If anyone is contemplating investing in Welspun, one needs to consider very high debt on balance sheet in addition to what all is going on just now. Even if company can salvage something, overall stress on balance sheet could be quite severe. For punters, trying to take advantage of inevitable fluctuations in price, nothing can be said.

7 Likes

@Prash thanks for sharing the article. Looks like 90% of goods sold as egyptian cotton made have actially not used it as per article. This makes me think if there could be bigger problem in d industry and if federal agencies start coming into play it may get much more bigger problem for other companies as well. This makes me think shud i be holding indo count currently 10% pf or atleast reduce my stake. Thanks!

My 2 cents in few sentences.

Salad Oil Scandal and Buffett - Buffett took advantage of adversity because he had the required information to take a call. Do we have the required information to consider this as a buying opportunity. SIMPLY NO. Are these two similar situations? SIMPLY NO.

Approach to say only x% revenue comes from Egyptian cotton, hence price fall not warranted - With all due respect totally a wrong approach in the light of the fact that Target terminated entire relationship with Welspun and not just Egyptian cotton related prods.

Is the price fall justified? IMHO yes as there is fear of other clients pulling out.

Is the above fear justified? IMHO yes. WHY? Because what would I do when in shoes of Walmart, Bed & Bath and JC Penny’s of the world? If I find that same thing happened with me I would also pull out from Welspun, because (1) Target did it and I don’t want to be viewed as compromising on quality/standards/delivering to customer what I committed (even if quality is good) when my competitor doesn’t do it (2) Customer is GOD for me and not the SUPPLIER. I can SUBSTITUTE a SUPPLIER but not a CUSTOMER if he walks away.

Lastly buying at times of adversity would more aptly apply to a company like AYM Syntex because it corrected substantially due to Welspun issue as market perceives it to be related entity. Technically management separated but one can say that family is same [even if Son (Abhishek) has taken over the reins]. But was the fall in AYM warranted due to Welspun issue given the fact that AYM’s business wouldn’t be impacted? IMHO answer is NO. Judging management integrity of AYM management is one’s own decision in the light of Welspun saga. I personally would keep both issues separate and would take this as an opportunity to buy into AYM.

Discl: Utilised fall in AYM Syntex to start building position in it. Not invested in Welspun.

3 Likes

Disc: No position.

Man is not a rational animal, he is a rationalizing animal - Robert A. Heinlein

-

If we were strictly following Buffett he would not touch a company with a tainted management and that would include group/associate companies.

-

Amex v/s Welspun. Amex was scammed and of course it was responsible for not doing proper due diligence. In the current scenario Target is the company that was scammed and of course it did not do proper due diligence. So I don’t think Welspun situation should be compared with Amex.

-

Amex was scammed in a subsidiary and non-core business. Its core franchise was not tainted by the scandal. In case of Welspun, it is accused of the scam in its core business and that has hit its reputation. Very different in my opinion.

5 Likes

@sagararya, i agree with you,

as far as i know, There is a fundamental difference between the two cases…in Oil Salad Case, oil was kept as collateral security and in last during recovery phase it was found that there was no oil in place, so there was court case followed buy panic which causes amex share price fall, but companies basic business (credit card and travellers cheque business) was not at all faulty at any level in which he invested (business), after the court case they hav to pay huge fine. There was no effect in earning by business itself,although extra special expence would hav been there in balacesheet,reducing there net frofit / EPS…

@Sowmay,in my view both scenario are totally different, here business itself in trouble

dis…not invested,expecting it as possible turnaround in future…

On the point of it being an industry wide issue - Don’t know.

But being an investor in Indo Count I attended their Q1FY17 earnings call in the morning. Was very surprised and disappointed to hear their reply to the question on (not quoting exactly) 'What are the checks or controls measures they have in place to ensure that raw material supplied to them is the same as demanded?"

Mgmt. said that they depend upon the supplier’s certification and guarantee and don’t perform any tests/checks on their part. Mgmt. also said that they are not aware of any such testing mechanisms. To be honest I am angry hearing this response apart from being surprised and disappointed. In layman terms, I am pretty sure that there are various fibre testing mechanisms/processes existing, to test if raw material being supplied is as per standards asked for or not. We can see this with the help of a simple Google search. Mgmt. of a company that runs this business saying that they are not aware of any such mechanisms does take me back. I was surprised to see the so called analysts take this on face value and not countering it.

If Target also depended on Welspun’s guarantee then they would not have identified this issue. In all probability Target would have also conducted tests to come up with a conclusion that raw material used is not as per contract. Then how can companies like Indo Count not do such tests on raw material being received.

In the light of above facts there can always exist a possibility that despite mgmt.'s best intention they can end up supplying non contracted/inferior quality products to the end customers.

Cheers.

Discl - Invested in Indo Count.

