Anyone attending AGM (in Bangalore). Please share notes.

My notes from vst tillers AGM. Request others add /edit. (I may have misinterpreted few things while preparing notes)

New CEO Mr Antony Cherukara was there at AGM. He has worked earlier with Mahindra and Kirloskar. He interacted well with shareholders even after AGM. He seems to have good understanding about tillers,tractor products and farm mechanisation.

Fy 18 was tough for the company. Drought situation in key markets Gujarat,MH affected VST. Presently monsoon is good expecting company to have better FY20.

Tillers : Govt changed subsidy to DBT which impacted sales. Dealer had problem with cash. We didn’t want to extend credit. Our receivables have reduced. Q4 sales were significantly impacted.

We have lost market share in last FY. kirloskar and kamco must have gained. This year its improved and will maintain more than 50% market share.

DBT situation is still problematic, not many changes have happened compared to FY20. No update on states releasing subsidy amount at this point.

Andhra haven’t released subsidy amount for two years( provided provision), Assam has been good but patchy.

New 16HP launching soon and other variants.

China competition is there but not significant.

Tractors:

Compact segment last year it was tough due to competition launching low HP tractor. Around 15 variants of low HP tractors by other players. As farmers wanted to try new launch, our sales affected but in Q1 we are back indicating our low HP tractors doing good. Problem with gear box of low HP has been solved.

Whole tractor industry was affected due to drought in Guj/MH but we suffered most as these two states we get maximum tractor sales.

Higher HP tractors (39,42,45) launched in market. Sold around ?100 tractors. These are our own manufacturing at Whitfield factory. Once we reach reasonable scale will be shifted to Hosur. Target is to sell more than 1k tractors in FY20.

We are not aiming to gain market share or compete with big players. When we try to gain market share we will be burning cash. Plan is to build slowly over 5 years and remain profitable.

Product positioning as required by farmers at specific region is important. (At Nasilk farmers prefer four wheel drive but not in Guj depending on crop they grow. Punjab,Haryana requires high end tractors with special features, UP farmers require higher HP normal tractor. These states are good market for higher HP tractors)

Going by data market size and need for farm mechanisation is high. Don’t think tractor market is saturated.

47 Branson tractor indigenisation will happen over the next few years.

250 Cr capex spent almost 75%. Expanding tractor line for higher HP tractors.

New launches and variants may cause pressure on margins in the short term but will improve slowly.

Problem with our vendor base has been solved. Have new vendors for higher HP tractors.

Exports: FY 19 more than 600 tractors. Have presence in more than 15 countries including EU. Fy 20 not expecting much exports focusing on providing right product range in existing markets.

Dealers: 100 new dealers in fy20. Majority for tractor division.

Other products: power reapers doing well. Expect good sales. Power weeder: too much competition …not expecting good growth. Rice transplanters difficult to crack the market and make famers to learn it.

Discl: I have reduced my earlier holdings…currently having tracking position.

11 Likes

Can you please elaborate?

Earlier subsidy was provided through other medium & end user had to pay actual cost minus provided subsidy… Now you have to pay full amount and subsidy gets credited to your bank account.

Its similar to LPG refills, if you use

1 Like

What does “Dealer had problems with cash” mean? And why did it impact sales?

@VijayShetty it’s very difficult to understand the problem with DBT process. Every time I have interacted with company I have got different answers about it. Previously they use to get dbt at dealer level, then it is changed to directly company getting money from govt, now it seems to be directly transferred to farmers.Each state govt seems to work differently. Based on interaction still some states the invoicing and transfer of dbt happening at dealers/distributor level that must have changed. Overall it’s difficult to get perfect answer with each govt having it’s own method. Overall tillers business is difficult because of dependence on DBT and mansoon.

