How is acquiring & selling these shares bad?

CG Power 100% shares are pledge , means company is in bad shape and doesnt generate sufficient cash flow. Its a risky trade where both ups and lows r high. Yes bank is under pressure due to such kind of investment.

I think you’re understanding it wrong.

Yes Bank has invoked a pledge which means it’ll sell off these pledged shares (at whatever the best price is) and reduce the amount of outstanding loans against CG Power.

It is not a new lease of life for CG Yes Bank has signed on to.

2 Likes

Yes bank burnt its fingers in Fortis healthcare shares also similarly.

But all these skeletons are are pre RK. We cant say whether the strategy remains same under RG.

Regards

Disc. Tracking actively.

But they are not investing in CG Power. And anyway, CG Power is not really in bad shape.

Investing is more luck than skill.

I understand most of us here are skilled but not skilled enough (unless you are a professional)

Atleast for me, I am not a professional.

Just like a professional badminton player, would time and place the ball across the court for points. a non professional chances to win are only if he manages to place the ball at the other end of the court.

I would rather buy a bluechip Bank at a fair price and hold it for years. Is my best chance.

Every company has it’s fair share of bad days and good. The point is would you buy it during the bad days.

I don’t see any other circumstances you could buy YES Bank at these levels.

Obiviously things are bad, price might fall further.

I don’t want to be a contrarian nor an expert.

I just want to practice what I know. Place the Ball on the other side of the court.

4 Likes

I think it is not, the ingredient of luck will make the investing dish a lot more delicious but not that alone. Different people have different circles of competence. Some fund managers invest in cyclical companies as they believe they can get the cycles right. These type of situations could lead to potential loss of capital or could reward handsomely. And you forgot an important aspect of both investing and sports - experience. If you don’t indulge yourself in varied zones, expand your horizons you could never gain a meaningful experience which in turn will stop you from making loss-making decisions in the future. That is why a lot of members say they are still learning despite being in this forum for years. Because only when you have experienced something and you come across the same situation or a similar one, you will know what to do. I had beginner’s luck, saw a bull run first, then saw everything tumbling down, great experience. Now I have got a rough idea of what to make of a stock.

So I would rather give priority to knowledge, experience than to luck. You could add discipline to the list too (bowing out if your plan did not work). Luck will make a well-etched plan a multibagger, sure but not luck alone. Buffett too had some luck, he said he was lucky to have been born as a male in US at the right time and that he had won the ovarian lottery, but luck alone did not make him the most revered investor as his calls were wrong sometimes too.

As they say in the market, investors who have got experience will make money and who have money will get experience.

4 Likes

Sir,

Am i reading wrong but all r saying yes bank has acquired the pledge shares.

Great examples but wrongly applied. In all these examples core ops was intact but in case of YB it is the core corp. banking which will give maximum headache in the short to medium term. They want to move away from the current core. That’s why it is important to understand the Indian context without mindless application of great’s methods.

2 Likes

Two points to keep in mind: 1. Some of these issues were not core banking issue and hence must analyze the extent of difference between those scenarios and our own investment scenario and 2. some of these deals, Buffet was not a minority shareholder but someone who could dictate terms and get it on his own terms and conditions which a minority shareholder does hold privilege to do

3 Likes

Me too a fellow novice in the market and completely new to financial world.

If banks are cyclic, so have been the turmoils and troubles, particularly with Yes Bank. HDFC Bank’s journey has been smooth more or less and I would like to see a comparison with Indian banks instead of US banks, as I believe the institutions here and there operate differently many times despite being in the same business and the disastrous situations may be the same, but the cleaning may be different, particularly with Gill.

1 Like

1 Like

It was Rana kapoor who built and grew Yes bank from a small size to this size.

It was not the investors!

10 Likes

Guys,

Yes Bank thread is being littered with personal views without any logic or facts. Kindly refrain from such useless posts which do not add value to the thread.

If you have an investment case or a rejection case, kindly put up with valid reasons without bringing in personal likes/dislikes for RK or any other guys involved in Yes Bank.

Those whose posts dont add value are requested to delete the irrelevant posts or else post 24 hours we would be needed to sanitise this thread.

26 Likes

Iam invested in YES Bank from 180-200 levels ( Sep 2018). averaged it upwards upto 220 , and downwards upto 170. No prizes for guessing that its in a firm bear grip - wherein every positive development is discounted and every negative news is magnified and blown out of proportion. This post is NOT a rant- but just a self introspection journey … When i started buying @ 180 levels - the thought process was that I am getting one of India’s leading Private sector bank at a P/B of 1.2, market cap of hardly 50K crores with a definite room to grow upwards at a decent double digit pace for a very very long time.

