RajeevJ

February 9, 2024, 4:30am

90

The WPIL Q3 numbers have disappointed the markets, perhaps due to a decline in profitability. On closer look, this is largely due to lesser other income, something that should be ignored, even when it is high to get a better view of the picture. The other reason for declining profits is the sharp increase in employee remuneration. The mgt mentioned that the environment is pretty robust it is gearing up for bigger volumes for which there has been fresh hiring, not only in India, but also overseas. There is always a lag time before volumes start coming in.

The mgt expects a good Q4, which is always the biggest, volume wise. The current year 23-24 is more of a consolidation year after a 50% growth in Sales last year 22-23. This is only to be expected though there should still be nominal growth. I expect the coming year starting in about a month & a half from now see the Co. graduate to the next level.

The stock has corrected sharply & to my mind is already attractively valued. The pendulum we know swings rather wildly to both extremes of optimism & pessimism n it is up to us investors to benefit from this!!

16 Likes

Yes. Thank you for your reply. Corrections like these have been seen in the past as well in this counter, primarily due to very low liquidity.

Appreciate your views. Thank you.

4 Likes

Financials (Q3):

Revenues: INR 431 crores (35% QoQ).

EBITDA: INR 70 crores (5% QoQ), Margins: 16.24%.

PAT: INR 535 crores (Inclusive of INR 493 crores from woodshed business).

Financials (Nine-Month FY2024):

Revenues: INR 1,073 crores.

EBITDA: INR 196 crores (19% YoY), Margins: 18.3%.

PAT: INR 194 crores, PAT Margins: 11.13%.

Operations:

Rutschi sales concluded, strengthening balance sheet.

Project revenues rose from INR 130 crores to INR 214 crores QoQ.

Domestic segments performed robustly.

International growth expected in South Africa and Sterling, Australia.

Outlook:

Continued project revenue momentum.

Steady domestic order book.

Anticipated international growth in key markets.

International Order Book Decline (45%) and Rutschi Impact:

45% decline attributed to exclusion of Rutschi’s long-term contracts.

Order book, excluding Rutschi, remains strong and well-positioned globally.

Overall Order Book Strength:

Robust order book in all three major business segments.

Domestic product and project orders are solid.

Focus on addressing challenges related to execution improvement.

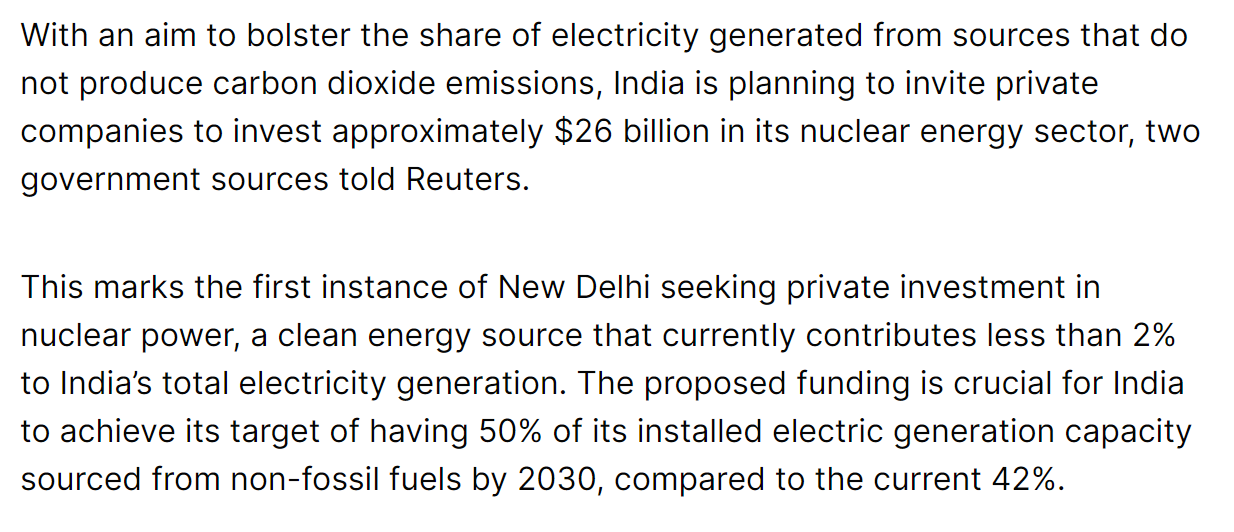

Nuclear Sector Involvement Post-Rutschi Exit:

Full exit from nuclear business associated with Rutschi.

