YB, Indus ind and kotak bank look very similar in terms of casa, total deposits and number of branches…

All 3 of them give 6% on savings account if I am not wrong

Annual report 2016-17 has some figures on the divergence-

divergence in provision for the year ended march31,2016-858 cr,net profit for year ending 2016 was recalculated to 1978 cr instead of 2539cr. So are the profits for subsequent years also going to be restated, but i cant see this restated figure in screener.So was book value adjusted after all these divergences, This is from page 267 and a line below mentions about the non recognition coming from a single account and strong chances of recovery.

Screener and the annual report shows huge contingent liabilities 583471cr, believe these are derivative instruments, Are these common to all banks and what are risks with these instruments.

2 Likes

Hello all this is my first writings here so I’m not aware of all rules of this forum. Not only yes bank but almost all shares went down drastically but recovered also drastically including sensex and nifty too…see 21st Septembers move of shares like gnfc,parag milk,escorts,suven life science,mahanagar gas,lupin,magma fincorp,future consumer and many many more went drastically down and in no time they went up with abnormal volumes and abnormal high low levels …this means that someone big must have short sell almost all shares ofcourse with prior planned strategy and they also covered theirs intraday shorts with big big profits ,and some how they went success in creating panic in already feared markets and made big money …what sebi is doing ,see the volumes of almost all markets !!! See the volumes of yes bank!! It all looks planned strategy for multipurpose like to gain profits by creating panic,against Indian financial market by vested interst …but why every time this happens just before elections !! Every times before election ruppes goes down drastically ,and market sees huge volatility, do government also involved in this shit? Otherwise this is not possible at all … if i hurts anyone …i apologize… but this kind of events must be looked after by sebi because retailers leave the markets forever believing it speculation and 21st event was purely speculation/satta by biggies jeorge Soros !!believe it or not !!

5 Likes

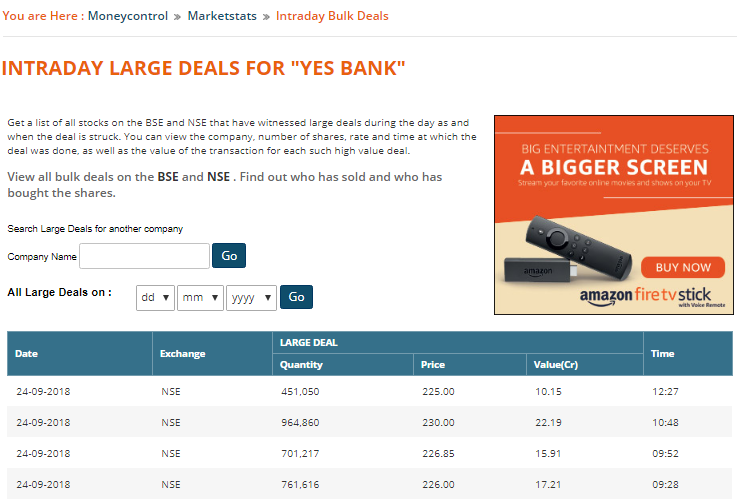

On opening there was a single seller of 3 Cr shares , with the sole intention of hammering it down . If any genuine fund/ person was interested in selling he wudd have sold in smaller chunks .

1 Like

Thank you for the clarification bro…My bad ,am blindly depending on screener nowadays

Higher savings deposits rate is a strategy being used to get incremental market share from the public sector banks which are under Prompt corrective action, as noted by Rajat Monga in last investor call:

Somewhere down the line it presents an opportunity to cut costs of funds for the bank, when it thinks the incremental market share is not worth chasing:

Sorry the earlier message went out without completion. I would like to summarise the discussion and narrow down on the narrative. Here are the thoughts that are keeping me busy:

-

Change of guard at the helm - The pros being that the new person in authority will bring out the true picture of the NPA’s and therefore, by virtue if after the recent divergences the subsequent upgrade of accounts were done on merit rather than showmanship basis - this should play out rather well.

The con being of course that if the true picture turns out to be murky, the the public will negatively re-rate the security further. - The heart of the matter being the NPA’s and the divergences - As has been correctly pointed out by several members on this forum - Yes bank has had issues in reporting the correct numbers in the past. The new person of authority will like starting from a blank slate and therefore, revealing all facts at face value. This is something that the value investors are looking forward to.

- Who will be the new person at top - There are issues between the promotors (Rana kapoor and ashok kapoors lineage) and for that reason the selection of a new person is an uphill task. Internally trusted people vs an outsider coming in.

- The public sector banks have tumbled recently and that should allow for tail winds for the entire private banking sector

- Yes bank has historically focused on corporate lending and with thin margins and even recently in the last couple of months have increased their loan book substantially.

The question i have is how tight is the loan granting protocol at Yes bank. We all have read exhaustively in interviews etc of this protocol being projected as robust. Does anyone have specific insights to share on this matter?

Requesting the old guard in this forum to comment on the probabilities of various outcomes and how they see the situation playing out in the next couple of years. I am new to this forum, and would like to learn the approach being adopted by the seasoned investors.

And 3 crore shares at opening with no Major bulk deals reported on the exchanges leads to a Big Question. Who’s the culprit?

1 Like

More so because no TDS is deducted on savings interest… On FDs, 10% TDS gets deducted by the bank, shows in your ITR, and one might need to give 20% more tax if one earns 10lpa+… Obviously people prefer 6% on savings… YB expects 30-40% casa growth again this year.

1 Like

Hey, what is the source of this information? Is it public or proprietary? I’m asking so that I can pull the info whenever I want. Thanks!

Why should he be labeled ‘smug’ if he’s thinking of challenging RBI’s decision? Is it not within his legal right to do so? Or you have made up your mind against him and are bent on giving him a public trial?

8 Likes

More remours …it seems day by day these guys are becoming like those WhatsApp and FB forwades …

News channels just seem to be concocting stories out of thin air. There should be some kind of a rule to disclose specific sources and the credibility of news items like this. How has this channel verified the facts? Can these reporters be held responsible if tomorrow this turns out to be false?

If there’s a take back on this decision to limit RK’s term, RBI will further lose credibility as an institution.

And why is RBI not coming out in the open with specific reasons for not allowing him to continue? The rumor mongering is counterproductive and potentially loss making for investors!

3 Likes

As per one ET article, he was summoned to RBI few times but he did not mend his ways. Now do you think the RBI would leave a loose legal end to allow him to come back on this? Once they have taken a decision you can’t fight unless you are mota bhai. If RBI decides to carry out a public trial, it would be hell lot embarrassing for mr RK. It is in the interest of everyone to let it go and allow others to take over. It is all but over for him as a promoter.

Has RK really sold shares as well? Just read this on Zee Business report:

This is getting crazy!

Media release by Yes Bank -

The media release is little confusing to me. In the headline only they say Rana kapoor will be reappointed , but nothing about it in the whole article. Has the RBI cancelled the decision ? or I am missing something. Please clarify.

Rana Kapoor was already reappointed. The meeting today is to discuss the next CEO considering RBI rejected the reappointment after January 2019

Rana mustn’t influence board in CEO search: Madhu