2 Likes

I can confirm this. I have audited one high end retail fashion chain and noted something similar. Many times top management has no clue that procurement manager is perpetrating fraud. Some times its so deep routed and sometimes it gets missed despite all good intentions of management. Some benefit of doubt can be given to WS Top management on this count. Though it does not absolve them from larger issue and tone at the top is ultimately their responsibility.

Disc: Not invested.

1 Like

For me its a binary event. No too many unknowns. Either there is a deep routed problem in their quality or NOT. And I am sure all large customers are capable to assess that. So either they will pull out or stay. I am not running after it. Just trying to objectively analyze the situation. “Separating the wheat from the chaff” That’s why we are here. right?

There is no doubt. And its quite possible.

White Inverted Hammer formed. It has a long tail, and a huuuge volume to follow… Also, historically oversold levels on RSI too! Expecting a bullish day tomorrow to confirm the signal. Maybe the Selloff is complete, until, more shit hits the fan. ![]()

DISC: Initiated position (Nibbled some) today.

I think everyone posting on this thread should make their disclosures clear.

Discl: Not invested.

This shows the fall was pretty much not as worse as it could be, Shows more damage can be done. Market assumption is that the big 5 clients will severe all ties, this may prompt smaller buyers to run aswell. More bloodshed to come.

Discl: Not invested, watching carefully.

For God’s sake ‘no one is going to die here’ just because the thread is from another type of cotton in a bed-sheet. This is not like a bad batch of drug from a pharma firm, due to a FDA non compliance. That said, I can completely understand how US clients behave. Invariably, this issue will be taken as an integrity issue, rather an ‘inconvenience’ issue. What baffled me is that the dating back to 2014 shipments. What have been they doing all this time?

I am not sure whether Welspun has the kind of suave International talent to manage such black swan events. All the big 4 talk is fine; they will give another report and move on but Welspun has to do the heavy lifting and open the dialog with these customers and convince them of course. I hope that they have given some serious thought to how they are going to revive this.

PS - invested and cringing/ views will be biased

2 Likes

I really wonder if the there are so many suppliers to fill the welspun quickly?

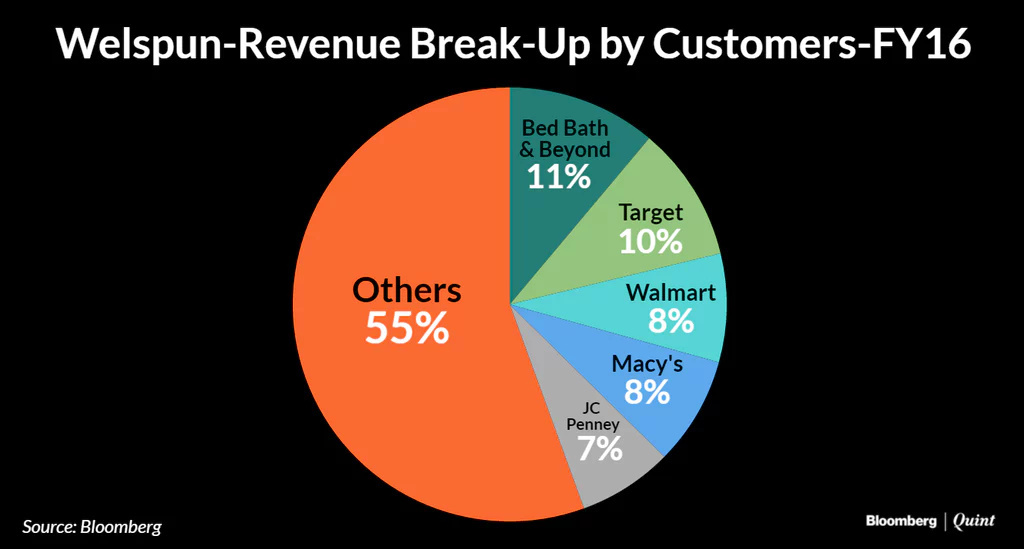

What is the damage to the business of Target/Wal Mart if they stop sourcing from Welspun and cannot replace with new suppliers quickly?

Will they stop selling bed lines/towels? Do we have any data on how many suppliers does Target/Wal-Mart/JC Penny for this kind of product?

Finally, in the business I feel, things has to settle at some point. If it’s so easy for BigBox retailers to severe ties with Welspun and switch to other suppliers with very less damage to their own business, that means Welspun had close to zero moat.

2 Likes

I feel the following may happen in Welspun case:

- Customers will stop buying Egyptian Cotton bedsheets from Welspun. And some more. Welspun may lose 10-15% of its sales. Customers will not stop buying other items from Welspun right away, because there is a huge lead time in developing a vendor, validating their manufacturing processes and getting the designs right.

- Customers will extract their pound of flesh in 2 ways- one, levy a penalty for the misleading supplies over the last 2 years; and two, get a price reduction for future supplies. Other customers are getting into the act as it is sort of a ‘free lunch’ for them.

- Welspun will produce report from EY to present their side of the story. This will be primarily used as a negotiating tool for lower penalty and price cuts.

