoter pledge issues

Zee Studios says it has reason to celebrate. The movie production and distribution company has recorded five major hits across languages in these three months — Manikarnika -The Queen of Jhansi (Hindi) Kala Shah Kala (Punjabi), Anandi Gopal (Marathi), Kesari (Hindi) and Lucifer (Malayalam), together grossing Rs. 375 crore at the worldwide box office.

This is a fairly impressive box office run for a studio technically less than four years into the business. Having halted its film production after Gadar: Ek Prem Katha in 2001, the company returned to it in 2015 with Aishwarya Rai-starrer Jazbaa, and attributes the recent numbers to lessons learnt on the way.

“There is no specific guidance on budget but we are looking a little more at mid-sized, youth-centric films which don’t necessarily burden the project upfront with huge star or director fees," said Shariq Patel, chief executive officer, Zee Studios adding that budgets are allocated according to the filmmaker and lead cast in question and the budget for an A-lister will differ from the budget for a newcomer or an actor on the verge of breaking out.

Zee has roped in Parmanu: The Story of Pokhran director Abhishek Sharma, Bosco Martis from choreographer duo Bosco-Caesar, Housefull 3 co-director Sajid Samji and Toilet: Ek Prem Katha filmmaker Shree Narayan Singh for its upcoming projects.

Source: Zee Studios Looks At Mid-sized Films, Web Shows To Strike Gold | Mint

ZEE5 PARTNERS WITH APPIER TO IMPLEMENT NEW AI-POWERED MARKETING AUTOMATION PLATFORM AIQUA

They recently announced ZEE5 Super Family (ZSF), a first-of-its-kind gaming experience for its viewers of fictional content. Although gamification isn’t a new trend for the OTT space, with ZSF, ZEE5 aims to connect India-wide GEC content like never before.Though I am not super excited about this one

Read more at: ZEE5, India’s largest OTT platform reimagines Hyper-personalisation for consumers

ZEE5, India’s largest OTT platform reimagines Hyper-personalisation for consumers

Targeted at students from Grade 6-12, it focusses on concept-based learning through interactive video lectures. As part of the introductory offer, ZEE5 will offer Eudauraa free for six months for new users who would subscribe to the annual pack and register before March 31.

Compare above to Netflix 15x worldwide subscribers and zee5 is just 2 year old

Some of great shows on zee5 are:

- Kaafir Kaafir (TV Series 2019– ) - IMDb 8.4

- Code M Code M (TV Series 2020– ) - IMDb 8.9 (watched)

- Rangbaaz 2 seasons https://www.imdb.com/title/tt11203746/ 8.5 (watched)

4.The final call The Final Call (TV Series 2019– ) - IMDb 7.4

5.Never kiss your best friend Never Kiss Your Best Friend (TV Series 2020– ) - IMDb 7.7 (watched)

Disclosure: Invested and holding around 5% of portfolio and this post is about new ventures transforming the co. Will post later about pledge/promoter/corp governance and traditional business ZEE/ZEE news etc as well as valuations in future posts.

3 Likes

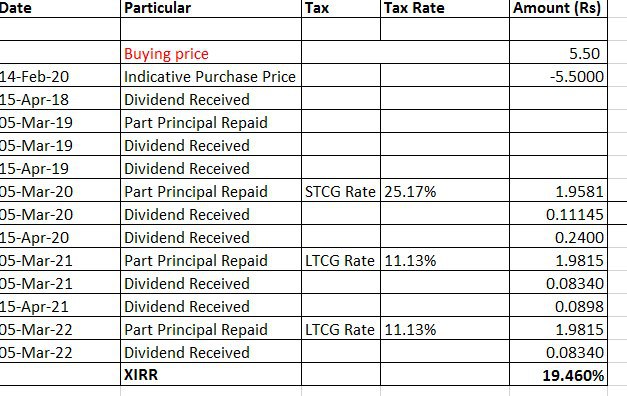

ZEEL has announced record-date for its this year’s principal repayment and preference dividend.

Clears one overhang of this year.

This is also reduce the outstanding pref shares to approx 800 Cr (from 1200 Cr). and there is no other debt

However (positively or negatively), even at this price XIRR is ~21.6%.

This is pre-tax and from next fiscal, dividend will be taxed in investor’s hands so it is likely to hit large firms/HNIs who pay tax at higher rates.

Disc: Invested since April and added recently

1 Like

From the above filing it seems that the 6% would only be paid on the rs 2 that is redeemed. Not on the entire 6 rs. Is anyone sure if we receive 6% of 6 which is 0.36 or 0.11148 as mentioned. Thank you.

On 2 rs for 1 apr 2019 to 5 mar 2020.

On remaining 4 rs will be in mar-apr 2020.

This image ws prior to ex-date

2 Likes

Anyone else following this stock?

1 Like

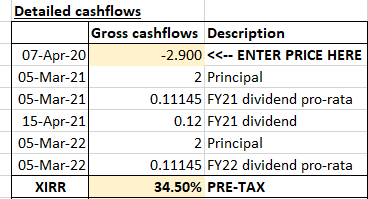

Revised XIRR calcs pre-tax

Again, the lucrative XIRR is a perception problem with ZEEL (as well as reinvestment factor which forum members have pointed out earlier rightly).Something too good to be true is actually too good to be true.

Disc: Invested in pref.shares

1 Like

1 Like

Further to today’s investor call with respect to an additional investment in Margo Networks Private Limited (SugarBox), a subsidiary of the Company, which was hosted on Microsoft Teams, enclosed please find a copy of the presentation