1 Like

Promoters increased holding… although its too small (3203 shares) to make any major impact

5DD36F86_D441_46F1_825C_AC6D4B7CFAA5_154241.pdf (974.1 KB)

Another buy action (29th August 2019) of promoters increasing holding further… again its small (1297 shares) … but certainly shows intent of promoter

CF4F2A59_86F7_4F86_AB88_7397B1EB59F4_144146.pdf (929.7 KB)

Once again buy action (16th September 2019) of promoters increasing holding again its small (3749 shares) but good to see continuity …

EFDABD44_F4BB_41EC_808A_879098C01210_163601.pdf (1.0 MB)

Few more transaction (all buy) by various promoters

3437CA2D_38A1_46BD_91D6_204067B95308_161126.pdf (65.9 KB) 43BA0E5F_3F48_4C7C_ACF2_0B64CBD21B15_170725.pdf (129.6 KB) 9F238115_E413_4D31_BB44_17AB0EB01EF8_170903.pdf (77.5 KB)

Looks like there is internal instruction (on lighter note) to buy ![]() shares at current levels which have become attractive

shares at current levels which have become attractive

1 Like

I am sure that their major focus states like Telangana, AP, Karnataka, TamilNadu have all received very good rainfall and all their dams are full. with Kaleshwaram project, the area under cultivation also will increase in Telangana. This may augur well for their tillers and Tractors. The Kharif season should be good atleast in South.

1 Like

Management is holding concall on 25th Nov, after 20 days of result declaration, results didn’t have anything special. As the notification of concall came after 3 weeks of results, can we guess that management has something special to share. Recent observations were that promoters kept on adding (although in very small quantity), monsoon was good (although a bit late) & Maharashtra got badly affected due to late rains (most of the political parties have started raising this issue now).

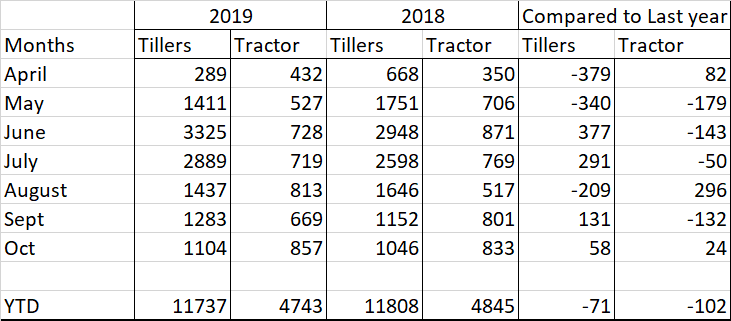

2019 2018 Compared to Last year

Months Tillers Tractor Tillers Tractor Tillers Tractor

April 289 432 668 350 -379 82

May 1411 527 1751 706 -340 -179

June 3325 728 2948 871 377 -143

July 2889 719 2598 769 291 -50

August 1437 813 1646 517 -209 296

Sept 1283 669 1152 801 131 -132

Oct 1104 857 1046 833 58 24

Months Tillers Tractor Tillers Tractor Tillers Tractor

April 289 432 668 350 -379 82

May 1411 527 1751 706 -340 -179

June 3325 728 2948 871 377 -143

July 2889 719 2598 769 291 -50

August 1437 813 1646 517 -209 296

Sept 1283 669 1152 801 131 -132

Oct 1104 857 1046 833 58 24

YTD 11737 4743 11808 4845 -71 -102

concall details

- QoQ Topline grew little bit but bottomline down due to raw material cost

- Raw material cost increased from 64% to 72.5%…

- High HP products have high material cost

- Company will be under margin /ebitda pressure for couple of more quarters due to new products

- Employee cost had increased and will remain around current levels & not expected to go down as resources are needed for future topline growth

- Dealerships for higher HP products has grown from 22 (Q1) to 40 (Q2) dealers (target to achieve 60 by EOY) - Each dealer (added in Q1) is selling approx 2 Tractors per month

- Q2 : tractor revenue / tiller revenue : 65 cr / 77 cr

- Inventory at dealer level has gone down - cirrently approx 2700 Tillers / 2000 Tractors

- First half capex is 6 cr - annual capex could be higher due to Higher HP products

- Subsidy is still awaited from most of key states (Orissa, Assam) - Assam subsidy disbursement expected in third qtr / Orissa will follow later in current year

- TN / Karnataka went well with subsidy for tillers & we are good with them… Maha stuck due to election