Continued domestic production of certain pumps for the nuclear sector (excluded from Rutschi transaction).

Performance Comparison Q3 FY24 vs. Q3 FY23:

Minimal growth, earnings declined.

Management Explanation:

Year-on-year flatness from Dec 31, 2022, to 2023.

Foresees a robust Q4 with expected growth.

Attributes flat performance to a remarkable jump in the previous year (INR 1,000 cr to INR 1,800 cr).

Anticipates sustained growth, though not as significant.

EBITDA Margin Fluctuation:

Q3 international EBITDA margin dropped from 22% to 11%.

Attributed to revenue shifts, not margin challenges.

Revenue Impact Clarification:

Emphasizes that margin drop results from revenue fluctuations, not reduced profitability.

Suggests considering nine-month and yearly figures for a more accurate assessment.

EBITDA Performance and Guidance:

Q3 standalone EBITDA: 19%, nine-month EBITDA: 17.64.

Indicates stability across product and project divisions.

No significant project ramp-up to maintain EBITDA and contractual commitments.

Emphasizes the critical importance of maintaining EBITDA margin.

Benchmark figures for guidance: 17.64 standalone, 18.27 consolidated.

Execution Capacity and Future Growth:

Identifies growth in domestic and international product segments.

Improved project performance with an INR240 crores run rate.

Resolved supply chain challenges.

Anticipates growth with a robust order book.

Post Rutschi Exit and Plans:

Plans for capital deployment in inorganic expansion.

Exploration of opportunities within and outside India.

Focus on opportunities within the company’s core expertise.

Project Execution and Revenue Decline:

Improvement in project execution noted in the current quarter.

Overall nine months show a decline in revenues.

Order book stands at INR3,800 crores (3500+ project, 260 product)

Average project completion time: 24 to 30 months.

Management’s Explanation:

Two aspects of project work: supply side and construction side.

Last year witnessed a ramp-up in the supply side, contributing to good revenues.

Lower supplies in the first half due to market challenges, now picking up.

Major rebound in construction this year, expected to increase quarter-on-quarter.

Emphasis on execution before booking more orders.

Q4 Project Execution and Growth:

Expecting better Q4 project execution compared to the previous year.

Targeting improvement on last year, aiming for around INR900 crores.

Pump and Accessory Business:

Decline noted in the current quarter and a 6% growth on a nine-month like-to-like basis.

Management’s Insight:

Segment has a strong order book and good execution.

Anticipates growth, though not as high as last year.

Unallocable Expenses and Tax Rate:

Sharp rise in consolidated unallocable expenses in the nine months.

Effective tax rate for nine months closer to 30%, up from 25.6% last year.

Management’s Clarification:

Unallocable expenses increase due to specific regrouping in consolidated figures.

Tax rate influenced by capital gains tax for a transaction.

Proceeds from Rutschi and Future Plans:

Priority was debt settlement, freeing up INR650 crores cash with INR150 crores in borrowings.

Focus on growth opportunities, primarily utilizing available cash.

Considering reversing holding or fixing leakages in minorities at Holdco level if growth opportunities are not realized.

Current Strategy:

Primary target is growth, exploring interesting ideas and markets aggressively.

Fixed deposit rates are favorable, cash is effectively parked.

Will review strategies if growth opportunities are not effectively utilized.

Profit Margin Decline:

Operating margins dropped from 19.2% to 16%.

Main raw material: steel; prices stable.

No specific reason for the decline.

Middle East crisis, Suez Canal blockage affecting Italian business’s supply chain in Europe.

Some missed dispatches last quarter will shift to the current quarter.

Nine-month EBITDA margins at 18.27%.

Assured decline not due to costs or revenue.

Future Outlook:

No expectation of further margin erosion.

Positive environment, anticipates improvement.

User Industries and Growth:

Domestically, industrial segments like steel and oil and gas are contributing to the growth.

Municipal segments are strong due to focus on Jal Jeevan and Swachh Bharat missions.

Internationally, oil and gas markets in Australia and Italy are robust.

Strong presence in municipal water supply markets, especially in South Africa’s mining industry.

12 Likes

One of WPIL’s offerings…

After the recent developments in this area, a question arises if WPIL would benefit from this…

9 Likes