As a regular retail investor, I did all the usual stuff- going thru the AR, Forum thread on YES, some back of the envelope valuation etc. etc.

I can do either of these 2 things …

-

Book losses and exit - may be a 30-35% shave off … walk away with a humble pie in the mouth…- that my investment theory has backfired .

-

See if the investment theory that I have bought it with - still holds good … My thoughts are

a) New management in place - clear evidence of kitchen sinking, aggressive clean up of doubtful skeletons

b) enhanced regulatory scrutiny - massive increase in the quality of disclosures, additional RBI presence in the board etc.

c) Need to look good when they raise capital in the next 5-6 months - another vicious cycle of good base book, quality of disclosures etc.

d) whats the worst case scenario in terms of bad loans … another 10K ? means - another 2 quarters of pathetic results . Market cap can go down to lets say even 15/20K ( another 40% downside … May be Share price @ double digits.

My question is - how do we approach such scenarios ? Do we give time for news to settle down and take a call - lets say 12 months down the lane? My heart is rooting for Option 2- that the bank would recover …whereas brain is directing me to place the sell order and cut losses!

Ram

7 Likes

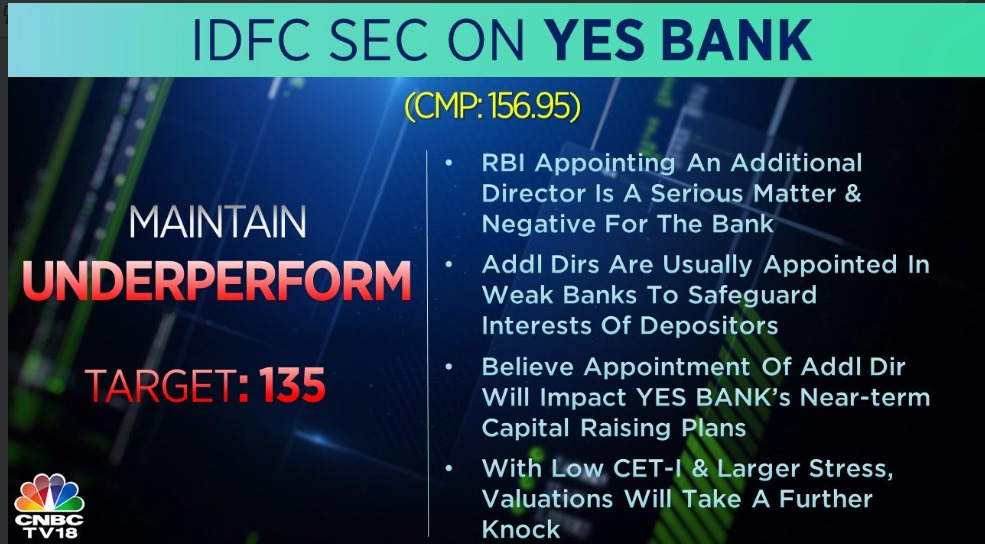

Is appointment of additional Director is always a bad news or there is some other view??

However hard I try - I am not able to come up with a positive spin to the news of RBI director’s appointment. Clearly means that RBI sees YES to be systemically important one and wants to have a good pair of eyes ( read about Mr Gandhi… very conservative Central Banker and carries lot of respect within Banking circles) …

As a shareholder, I am quite happy that this news will provide some relief from the constant bad news / rumours on YES’s solvency. But Moneycontrol tells me that SGX is factoring 10% downside - again !

I had the exact view and had a small holding bought at Rs180 and sold at Rs160. My reason was the opportunity cost. On the one hand we have corporate banks where all of them are performing very bad. When one sector recovers another fall in stress. No point holding them just for the sake of diversification.

On the other hand, we have the new age small finance banks, which is Retail focussed, granular, with high liquidity and high NIM addressing the unbanked sector in India which has a long runway. So I switched my holding in NBFCs and Yes Bank to AU small finance bank, Equitas and Ujjivan. Equitas and Ujjivan offer value similar to Yes Bank at this price.

1 Like

Whatever bad had 2 happen has already happened! V might sink by another 30/40% post next couple of quarter result with d renewed cleanup with d microscopic eyes of Gandhi. V r in d aftermath of d bad practices. If RG walk the talk post Q4 result on the growth aspect even with d cautionary eyes of RBI, d green shoot might not be faraway. Holding @ 155, contemplating about selling if I get better pasture outside