- Total capex 210cr as per annual report - 60-70% is already done

- Power ripper can be 15% more than last year but no meaningful impact as the no. are too small

- Rice trasplanter has grown but its still very small part of topline

- October was good / November - December look flat - current year will be flat or a little bit above on last year

- No commitment on guidance for next FY

- Excited with pull requests from dealers for Tractors - could help in future topline expansion

- Other expenses increased in current qtr - slight planned increase in travel/admin expense

- Focus area is MP & UP for new dealers

- In tiller market we regained lost market & we are back to around 50% again

Capacity utilization

Tiller - 50%

tractor - 40-45% (higher HP is very low)

- Higher HP tractor production is only in whitefield facility, can’t achieve breakeven till it is manufactured in Whitefield plant (as it has higher cost of production) … plan to move to Hosur facility as well (till end of FY 21)

- Currently no plans of monetizing whitefield land… but will be taken up later

- Kukje technology transfer used on only 47HP … no plans to expand for other products - evaluating others for technology exchange options

5 Likes

VST Tillers Tractors Ltd. MOU with ZETOR TRACTORS (Czech Republic)

These players with over 120 Years of combined experience agreed upon the joint product development, manufacturing and business plan for tractors with a horsepower greater than 36 HP for India and global markets. The key aspects of the MOU are as follows:

- Joint development of Products.

- Manufacturing of tractors by VST at its new high horsepower manufacturing facility.

- Marketing of the jointly developed product in both the Indian and global markets through a JV between VST Tillers Tractors Ltd. and ZETOR TRACTORS a.s. The jointly developed products would be sold through VST channel partners in India and Zetor channel partners in the international market.

- Explore marketing of VST products through channel in the global market.

VST Tillers Tractors Ltd. Chairman Mr. V.K Surendra informed that VST has always strived to get the best technology for the Indian farmers while VST remains a leader in the compact tractor segment and the power tiller segment; this MOU would enable VST to bring better technology in the higher horse power segment for the benefit of Indian farmers.

Zetor already has a long history in India with their earlier collaboration with erstwhile HMT Ltd and products like HMT 5911 was very popular in India. Zetor Tractors currently exports to more than 56 countries and has a customer base of 1.3 million globally.

2 Likes

Capex of 200 Cr planned for higher HP range tractors

thehindubusinessline.com/companies/vst-tillers-tractors-partners-czech-firm-to-invest-rs-200-crore

Demand for tractors has outstripped supply, as output has fallen with factories operating at a quarter of their capacity. Segment leader Mahindra & Mahindra has started planning for a second shift to meet demand, while rivals Escorts and Sonalika tractors have indicated that the market would return to normal levels within a quarter. Insiders expect the segment to continue growing and post the best performance in the automotive industry.

Almost all the players are struggling to meet demand and the concern is not on where the demand will come from but the concern is how we will make enough tractors, enough cars to meet the demand, says Pawan Goenka.