As a result of all this, its margins will suffer for the next 3 quarters and will have impact on its profitability for the coming years. It may take Welspun at least 2-3 years to get back to speed. Factor in lower sales and lower margins and estimated one time penalty in your projections and see if it still makes sense to buy at current prices.

PS- Not invested and do not intend to.

4 Likes

The simple fact that the company cheated one of its biggest customers is a good enough reason for me to not invest in this company – irrespective of the valuations.

2 Likes

I get that Target was also on call and then they have to be politically correct always.

1 Like

I think its not about management integrity (i.e. they knowingly substituted), but a supply chain issue.

Looks like Egyptian cotton is regularly substituted by cheaper products. To note, there isn’t much Egyptian cotton in the world (0.2% of global output) and when an Egyptian organisation tested the products on counter marked Egyptian cotton; 90% didn’t have any trace.

I am not sure of amex relevance (amex scandal was small in terms of relevance for them, but this issue for Welspun is slightly bigger); but this to me does not appear like a Volksvagen scandal (i.e. management knowingly involved).

In short term, i think, everyone would review Welspun’s products; but donot think other giants would sever ties completely, may be stop buying Egyptian cotton based products from Welspun. Also, the capacity would be fungible, in sense that they would be able to use that capacity for producing something else.

Disclosure: invested after recent drop, c. 1% of my portfolio.

7 Likes

I couldn’t find a method (on which everybody agrees or is a proven and accepted method) to test if a finished product is made of Egyptian cotton. Although ‘Cotton Institute of Research’ (CIR) says that it has developed a DNA-based Technology for identifying the presence of Egyp-tian Cotton Fibers for Various Textile Products, BUT ‘ADNAS’ advertorial paper (source link given at the end) claims that these CIR claims cannot be validated and are not reliable. The Egyptian Cotton Gold Seal is given on the basis of the above test developed by CIR.

Target found this non compliance problem in products sold under its ‘Fieldcrest’ label for items produced by Welspun between August 2014 and July 2016. Target also said the below : (source link given at the end)

I wonder how did Target test all this conclusively for all suppliers including Welspun? Did they rely on the above CIR developed test? Did Welspun use any cotton other than Extra Long Staple (ELS) and therefore its non-compliance could be detected (I think all type of premium cotton like Egyptian, PIMA, etc. are ELS)? Target has denied till now to share exactly what tests they have conducted etc.

As stated by Narender above, Cotton Egypt Association itself claims that 90% of the products labelled as Egyptian Cotton are fake. Ironically this claim was made in the Welspun showroom itself while awarding them the Gold Seal ![]()

Some interesting reads. Pasting the links below. Pasting some points from these links too.

Q. Can you determine if this product is made from Pima, Egyptian or extra long staple cotton?

A. Maybe. First it should be noted that the supplier should be able to provide documentation to prove that extra long staple fiber has been used. Supima has a program through which you can determine approved suppliers of Pima products. http://www.supima.com/locate-suppliers/. As for testing, there is no physical test that will make this determination once the fiber is converted into a yarn. Very fine yarn counts (Ne 50/1 and higher) are most likely made from extra long staple (ELS) cottons just based on the physics involved. In other words, it is not physically possible to create extremely fine yarns from shorter staple fibers. Some research has been done to use DNA testing to determine Pima versus other cottons. For information on the possible use of this technology see the Applied DNA Sciences website: http://www.adnas.com/products/biomaterial_genotyping

Above info is from the following link - http://www.cottoninc.com/fiber/quality/PELab/PE-Lab-Frequently-Asked-Questions/

The following link sheds some light on ‘Complex cotton supply chain issues’ http://www.just-style.com/comment/cotton-supply-chain-transparency-an-ongoing-challenge_id128623.aspx

The following link is for ADNAS advertorial paper on ‘Testing processes for Premium Cotton’. This link also talks about why CIR method of DNA testing for Egyptian Cotton cannot be validated and is not reliable. http://www.adnas.com/sites/default/files/downloads/the_truth_about_testing_processes_for_premium_cotton_for_htt_may_2016.pdf (ADNAS seems to have a proven technology to distinguish PIMA cotton from the rest)

Note: Pasting the above only from an educative point of view. Please do your own due diligence.

Discl: Invested in Indo Count and hence curious with regards to above issue. Not invested in Welspun.

10 Likes

Exactly. I think the audit results will in favor to Welspun.

Welspun had appointed the EY for the same (as per the report of Bloomberg - Welspun India Hires EY to Probe U.S. Export Lapses ):

The company has appointed Ernst & Young LLP to review our supply chain systems and processes,” Welspun India said in a BSE filing.

Further, they also stated:

The audit will give us clarity on a number of questions, including where and how the issue occurred and what steps we will need to take to tighten our processes,” Welspun India Managing Director Rajesh Mandawewala told analysts in a conference call.

Promoters hold almost 73% of the stake and looks like they are really highly concerned about the row.

Updated.

Disclaimer: Invested after 3 LC.

1 Like