2018 AR is released. Link http://www.yashpapers.com/pdf/yash_papers_ar_17_18_web.pdf

Some points (copied from the AR):

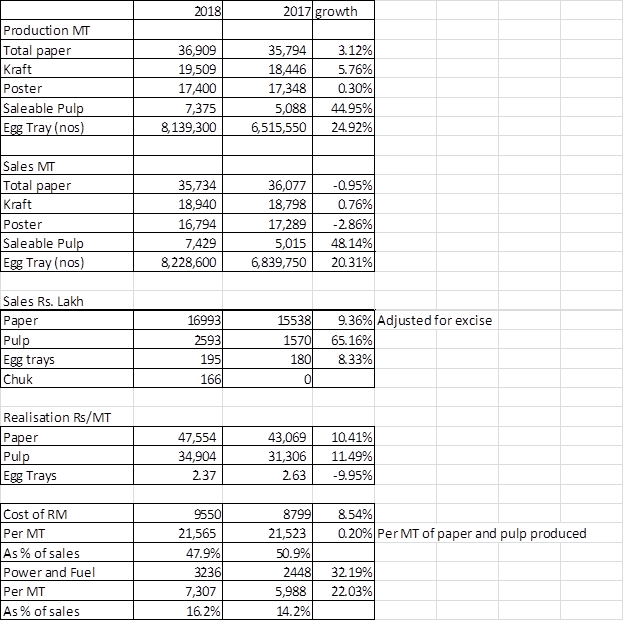

Our achievement: We reported 3.11% and 44.94% increase in paper and pulp production respectively, driving our turnover growth of 9.99%, operating profit surge of 102.06% and net profit increase of 60.27% - the best ever in the history of Yash papers.

We are going to enhance PM3 capacity by 42.86% which helped us in achieving one of the highest output till date. _(this is not clear – whether they are going to enhance, or they have enhanced – see below)

At Yash Papers, we focused on manufacturing paper bags. We tied up with a Swedish technology provider to ramp up our technical edge.

Our achievement: Demand for our paper bags grew month-on-month basis in 2017-18; Detpak, one of the major paper bag producers in the world, became our customer. – targets? this can be a new attractive line of business

We invested Rs 62.33 crore to build a state-of-the-art plant for manufacturing compostable table ware. We commenced our commercial production in January 2018 and in a brief span of three months, we achieved a capacity utilization of 30%. Our target: achieve 60% capacity utilization in 2018-19. This is not all. Our research team created egg trays from factory sludge and pellets from pith – usage of pellets?.

Our achievements: During 2017-18, our fresh water consumption reduced by 8.38% and we could save 4,027 tonnes of CO2 emission. We emerged as India’s first B Corporation aiming to be profitable as well responsible to the environment.

We saved electricity consumption; we installed technology to virtually consume zero fresh water at two of our plants, we improved emission quality through better sedimentation and clarification of recycled water

Vertically integrated - paper manufacturing capacity of ==== TPA complemented by 130 TPD pulp manufacturing, 145 MT BD chemical recovery and 8.5 MW power generating capacities (two plants having extraction-cum-condensing turbines and rice husk-based FBC boilers)

The year saw paper production growth by 3.11% while our pulp production reported a 44.94% growth during the year under review. Besides, we continued to work on cost saving initiatives. We reduced using of fresh caustic by 50% through the implementation of bleach booster; Reduced COD in effluent by around 25%.

Increased the production capacity of PM3 by 785 MT (4.3%) tonnes per annum during this year

Adopted new sedimentation technology which helped two of our manufacturing units to bring down fresh water intake to zero • We invested in infrastructure to store 100% of our bagasse in wet condition helping us in increasing yield, reducing shade variation and deterioration of bagasse. • Undertook initiatives to reduce electricity consumption • We reused water from the process for wet storage of bagasse

Developed Six new grades in the paper segment.

We developed two new qualities for paper bags which resulted in increasing our monthly orders • We added Detpak to our client list. It is one of the largest bag manufacturers in the world • We developed six new products for the exports market. We are entering into the colour wrapping segment which has a strong demand from both the domestic and international markets • We fully automated the pulp plant which helped in minimising the feed volume variation by automation, resulting into regular feed of chemicals sychronised to feed volume resulting in constant quality of pulp and hence the consistent paper quality. This has resulted in lower cost of chemical consumption and retention of fiber strength as well.

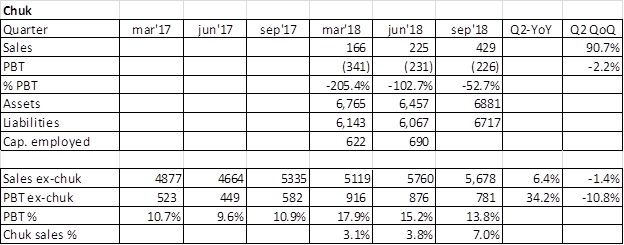

The following are the corporate priority for the coming year: • Strengthening the water treatment plant with new technological Installations resulting in enhanced efficiency by 5% • Redesigning PM # 3 to manufacture high strength bag paper • Innovating for use of lime sludge in solid waste generation for in-house consumption • Innovative manufacturing of rice husk ash for high-end market • New product development in Chuk for Indian Railways

Company sourced 124368.91 tonnes of bagasse, comprising 100% of its requirement within 60 kms from its plants. The Company created wet plant for better storage of bagasse. Raw material cost as % of revenues: 2016-17: 28.71% | 2017-18: 31.04%

During the year under review, the Company enhanced paper plant production by 16.98%. The Company’s various initiatives helped in achieving 94% capacity utilization in paper manufacturing.

Operating cost as % of revenues: 2016-17: 94% |2017-18: 89%

1,12,331 Trees saved 8,53,540 Tonnes of coal saved 239 mn litre Reduction in fresh water consumption (mnlitres) 81,08,700 Pieces of egg trays produced; conversion of waste into value

Non-fossil fuel 100% energy met through renewable resources

Some quantative data:

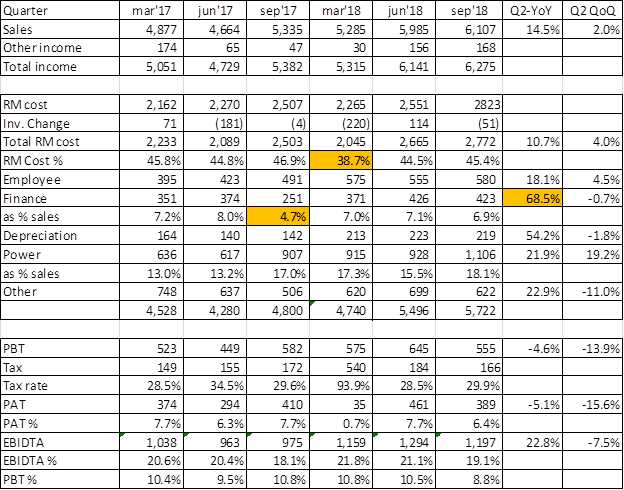

One glaring error I noted in the cashflow statement was that reduction in current portion of long term borrowings of 15cr has been shown under cashflow from operations, due to which CFO has increased from 22cr in FY17 to 48cr in FY18. Still, adjusting for this amount of 15cr, CFO is healthy and improved. But company should be careful of these kind of entries and should avoid them. I have other doubts in the numbers (more clarificatory in nature) and I will try and seek answers to those.