4 Likes

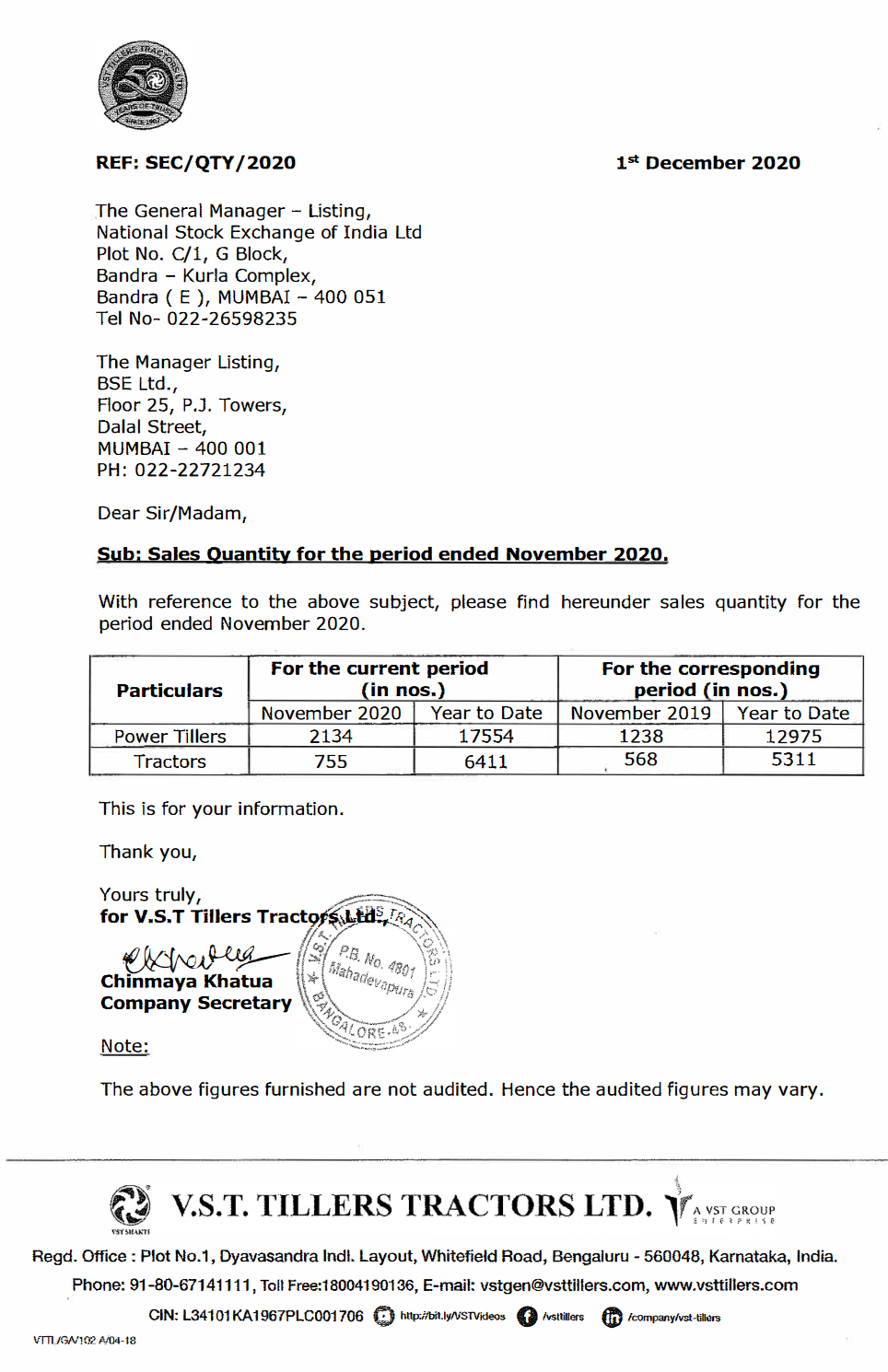

Good going by VST Tillers…

The company has sold 2134 power tillers in November 2020 as against 1238 in November 2019, registering a growth of 72.37% growth YoY.

The company has sold 755 tractors during November 2020, as compared to 568 in November 2019, registering a growth of 32.92% YoY.

The company has sold 17554 power tillers YTD (April 2020 to November 2020) as against 12975 during the period April 2019 to November 2019. The company has sold 6411 tractors YTD (April 2020 to November 2020) as against 5311 during the period April 2019 to November 2019.

Over the longer term the company has set an ambitious target of being a 3000 crore company by 2025 in diversified farm mechanization products and solutions with aim of garnering over 50% market share in Tillers.

1 Like

The guidance is predicated on good contribution from contract mfg. of Tillers for other OEMs and new business segments like precision components to their topline in 5 years.The company seems to be planning to become a one-stop shop for many requirements of farmers.At the same time they plan to expand the tiller market further by helping other OEMs.The best part is that after the 80-85cr. capex this year,company will be increasing tractor capacity by 150% and won’t need much capex for few years.They are already sitting on ~300cr. cash and with such limited capacity requirements,company can really ramp-up marketing spends in a big way.Let’s see how they go about it.One interesting change in the tillers market is that 29% of the buyers are now buying without any subsidy(though this is down from 45% a qtr. ago)

3 Likes